Changing our Climate

Our goal is to encourage our investee companies towards a more sustainable future.

Proactive engagement in Oil & Gas

We notably focus on climate change and biodiversity loss, two global emergencies that require urgent action. We also engage regularly on corporate-governance related issues, which reflects the increasing importance that companies are placing on ESG.

In this case study, we outline how this looks in practice for two Oil & Gas companies, and how our on-going dialogue with companies influences how we vote during their respective AGMs.

The Investee Companies

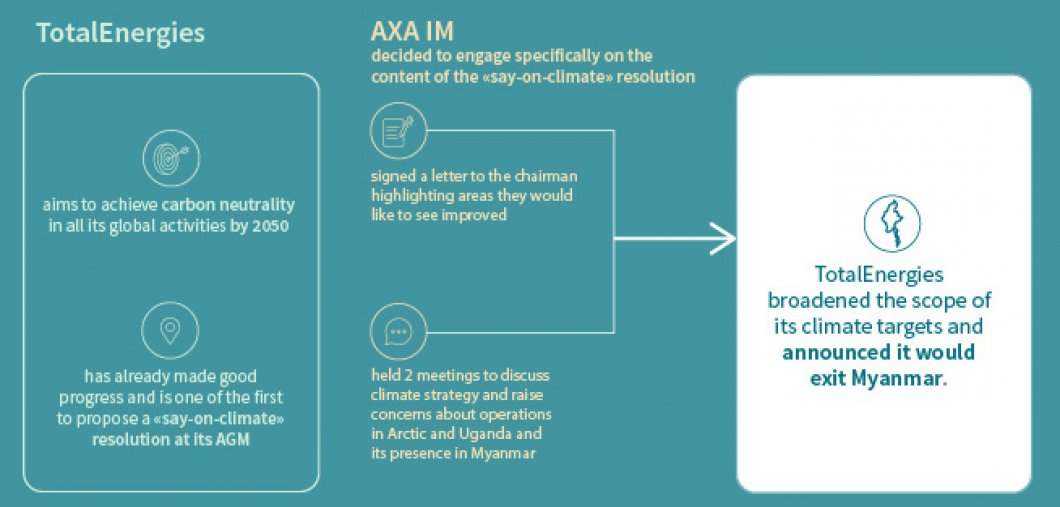

TotalEnergies, a French multinational integrated oil and gas company, is one of the seven “supermajor” oil companies. It aims to be a world-class player in the energy transition and achieve carbon neutrality in all its global activities by 2050.

TotalEnergies has already made good progress on setting and meeting climate related targets. It submitted its first Say on Climate resolution at its 2021 AGM, which was supported by 91.8% of shareholders, including AXA IM and AXA. The company has presented a progress report during its 2022 AGM. Total has one of the most convincing strategies among the oil and gas majors, according to AXA IM’s Oil and Gas Paper.

Chevron is an American multinational energy corporation. Headquartered in California, it is one of the world’s largest oil and gas integrated companies, with activities spanning the entire value chain, from refining to chemicals and distribution.

In contrast, Chevron’s energy transition strategies is not as demanding relative to is main peers, BP, Shell and TotalEnergies in Europe. While all its peers have goals to achieve net zero by 2050 for their scope 1 and 2 operations and for their entire activities, Chevron is limiting this goal to its upstream business, excluding all downstream operations. Chevron is yet to take scope 3 emissions into account, and as a result its targets to reduce emission intensity of its energy sales between 2016-28 are not as ambitious as other companies in the industry who are factoring scope 3 into their plans. All Chevron’s European peers have a net zero by 2050 ambition for their scope 3 and intermediary targets. Chevron is more credible when it comes to developing low carbon products such as biofuels, hydrogen and renewable gas, although its peers are pursuing the same avenues. But Chevron, unlike all its European peers, is not planning on developing a renewable electricity business. Overall, although Chevron has improved its energy transition strategy over the past two years, it is still some way behind the industry leaders in its strategy.

