Warning Shot

- 15 June 2020 (10 min read)

Key points

- Bad news on the pandemic front triggered some measure of market turmoil last week. Contagion from equity to credit market was limited though. Central bank support shows.

- We take a look at money supply growth. It may ultimately look more like a one-off level shift than as a permanent acceleration. We remain convinced this crisis is more deflationary than inflationary.

Last week’s market turmoil was not a replication on a smaller scale of the shock of late February and March. Contagion from the equity to the credit market was limited. The impact of the central banks’ support is showing. Still, the market’s bout of nervousness is a reminder that the recovery is not going to follow a straight line. Its immediate cause was bad news on the pandemic front from the US. We expressed last week our concerns that this country is exiting too quickly from lockdown and unfortunately the latest data strengthened this view. A new cluster discovered in Beijing is not going to help lift the mood as we start a new week.

Still, it is quite clear that appetite in the US – and elsewhere – for a resumption of severe lockdown conditions is very low given the economic cost. Healthcare capacity has been restored in the advanced economies, testing is accelerating and in Europe (where the pandemic was much better controlled by the time lockdown was released) there is still no sign of a relapse. Our baseline remains that progress towards a normalization in supply conditions will continue in the months ahead across the northern hemisphere.

Our view that the current crisis is more deflationary than inflationary is consensual – and that is what markets are pricing. However, we note highly respected economists such as Charles Goodhart are expressing their concerns that in the medium run the ongoing acceleration in money supply could trigger an inflation backlash, once the velocity of money normalizes. We discuss this in some detail. In our view the most plausible scenario is that money supply is going through a one-off level shift without embarking on a long-lasting upward drift.

Finally, even if inflation is “ultimately a monetary phenomenon”, market institutions play an essential role as well. In our view those institutions – the degree of regulation of labour, product and services market – are very different from what prevailed at the time of the big inflationary spiral of the 1970s. Still, institutional set-ups can change, and we take a look at the relaxation of state aid rules in the EU and how governments could be tempted to stifle competition as they intervene directly in strategic sectors.

Not a straight line

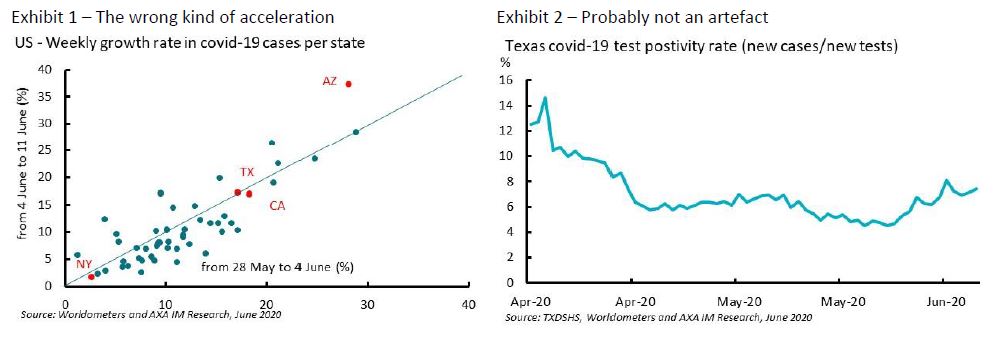

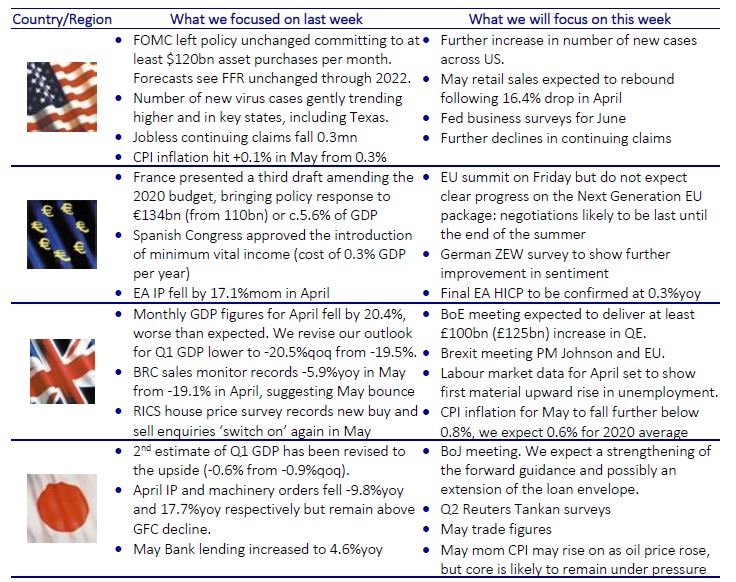

The impressive rebound in financial markets, epitomised by the S&P 500 restoring its pre-pandemic level, stumbled in the middle of last week. Some warning signals on the Covid epidemic in the US were the immediate cause. In Macrocast last week we expressed our concern that the US had relaxed its lockdown too early, in contrast with Europe. The latest data confirms those concerns. Last week’s version of Exhibit 1 already illustrated how the epidemic had stopped decelerating in some parts of the US. This has worsened, with 12 states instead of 8 where the weekly growth rate has accelerated and remained in two-digit territory.

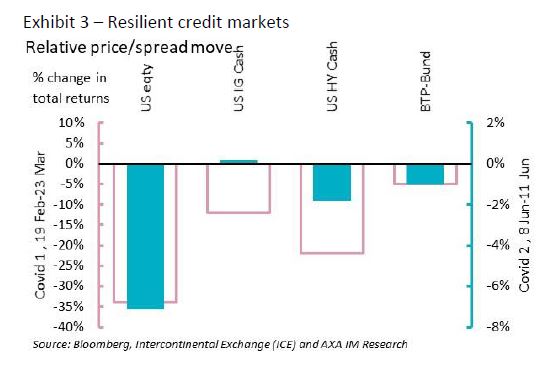

This does not seem to be a statistical artefact merely reflecting more intense testing. In Texas – on which we tend to focus, given its size (10% of the US GDP) – the ratio of new cases to new tests has risen again over the last two weeks (Exhibit 2), after initially following the usual downward trend which in hard-hit countries such as Italy was a sign that the epidemic was getting under control. The number of hospitalisations has started to climb back as well. At trough on 25 May, Texas was registering c.1,500 new hospitalisations per day. This has risen again above 2,000 for the past three days. Florida (5% of US GDP) is also high on the watch-list. The epidemic was dying down by the end of April with less than 600 new cases per day on a seven-day average basis. It has doubled since then to more than 1,200 cases at the end of last week. Another source of concern is that in some states such as California which had gone into lockdown very early and quite drastically, the epidemic is now plateauing rather than dying down.

From a purely economic point of view, the key issue is whether this could alter the path towards economic normalisation in the US. Treasury Secretary Mnuchin stated last Thursday that the US “can’t shut down the economy again”. However, there is not much federal authorities can do since lockdown measures are in the purview of the states. Attitude to risk differs a lot there. The Governors of Oregon and Utah – two of those “accelerating states”, albeit from a very low absolute level – announced a pause in the re-opening process. Conversely, the Governor of Texas – who ordered the first relaxation measures as early as on 30 April – confirmed on Friday his decision to allow restaurants back to near-full capacity, stating he was “concerned but not alarmed” by the latest figures.

These recent developments – together with a cluster of “home grown” cases in a market in Beijing - should act as a reminder that the recovery is unlikely to be a straight line. There can be delays and setbacks on the way. Our baseline remains though that given the already massive economic cost, authorities will be very reluctant to re-engage into the sort of severe lockdowns we have been through in April and for most of May. In advanced economies the healthcare systems have had time to rebuild capacity or develop new ones (Texas communicated on wide availability of respirators across the state’s hospitals). Testing capacity has also improved even if more progress would be needed. Europe continues to show no sign of relapse. The speed and intensity of the mechanical rebound may have been dented, but for now this continues to be the most plausible path.

