Inflation Review: The "greedy beast" of inflation is still breathing, in particular in services

- 09 February 2024 (5 min read)

Key points:

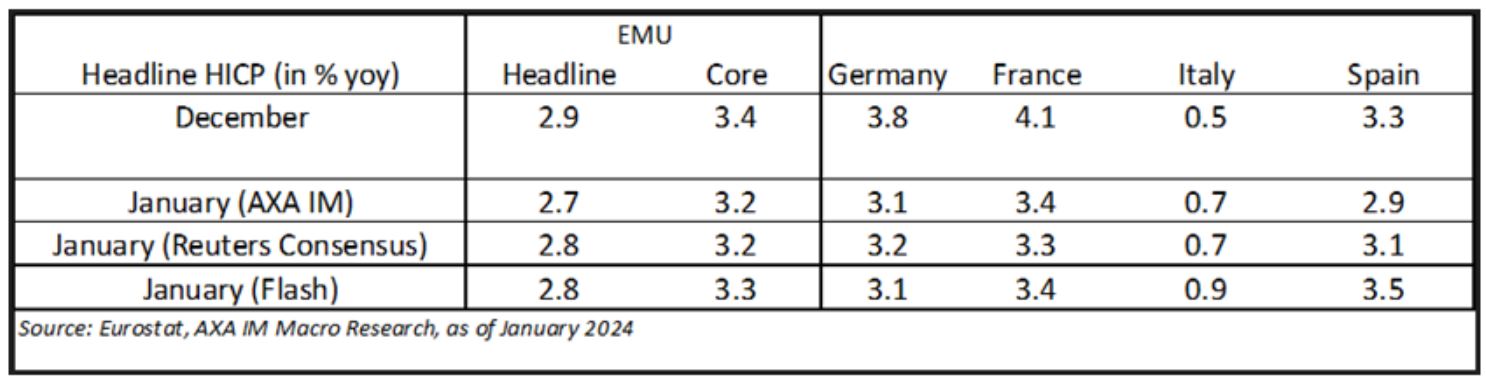

- Both euro area headline and core inflation dropped by 0.1 point, respectively to 2.8% y/y and 3.3%, slightly above consensus expectations

- At face value, these are good news. But services inflation is stickier, being flat at 4% for the third successive month.

- We believe it will only reinforce ECB's dependence towards data, in particular on services prices and wage data, while keeping an eye on other components subjected to upside risks from tensions in the Middle East.

Euro area headline inflation decelerated to 2.8% y/y in January (-0.1 percentage point from December), slightly above our forecast (2.7%) but in line with consensus.

Core inflation dropped to 3.3% y/y, 0.1 pp below December level, but slightly above our forecast and consensus (3.2%). Crucially, the decline was only driven by non-energy industrial goods (NEIG) (2.0% y/y; -0.5pp from December), while services prices were flat at 4.0% for the 3rd successive month. Energy prices were a bit stronger than our forecast, declining by only -6.3% y/y (+0.9% on a monthly basis). Food alcohol and tobacco (FAT) came at 5.7% y/y, in line with our forecasts. Processed and unprocessed food continued to decelerate, respectively at 5.7% and 5.3%.

Services prices are flat at 4% (again), likely to maintain the ECB on the cautious side

Putting us in the ECB's shoes, this January print doesn't change much. At face value, both headline and core inflation decelerated, despite several measures of support, deployed during the energy crisis, being removed. The ECB probably pencilled in a stronger inflation in January as they were forecasting 2.9% on average for Q1 2024 while January is our highest monthly print. The big picture is (ever so slightly) improving but services momentum isn't.

The ECB cares much more about services inflation which now accounts for 44.5% of total inflation basket. The latter came at 4.0% y/y, at the same level for three successive months. Looking at the monthly pace (-0.1%), it is the same than January 2023 and 2022, largely above average of 2015-2020 (-0.6% m/m). It is partially explained by some increasing taxes such as in VAT for German restaurants or package holidays methodological changes, but the difference is noteworthy. That means companies continue to hike prices at a significant pace. The reasons behind such pricing behaviour are probably to be matched with past inflation, wages anticipations and resilient corporate profit margins.

Wage growth is also key for the ECB. Some figures surrounding ongoing wage negotiations seem high, in particular in Germany or in the Netherlands (negotiated wages just came out at 6.9% y/y, flat from December). After 4.4% in Q2 2023 and 4.7% in Q3, we forecast EMU negotiated wages to reach 4.4% in Q4. We can't exclude something a bit higher, in particular after the surge of hourly wages in Italy in December (7.9% y/y in Q4, from 2.7%). A large part of it is an artefact as it reflects an advance payment, but it will mechanically boost the aggregated index.

Last but not least, we fear components which are currently driving down inflation, may face upside risks as tensions in the Red sea and in the Middle East have not faded and its impact on good and possibly food prices are yet to be seen. Some studies are pointing to an impact worth of 0.1-0.2 pp on core inflation from doubling shipping cost.

There is more to learn from the final January release

Preliminary data give … preliminary conclusions but everything else equal, weight changes are likely to boost inflation figures in 2024. Indeed, services weight rose to 44.5% (+1.3 p) while the other majors components declined (NEIG to 25.70% (-0.57 p), FAT to 19.47% (-0.51p) and energy (9.94% (-0.29 p). Nowadays, services inflation is the stickier component, so rising weight push inflation on the upside. Lower weights from components with downward price pressures also lower their contribution. It is likely to boost average inflation by some bps in 2024. We will have full details for items and countries by February 22.

Another interesting details will be to look at industries usually keen to increase their prices during January. It is around 15% of the basket (excluding energy, fresh food), twice the usual monthly rate and mostly concentrated on services like insurance products, subscriptions…etc (source: "New facts on consumer price rigidity in the euro area", E.Gautier & al. Sep 2023). Their pricing behaviour consider what happened last year but also what they expect for this year and in particular labour cost.

January inflation figures have been only slightly stronger so there are no reasons to adjust our forecasts yet, in particular as we need to see final weights for countries and items. The only change we've made is removing the normalisation of monthly train ticket in Germany. In fact, we were pencilling in a large increase this year, but the government recently extended the measure into 2024. The latter had a significant impact on our forecasts. We lower accordingly our euro area core inflation by approximately 0.15pt on average for 2024 and 0.1pt for headline. We now project both headline and core at 2.5% for 2024 and 2.1% for 2025 (also for both headline and core).

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved