Pensions investment outlook 2024: Mining for opportunities amid easing growth

- 06 December 2023 (7 min read)

Key points:

- Global economic growth is likely to remain subdued in 2024, with some pick-up in 2025

- Given bond yields have risen to multi-year highs, fixed income has become increasingly attractive for pension funds

- Demand for sustainable investments should continue to rise

Global economic growth is expected to ease in 2024, creating fresh challenges for pension fund investors. Some pick-up is expected in 2025, but risks around inflation stickiness and geopolitical tensions persist, meaning schemes will continue to navigate an uncertain environment.

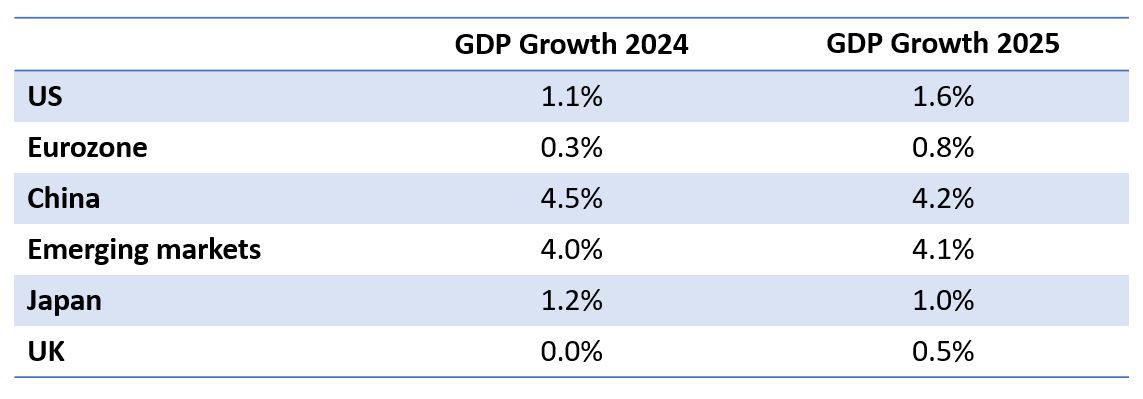

Overall, we forecast global growth reaching 3.0% in 2023, 2.8% in 2024 before rising back to 3.0% in 2025.

However, we believe that judicious asset management decisions should help pension fund investors steer a course through this coming period of likely modest growth and returns.

Macro backdrop

The US economy will probably avoid a recession in 2024, but a marked slowdown over the coming quarters is likely before growth picks up in 2025. But the world’s largest economy will set the pace for the global economic outlook.

China should achieve its internal economic growth target in 2023, managed by fiscal policy fine-tuning. The extra stimulus already announced will have a positive effect next year and the growth path will quicken in 2024 before easing in 2025. However, longer-term structural economic issues will persist.

The Eurozone is more likely to see a slowdown in activity in 2024. Thanks to falling inflation the bloc should avoid a recession but economic stagnation throughout next year is very likely before a mild recovery will take place.

AXA IM: Forward looking estimates for economic growth

Inflation is likely to return to the European Central Bank’s (ECB) 2% target late in the first half of 2025, with the ECB starting to loosen its monetary policy likely from the middle of 2024, but fiscal stability risks might become a feature. High deficits in Eurozone countries will likely lead to a flood of new issuance of government bonds, putting pressure on the long end of the curve. However, this could potentially meet stronger demand by institutional investors like pension funds.

Economic growth in emerging markets (EM) is expected to continue, albeit with most of the acceleration driven by smaller EM countries. Tighter global financial conditions will increase stresses, but most EM economies will be structurally more resilient than in previous periods.

All eyes will be on November’s US Presidential Election as its result will have reverberations worldwide, setting the political scene for the coming years.

AXA IM: Forward looking estimates for average inflation

Bonds and alternatives increasingly attractive for pension funds

While the global economy is not stagnating, growth is expected to slow in 2024, potentially working its way via lower profit margins into lower equity prices.

Tighter monetary policy in 2023 caused bond yields to rise significantly, first in short maturities and in the second half of the year, in longer maturities too.

As a result, bonds have become increasingly attractive for pension funds, in particular investment-grade credit and sovereign, supranational and agency bonds.

In the alternatives space, liquid assets, asset-backed securities and collateralised loan obligations can potentially deliver attractive spreads too.

High interest rates have also improved the funding ratios of pension funds overall in 2023, making a (partial) buy-out by insurance companies increasingly prevalent in the last decade.