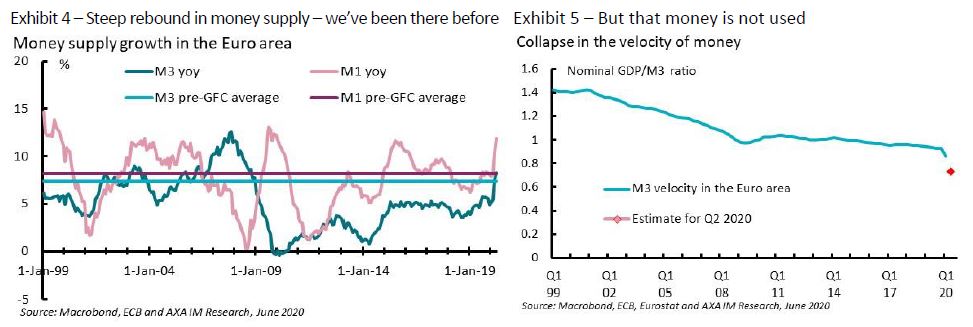

In the meantime, last week provides an interesting “natural experiment” in the way the market now reacts to pandemic-related news. Indeed, the market reaction was not a mere replication on a smaller scale of the late February/March rout. Of course, the losses last week were only a fraction of what was observed then, but rescaling for the change in equity returns, interesting insights emerge (Exhibit 3). Last week, the credit market held up well. In February and March, the drop in returns on the US high-yield market stood at two-thirds of the one incurred by equities. Last week it was only a third. The investment grade credit market barely moved. We must be cautious when drawing conclusions from what has been a very short move, but for now at least the impact of aggressive involvement by central banks is showing.

Should we panic about money supply?

If anything, the market gyrations of last week remind us that monetary policy cannot “drop its guard”. Still, we are witnessing some growing concerns over the impact the ongoing acceleration in money creation could ultimately have on price stability. It is a minority view so far, with no effect on policymaking, but it could gain in strength as data start improving.

A short paper by Charles Goodhart in Vox1 makes the point in a nuanced and effective way. In his view, while for now the growth in money supply is offset by a collapse in the velocity of money which neutralises the inflationary impact, at some point velocity will normalise, bringing on risks of an inflationary backlash. Goodhart continues by debunking the usual counterargument, according to which “once we are there” monetary policy will also normalise, and central banks will be able to “lean against the wind”. It took in the past unusual political combinations – for instance in 1980 in the US – to successfully roll back inflation once it had set in. Charles Goodhart, both an academic and a former policymaker, is one of the “elder statesmen” of monetary economics. His views matter. They need to be carefully considered.

In the Euro area, the “broad money” aggregate M3 rose by 8.3%yoy in April, accelerating sharply from pre-pandemic 5.5% in February (Exhibit 4). This is by far the highest growth rate since the Great Financial Crisis of 2008/2009. The explanation behind this acceleration is very straightforward: credit origination has been very brisk since the beginning of the pandemic crisis, as we have already documented in Macrocast, with record flows of lending to corporations in March and April. Credit to the private sector contributed 4.8 points to the year-and-year growth rate in M3 in April, while 2.3 points came from lending to the government. Indeed, just like credit institutions create money by granting loans to businesses or households, they also do so when purchasing government bonds.

The latter has nothing to do with quantitative easing, at least not directly. It is the “normal way of things”. When banks are faced with uncertainty, they tend to rebalance their portfolio towards government debt (seen as a risk-free asset). What QE adds is to introduce a “structural”, not profit-seeking buyer of risk-free assets in the system which reduces the investible quantum and drives interest rates down. The central bank does not buy bonds from businesses of households, but from institutional investors. Those investors’ cash holdings rise with the proceeds of QE, but they tend to recycle them quickly in other non-monetary assets.

A first specific feature of the current configuration is that there is no sign of any “crowding out” effects: banks manage to both increase their lending to governments and to the private sector. This is made possible by the ECB’s action – in particular the new, very generous TLTROs – but also and maybe mainly by the governments’ decisions to pledge their own balance sheet by guaranteeing the emergency loans originated during the pandemic. In a nutshell they have abolished the difference in riskiness between investing in government bonds and lending to businesses (not fully though since in most cases the guarantee is lower than 100%).

A second specific feature is that the newly created money is not spent, at least not in net terms. So far, the fiscal stimulus funded by newly-issued government debt is a mere – and only partial – substitute to business spending which is not happening now. The best example of this are the temporary unemployment benefits through which the state pays wages instead of employers. At the same time, businesses tend to “hoard liquidity” and are drawing on their credit lines beyond their immediate needs to create buffers. Finally, households have been reduced into “forced saving” during the lockdown. This means that money supply is currently growing much faster than the number of transactions in the economy, proxied by nominal GDP. This is the very definition of a decline in the velocity of money, i.e. the number of times the same unit of money is used. In our estimate for Q2 we took the ECB’s forecast for GDP growth for the current quarter (-13%) and prolonged the April growth rate for M3 to May and June. Money velocity would fall by 22%yoy (see Exhibit 5).

