How responsible investing standards and policies affect returns

- 06 April 2020 (7 min read)

Executive summary

- Excluding companies from investment portfolios due to certain business activities, products and services on sustainability considerations was arguably the first notable approach which came to define socially responsible investing as it emerged in the 1970s and 1980s. Exclusions continue to be the most widely adopted sustainable investment strategy, with more than 64%1 of global sustainable assets under management using this approach.

- AXA Investment Managers has implemented a series of exclusion-based policies and standards2 and in this research paper, we assess their effect on investment returns.

- Our analysis showed that AXA IM’s exclusion policies have a relatively limited impact on the investment choice available to fund managers - and excluding certain companies did not come at expense of risk-adjusted performance. What’s more, we also saw that it drove outperformance over the period studied.

The asset management industry has traditionally adhered to the notion that excluding certain companies from investment portfolios based on sustainability considerations linked to certain business activities, products and services will inevitably harm returns by reducing the investable universe. We have seen increasing volume of academic research which has dispelled this myth and shown this not to always be the case3 .

When it comes to environmental, social and governance (ESG) policies, the first question we are often asked is: What is the cost on return? As a result, we decided to assess the impact of our exclusion policies on investment returns.

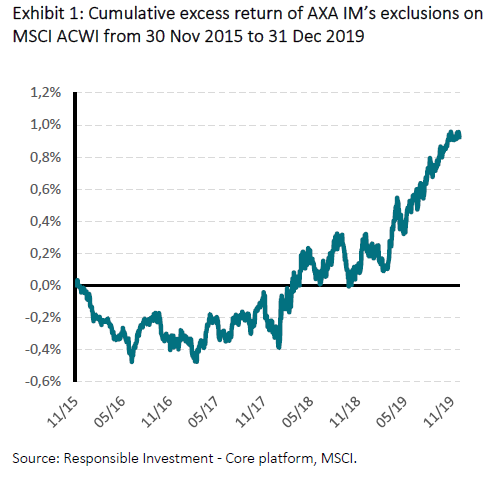

As shown in Exhibit 1 (right), over a period of 49 months to 31 December 2019, the excess return4 generated by excluding issuers across AXA IM’s exclusion policies (including all sectorial policies and ESG Standards policies) from the MSCI All country World Index5 (ACWI) is positive: +0.92%. The outperformance has accelerated over the final 12 months of the study. The main drivers of this were companies in the climate risk and tobacco exclusion policies which dragged down the MSCI ACWI compared to a portfolio composing the same index constituents without the exclusion list companies.

See Appendix for more details of our exclusion policies.

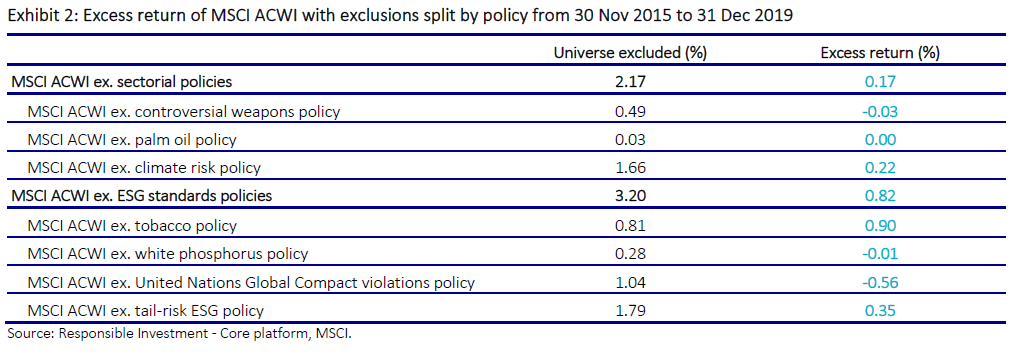

Going into more detail as presented in Exhibit 2, the excess return generated by excluding issuers in the sectorial exclusion policies is +0.17%. The excess return generated by excluding issuers in the ESG standards policies is higher with +0.82%.

A look at risk

While the return component is important, risk has to be considered to have a full picture of the impact of exclusion policies.