In addition, elevated interest rates make an increased hedging strategy more appealing - through bonds, to avoid over-leveraged positions with related liquidity risks. High funding ratio positions also give greater leeway to pension fund trustees to give more indexation to their members – i.e., adjusting payments amid this high inflation environment - then leading to lower funding positions next year.

We believe adding (or expanding into) inflation-linked bonds to the asset allocation might be a little too early for pension fund investors for now, but we expect better potential for investors in this space during 2024.

The improved funding ratios in 2023 - a result of both rising interest rates and equity prices - have not completely brought illiquid investments in pension funds’ asset allocations back to previous levels yet. Although some rebalancing took place, and new commitments have been slowed down in 2023, it is expected that some repricing of real estate and private equity is still in the pipeline.

It could well take the whole of 2024 before the desired allocation to illiquid assets is back on track.

Aligning with net zero

One global trend that is continuing apace – despite some pushback - is the demand for more sustainable investments. This is relevant for all asset categories. Global equity index portfolios are being reset to net zero-aligned allocations, whether passively via index funds or actively via a readjustment of the global equity universe. Impact investments are increasingly forming part of more concentrated actively managed portfolios as well.

In the fixed income space, green bond issuance has reached a record high and the demand for impact bonds is growing (with social and sustainable goals as well as environmental ones).1 Liability-driven investments or liability-matching portfolios are becoming more sustainable too.

Investments to fight climate change via net zero-aligned portfolios are becoming more and more mainstream, while biodiversity looks set to become the over-arching theme in the coming years. The two topics are utterly interconnected: Climate change is one of the drivers of biodiversity loss and will likely overtake land use change to become the largest contributor beyond 2050.2

While some aspects of biodiversity loss may appear a local rather than global problem, over half of global GDP depends on high-functioning biodiversity and ecosystems degradation costs the global economy more than $5trn a year.3

Investments linked to the United Nations Sustainable Development Goals, a set of targets to help protect and preserve people and planet, alongside pension funds’ financial objectives and members’ personal interests, are increasingly allowing pension fund trustees to embrace sustainability to a greater extent perhaps than ever before. This can be achieved via specialised mandates as well as emphasising these aims through key performance indicators in broader equity and bond mandates.

- R2xvYmFsIGdyZWVuIGJvbmQgaXNzdWFuY2UgYWNjZWxlcmF0ZXMgdG8gcmVjb3JkLXNldHRpbmcgcGFjZSB8IEluc2lnaHRzIHwgQmxvb21iZXJnIFByb2Zlc3Npb25hbCBTZXJ2aWNlcw==

- QmlvZGl2ZXJzaXR5IFEmYW1wO0E6IFVuZGVyc3RhbmRpbmcgYSBwb3dlcmZ1bCBuZXcgaW52ZXN0bWVudCB0aGVtZSB8IEFYQSBJTSBDb3Jwb3JhdGUgKGF4YS1pbS5jb20p

- QmlvZGl2ZXJzaXR5IFEmYW1wO0E6IFVuZGVyc3RhbmRpbmcgYSBwb3dlcmZ1bCBuZXcgaW52ZXN0bWVudCB0aGVtZSB8IEFYQSBJTSBDb3Jwb3JhdGUgKGF4YS1pbS5jb20p

Pension fund allocation

For defined contribution (DC) plans, stagnation carries the most risk, as equities would struggle due to lower earnings, while bonds could also suffer because of stickier inflation and greater supply, pushing bond prices down and causing yields to rise. This could result in capital losses for DC plans, whereas for defined benefit plans, it could mean a more balanced outcome in funding ratio terms.

While interest rates in major economies are expected to have now peaked, inflation will likely remain above central banks’ targets in 2024, before slowing to desired levels by the end of 2025 – but developed markets should avoid recession. Longer-term rates will be able to decline but short-term policy rates are expected to pause at current levels for a while. Spreads could widen further, as the slowing economy may not be able to produce ongoing strong company profits, and this will in turn impact equity markets.

We expect pension funds to keep adding more resources to sustainable and impact investments in all asset classes, most likely listed equity and bonds, as the allocation to illiquid assets are still on the high side of what most funds desire in their asset mix.

Our views for 2024

View all articles

Beware the merchants of doom

- by Nigel Topping

- 06 December 2023 (5 min read)

Currencies Outlook – US dollar high(er) for longer

- by

- 30 November 2023 (5 min read)

UK Outlook – Lags could push Bank of England to faster cuts

- by David Page

- 30 November 2023 (5 min read)

Canada Outlook – Sticky core inflation challenges Bank of Canada

- by David Page

- 30 November 2023 (5 min read)

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2023 AXA Investment Managers. All rights reserved