The problem Goodhart focused on is the “exit strategy”. At some point, the velocity of money will normalise, as the economy exits lockdown. Then the full impact of the jump in money supply would show on inflationary pressure. While in theory we recognise this as a risk, in the present circumstances we are not as concerned as he is. Indeed, in our view it is likely that the normalisation in money velocity would coincide with a slowdown in net credit origination.

In the immediate pre-GFC days, the ECB was getting increasingly worried by the acceleration in M3 (Exhibit 3) – as its growth rate stood in 2-digit territory from December 2006 to May 2008. It was one of the reasons why the central bank maintained a tightening policy stance in mid-2008 despite the growing evidence the world economy had fallen into recession. But the nature of the acceleration in money supply was very different from the one we are witnessing right now. Then, the financial “machine” was in complete overdrive, with loans – in particular mortgages – being originated on the basis of unsustainable expectations on income and house prices.

Nothing could be more different today. Businesses are taking loans to offset the collapse in their cash flows, not because they expect strong conditions ahead. The biggest risk to the recovery in our view is not so much that credit overheats as we exit from lockdown, but rather that credit decelerates once the exit from lockdown is confirmed and businesses can rely again on at least a significant fraction of their cash flows. Note as well that in the Euro area most of these “emergency loans” have been granted with a fairly short maturity (typically between two and four years). Credit creates money. Paying back credit destroys money. Paying back short-term credit destroys money quickly. This will hold back net credit origination in the years ahead.

In addition, while businesses have been keen to leverage themselves these past two months, the opposite is true for households (they have paid back more than they have taken new loans in March and April). We would be surprised if households were to reverse course upon exiting from lockdown. With their employment prospects dimming, appetite for mortgages and consumer credit is likely to be subdued.

What will remain as a source of strong money creation? Extending credit to governments is a natural candidate, and we would expect a continuation at least into 2021 of a robust contribution from this counterpart to the growth in M3. But again, governments are substituting themselves to private spending at the moment, but it is unlikely to be a full substitution.

All in all, we would not be surprised to see money supply to return to a more sedate growth rate, possibly to the very low growth rates seen after the GFC. We would end up with a one-off level shift in M3, without lasting consequences for inflationary pressure even by the time the velocity of money normalises. It is of course possible that in the long term, central banks “fall asleep at the wheel” and, still shell-shocked by the brutality of pandemic crisis, fail to recognise times have changed and monetary conditions need to tighten. But for now, and probably for several years, the deflation risk is much more manifest, in our views.

Beware of institutional changes

The notion that “in the long run, inflation is a monetary phenomenon” has been drilled down in your humble servant’s brain during 12 years at Banque de France. But what is often ignored by the popular version of monetarism if that all the monetary policy mistakes Milton Friedman explored in his seminal book (“A monetary History of the United States”) are all episodes of excessive tightening by the Federal Reserve triggering deflationary risks.

Friedman’s ideas on the role of monetary policy and the control of money supply became mainstream in the 1970s when inflation had become rampant. But even though it took the brutal policy tightening of 1980 to regain price stability, it is not obvious that the prime cause of inflation in the previous decade was accommodative monetary policy. Central banks allowed inflation to get out control, but what was at the root of the acceleration in consumer prices was the institutional set-up of the time, in particular rigid wage/price indexation. The current institutional set-up is very different. Labour markets have been liberalised across advanced economies. The rigid rules which in the 1970s allowed mass unemployment to co-exist with excess inflation have disappeared. With more job losses ahead of us, it is unclear to us how a proper inflationary spiral could settle in. Moreover, beyond the labour market, the level of competition in services and product markets was markedly lower in the 1970s than today. International integration was a fraction of what it is today and monopolistic behaviour on national markets was rife.

Of course, institutional set-ups do change over time, and it is tempting to see in the pandemic crisis a watershed moment at which the “pendulum would swing back” and the liberalisation consensus of the 1980/1990s would give way to a re-regulation of our economies. We certainly see this as a plausible scenario, but it is not a foregone conclusion.