From a risk perspective, we can see in Exhibit 3 that annualised volatility of indices with exclusion policies are in line with the parent index. The tracking error of filtered indices is similar to passive management and ranges from eight basis points for the sectorial policies to 32 basis points for AXA IM exclusion policies.

We notice the risk/reward ratio6 is slightly improving with the increase of exclusions. We also see that MSCI ACWI ex. AXA IM exclusion policies has the highest risk/reward, while the excess return of 0.92% is lower than the sum of MSCI ACWI ex. sectorial policies’ and MSCI ACWI ex. ESG standards policies’ excess returns at 0.17% and 0.82% respectively, indicating some diversification benefit. Over the long term, AXA IM exclusion policies have not come at the expense of risk-adjusted performance on a broad equity market index.

Diversification is preserved

Exclusions, by definition, reduce investment possibilities

for portfolio managers. As described in Exhibit 3, exclusions from all policies represents 5.2% (market weight) of the MSCI ACWI index, of which 35% is explained by the tail risk ESG screen. This is why AXA IM has decided to give leeway

to portfolio managers with regards to tail risk ESG policy; thus, issuers where there is a robust investment rationale - or a clear sign of positive momentum - can remain eligible for investment. The goal is to retain the opportunity to invest in transitioning companies.

To put this 5.2% impact in perspective, the French socially responsible investment fund label ISR requires a 20% reduction in the initial investment universe using ESG indicators to meet the criteria of an ESG investable universe7

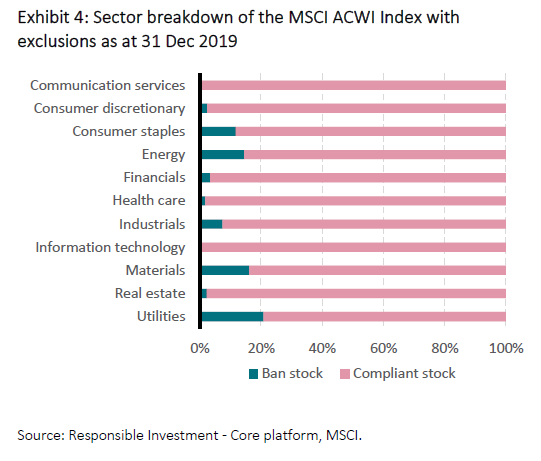

. From a sector perspective, we can see

in Exhibit 4 that exclusions have the main impact on the utilities, materials and energy sectors - but this is still limited with a maximum impact of 20% on utilities.

The impact of AXA IM’s exclusion policies on the investment universe is material, with an impact above 5%, but limited compared to criteria applied to an ESG investment universe or sector biases.

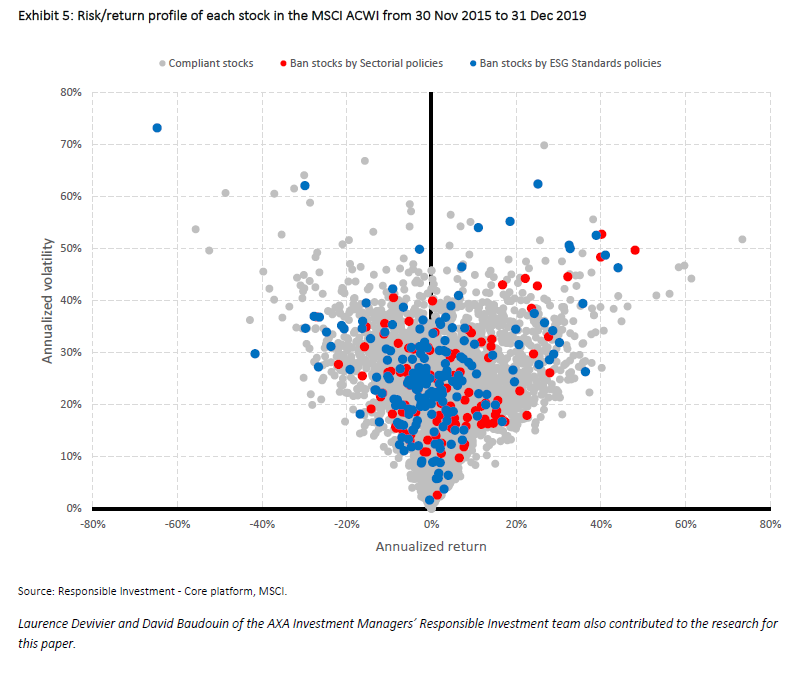

On the other hand, for diversification purpose portfolio managers aim to build portfolios made up of multiple stocks with various characteristics. In Exhibit 5, we see excluded stocks are well scattered across the risk profile spectrum of the MSCI ACWI. There are many other candidates or stocks with similar risk profiles available within the universe. We believe this shows that AXA IM exclusion policies do not affect the ability to build diversified portfolios from a risk-profile or sector perspective.