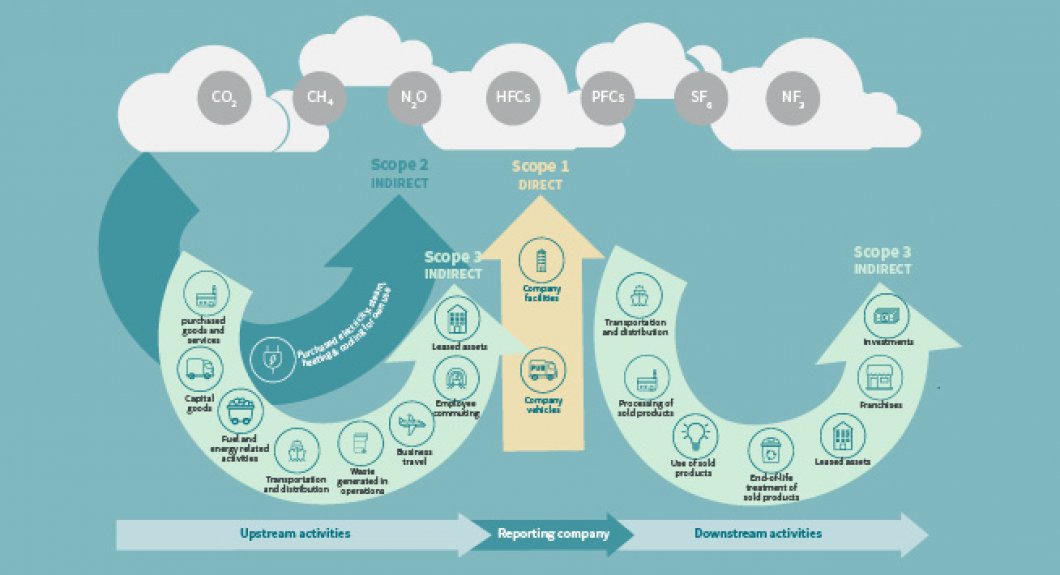

Measuring scope 1,2&3 for the Oil and Gas industry

The Approach

AXA IM regularly engages with TotalEnergies and held four individual engagement meetings with the company in 2021, including one ahead of the 2021 AGM and another to focus on the group’s strategy for Nature Based Solutions. AXA IM held another two meetings in 2022: one with the CFO and one to specifically discuss the progress report presented to the shareholders during the 2022 AGM. It decided to use two tools to gain maximum effect.

Firstly, in 2021, AXA IM decided to engage specifically on the content of the Say On Climate resolution. AXA IM worked with Climate Action 100+ and signed a statement prepared ahead of the AGM that year. Secondly the team requested and held meetings to discuss the details of the company’s climate strategy and raise concerns about its operations in the Arctic and Uganda and its presence in Myanmar.

On this basis, at the 2022 AGM, AXA IM is supporting the progress report presented by TotalEnergies’ management and will continue to engage regularly to ensure the company progresses in a timely manner in its climate journey.

At Chevron’s 2021 AGM, a shareholder proposal asked the company to reduce its Scope 3 emissions. This received the support of 60.7% of votes cast, including AXA IM’s, and was adopted. Despite this, the company considered that the reduction of scope 3 emissions would clash with its business strategy, which aims to decrease carbon intensity while increasing oil and gas production.

Chevron is making some investments in low-carbon technologies, but it is unlikely that its plans will lead to an absolute reduction in GHG emissions that is consistent with a “substantial reduction in scope 3 emissions” and thus a limitation of warming to below 2°C. Given this, at the 2022 AGM, AXA IM plans to support a vote of no confidence against the directors of the public policy and sustainability committee.

AXA IM also plans to support the vote against the chairman and the lead independent director for not taking the necessary measures in their company to limit global warming to below 2C. In addition to this, AXA IM plans to vote for a shareholder resolution asking Chevron to adopt medium and long-term GHG emissions reduction targets. It will also vote in favour of asking Chevron to issue a report assured by an independent auditor on a net-zero scenario analysis and a report summarising the company’s efforts to measure methane emissions.

Finally, it will vote for a resolution that Chevron oversee and report on a racial equity audit.

Key Results and Changes

Between September 2021 and March 2022, TotalEnergies broadened the scope of its climate targets, committed to improve transparency (notably on capex) and to an annual vote on its Progress Report. In addition, in January 2022, it announced it would exit Myanmar. It is likely these moves were a direct result of pressure from investors, including AXA IM.

AXA IM’s experience at Chevron is somewhat different. Chevron has resisted addressing concerns raised by shareholders around its climate policies. Instead, it is focusing on its business strategy to increase oil and gas production. This attitude reflects a growing trans-Atlantic rift when it comes to the oil industry’s response to climate change.

TotalEnergies and AXA IM engagement on climate resolution

Next Steps and Learnings

The dialogue continues with TotalEnergies on two main aspects, its production profile and the use of Nature Based Solutions. As for production, NGOs refer to the International Energy Agency’s net zero 1.5°C scenario, which concludes that no new oil and gas greenfields are needed. As TotalEnergies and many of its peers are developing new oil & gas fields, this makes for a a red line for those same NGOs. It is worth highlighting that TotalEnergies does aim for a reduction of its oil and gas production of 80% by 2050, but mostly post 2030. Another dimension of our engagement with them will also be on shareholder dialogue practices.

This is an important area to discuss with oil and gas companies. We believe the equation around production is complex and should encompass a demand criteria to avoid any dramatic increase in energy prices should supply be cut independently of demand and technological developments. We need to take a holistic perspective, allowing for a shift from oil to gas in this transition period to 2030.

According to the Climate Action 100+ group, Chevron does not meet the criteria for alignment with net zero by 2050. In AXA IM’s view, the targets the company set itself for reducing emissions are not sufficiently binding. In addition, not enough spending is being allocated to alternative fuels and technologies to reduce oil and gas demand. As a result of this, AXA IM decided not to support the management.

Stewardship and engagement

Our engagement to drive action and create meaningful impact.

Learn more

Disclaimer

Companies shown are for illustrative purposes only. It does not constitute investment research or financial analysis relating to transactions in financial instruments, nor does it constitute an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.