People across the world have rediscovered that fully-functional governments are a key asset in tough times, to deal with the immediate, sanitary aspects of the crisis but also to provide the ultimate backstop to avoid a complete economic meltdown. Governments everywhere are providing traditional stimulus measures – for instance a “good old” VAT rate cut coupled with cash handouts to families as per the new batch agreed by the German coalition we discussed in Macrocast last week – but again a key aspect of the ongoing public sector response is the pledge of its balance sheet through loan guarantees and in some cases equity stakes to shore up the private sector. In most cases, the potential liabilities incurred by the governments through this financial channel exceed by far their “ordinary” discretionary packages (Exhibit 6), even if these financial commitments are of a contingent nature whereas the “ordinary” measures will immediately impact public debt.

This is not exactly new in the sense that at the worst of the 2008-2009 Great Recession governments had to intervene directly to save the banks. There was a price to pay for this state bailout: regulation on banks was significantly tightened, which had a negative impact on their profitability. Could this pattern repeat for the entirety of the corporate sector this time? In principle, no. “Re-regulating” banks was essential to secure democratic support for the bailouts at the time, since it was the behaviour of the financial sector which was directly responsible for the 2008-2009 recession. This time the business sector including financial firms are clearly the victim of an exogenous shock.

Yet, the direct involvement of governments as guarantor, direct lender or equity investor may trigger some thorny dilemmas for political authorities, with potential lasting impacts on potential growth and inflation in the long run. Indeed, while in the aftermath of the Great Financial Crisis the governments’ goal was to re-regulate to avoid a new crisis in the future, this time a willingness to protect firms deemed strategic during the slump could “rigidify” our economies, by lowering competition intensity. In Europe, these risks are likely to be kept in check by the European Commission enforcing the Single Market rules, but conflicts will arise.

On 3 April and then on 8 May, the European Commission announced a relaxation of its state aid rules to help deal with the pandemic crisis, after having already endorsed EUR1.9tn in support to the business sector by member states. But crucially it also set several “red lines”. For instance, to guarantee the temporary nature of additional government involvement in firms ‘capital – in principle limited to six years – the remuneration owed to the state by the firms would rise over time to incentivise them to buy back the equity stake. Also, firms benefitting from the state’s entry in its capital are prevented from acquiring more than a 10% stake in their competitors. This would ensure that “national champions” cannot take advantage of government support to further increase their market power. Finally, member states cannot use the aid to support economic activities of “integrated companies that were in economic difficulties prior to 31 December 2019” although this may be difficult to establish objectively.

The recent case of Lutfhansa may provide some interesting early lessons. The German government is lending to the company (mainly via KfW), while also taking a “silent participation”, of which the majority will be treated as equity, on top of a more “traditional” equity stake of 20%, rising to 25% in case of hostile take-over. The financial structure itself is compliant with the European Commission’s rulebook. For instance, the dividend on the silent participation would become gradually punitive (from 4.5% in 2020/21 to 9.5% by 2027). But a thorny issue arose with the Commission’s request for Lufthansa to release some landing slots from Munich and Frankfurt airports to “offset” state aid to a national champion with a higher degree of competition. After an initial rejection by the board of Lufthansa, an agreement was finally found on the release of 24 slots in each of the airports. However, for the first 18 months, these slots will be open only to new competitors, i.e. firms that do not yet operate in these two hubs, which will make it difficult for the two leading low-cost companies (EasyJet and Ryanair) to bid.

Some comments from German politicians at the time of the negotiations were quite interesting. The Prime Minister of Bavaria for instance expressed concerns that low-cost operators would offer less secure jobs. This encapsulates the difficulties in which governments may find themselves after expanding their direct role in strategic corporations. With the equity stakes comes political responsibility in the eyes of the electorate. It will be difficult to act as an “ordinary shareholder” and tempting to offer a high level of protection, to the detriment of competition within the single market.

For the time being, there is no evidence of widespread re-regulation and this would not affect our firm belief that for the foreseeable horizon this crisis is deflationary, and not inflationary. But we think policy discussions will increasingly focus on the regulation topic once we work our way through what could be a quite bumpy recovery.

- 4oCcSW5mbGF0aW9uIGFmdGVyIHRoZSBwYW5kZW1pYzogVGhlb3J5IGFuZCBwcmFjdGljZeKAnS4gVm94LCAxMyBKdW5lIDIwMjA=

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.