- MjAxOCBHbG9iYWwgU3VzdGFpbmFibGUgaW52ZXN0bWVudCByZXZpZXcsIEdsb2JhbCBTdXN0YWluYWJsZSBJbnZlc3RtZW50IEFsbGlhbmNl

- aHR0cHM6Ly93d3cuYXhhLWltLmNvbS9yZXNwb25zaWJsZS1pbnZlc3Rpbmcvc2VjdG9yLWludmVzdG1lbnQtZ3VpZGVsaW5lcz9saW5raWQ9cmVzcG9uc2libGVpbnZlc3RpbmctbWVudS1zZWN0b3JndWlkZWxpbmVz

- Rm9yIG1vcmUgcGxlYXNlIHJlZmVyIHRvIOKAnEVTRyBhbmQgRmluYW5jaWFsIFJldHVybnMg4oCTIGFuIGFjYWRlbWljIHBlcnNwZWN0aXZl4oCdIEFYQSBJbnZlc3RtZW50IE1hbmFnZXJzLCBKdWx5IDIwMTku

- U3R1ZHkgaXMgcGVyZm9ybWVkIHVzaW5nIGRhaWx5IGNoYWluLWxpbmtlZCByZXR1cm5zIGF0IGluc3RydW1lbnQgbGV2ZWwuIEV4Y2x1c2lvbnMgb3ZlciB0aW1lIGFyZSBldm9sdmluZyBkdWUgdG8gc3RyaW5nZW50IHJ1bGVzIG9yIGluLW91dCBjb21wYW5pZXMgaW50byBleGNsdXNpb24gbGlzdHMsIHRoZXJlZm9yZSBvZmZpY2lhbCBiYW4gbGlzdHMgYXQgdGhlIGRhdGUgb2YgcmViYWxhbmNpbmcgaGF2ZSBiZWVuIGV4Y2x1ZGVkICjigJxhcyB3YXPigJ0gcnVsZSkgdG8gcmVmbGVjdCByZWFsIGltcGxlbWVudGF0aW9uLiBUaGUgc3R1ZHkgaXMgbm90IGEgcmV0cm9wb2xhdGVkIHJldHVybiBzdHVkeSBiYXNlZCBvbiB0aGUgbGFzdCBhdmFpbGFibGUgYmFuIGxpc3RzICjigJxhcyBpc+KAnSBydWxlKS4gQSBsaW5lYXIgd2VpZ2h0IHJlc2NhbGluZyBpcyBhcHBsaWVkIHRvIGVhY2ggaW5zdHJ1bWVudCBvZiB0aGUgaW5kZXggYWZ0ZXIgZXhjbHVzaW9uIGZpbHRlcnMu

- TVNDSSBBbGwgQ291bnRyeSBXb3JsZCBJbmRleCwgbmV0IHJldHVybiwgaW4gZXVybyBjdXJyZW5jeSB1bmhlZGdlZC4=

- Umlzay9yZXdhcmQgY29ycmVzcG9uZHMgdG8gYW5udWFsaXNlZCByZXR1cm4gZGl2aWRlZCBieSBhbm51YWxpc2VkIHZvbGF0aWxpdHkgYW5kIGdpdmVzIHRoZSBhbW91bnQgb2YgcmV0dXJuIHBlciB1bml0IG9mIGV4LXBvc3Qgdm9sYXRpbGl0eS4=

- U291cmNlIDogaHR0cHM6Ly93d3cubGVsYWJlbGlzci5mci93cC1jb250ZW50L3VwbG9hZHMvMjAxOS8xMC9SZWZlcmVudGllbF9MYWJlbElTUl9Ob3ZlbWJyZTIwMTgtMS5wZGY=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.