UK - Winter outbreak and Brexit to delay 2021 recovery

- 02 December 2020 (5 min read)

Key points

- The virus has left a 10% hole in UK output – and a winter outbreak and Brexit disruption could dampen any rebound over the coming quarters

- An easing of restrictions and a vaccine should lift growth by 4.6% in 2021 and 6.5% in 2022

- Policy support will remain important. We expect a fiscal stimulus package next year and more QE from the Bank of England, although on balance we do not expect negative interest rates

Pandemic leaves devastating gap

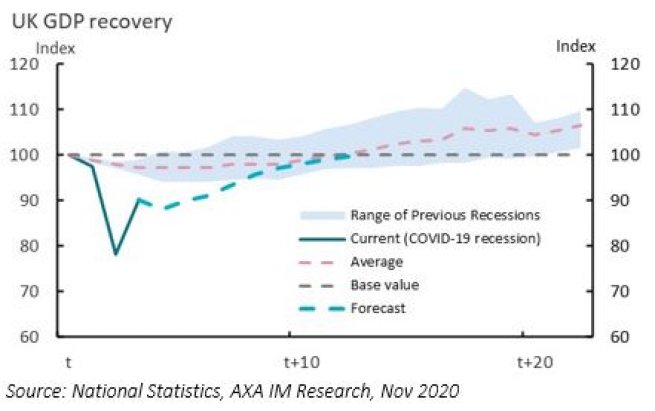

The pandemic saw GDP contract by 19.8% in Q2 – the sharpest quarterly fall on record and one of the worst worldwide. Despite a 15.5% rebound in Q3, output remained 9.7% below its end-2019 level. The return to national lockdown in Q4 – albeit shorter and less intense than before – looks likely to see a further drop in GDP by year-end. We forecast GDP at -11.2% in 2020. Exhibit 1 illustrates how this compares with previous recessions.

Exhibit 1: GDP comparison with prior recessions

We predict a rebound in 2021. With lockdown ending in December, 2021 should see an initial strong rebound, but we are mindful of risks. While there are glimmers of hope that new virus cases are slowing, restrictions will not be fully removed in December and renewed deterioration is possible in January. We expect mass vaccination from around mid-2021, offering the prospect of an economic boost later in the year. While distribution prospects are daunting, demand for a vaccine appears high. Earlier inoculation of vulnerable and essential workers should also provide economic protection against a renewed pick-up in virus cases.

The UK will complete Brexit this year. At the time of writing, the UK and EU were yet to agree a post-transition trade deal, although we expect one soon. This would avoid further separation costs and allow wider agreements, including equivalence for some financial services. Yet any agreement would be a bare-bones deal and estimates suggest that even a comprehensive deal would cost the UK 4.9ppt of GDP, compared to 7.6ppt in the event of no deal1 . Around 5% of British business reports being fully prepared for new trading conditions2 . We expect disruption at ports to block exports, build inventory and curtail production. The UK exports around 9.5% of GDP in goods to the EU in a normal year, so costs could be high. A ‘no deal’ outcome would be worse and could lower GDP growth by a further 1ppt in 2021.

We are cautious in our outlook for growth in early 2021 and pencil in a 4.6% rise for the year as a whole – the fastest since 1997 – but this would still leave GDP 4% lower than end-2019. A vaccine in H2 2021 should help recovery in 2022, when we forecast 6.5% growth, leading activity to regain end-2019 levels by end-2022. With supply capacity still rising, even then we would forecast excess supply. However, permanent losses associated with Brexit and scarring from the pandemic should see the output gap close in 2024.

Spare capacity is likely to be most obvious in the labour market. The furlough scheme has supported the economy and unemployment has only risen to 4.8% to date. However, it has also disguised the amount of labour market slack and with the scheme extended until March, this will continue into next year. For now, we expect unemployment to reach 7.5% around mid-2021 and retreat to 5% by end-2022.

The extension of the furlough scheme and other support measures will be key to ensuring a pick-up post-lockdown. Yet to drive recovery, a medium-term package of growth-enhancing measures is likely to be necessary. We expect a material fiscal easing in next year’s Budget. Yet with a deficit approaching 20% of GDP and debt exceeding 100%, the Treasury will also consider longer-term consolidation.

The Bank of England (BoE) will also provide support. Following a further £150bn of QE in November, the BoE forecasts inflation at 2% from mid-2021. We consider only a brief rebound and inflation to average 1.5% in 2022. Further stimulus looks necessary to return inflation to target. We expect more QE, with a further £75bn in Q2 2021, extending purchases into 2022. Yet we doubt the merits of negative rates and do not expect the BoE to experiment with them as the foundations for recovery take shape from mid-2021.

- IOKAnEVVIEV4aXQ6IExvbmctdGVybSBlY29ub21pYyBhbmFseXNpc+KAnSwgSE0gVHJlYXN1cnksIE5vdiAyMDE4

- TW9uZXRhcnkgUG9saWN5IFJlcG9ydCwgQmFuayBvZiBFbmdsYW5kLCBOb3YgMjAyMA==

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.