Long-term investing: Buying at the dip

- 04 June 2025 (3 min read)

Even during the relatively short period since the start of this century, there have been numerous severe market sell-offs. From the tech bubble of 2000-2002 when the S&P 500 fell by 49%, 9/11, the global financial crisis of 2007-2009, the Brexit vote in 2016 to more recent shocks such as the global pandemic shutdown, the war in Ukraine and US President Donald Trump’s trade tariffs, investor confidence has been shaken. With the value of hindsight though, markets have always recovered.

In the face of a severe market sell-off, many investors may be mindful of the saying “this time it’s different” and be tempted to exit their positions. However, market evidence shows that such a move has been historically detrimental. Markets rebound and almost a century’s worth of US data up to 2011 shows that a 20-year holding period in US equities never delivered a negative return.

There can often be attractive buying opportunities following market corrections. Whilst considering such an approach shortly after a market fall may be daunting, investors should remember that there exists the chance to take advantage of potential excess returns.

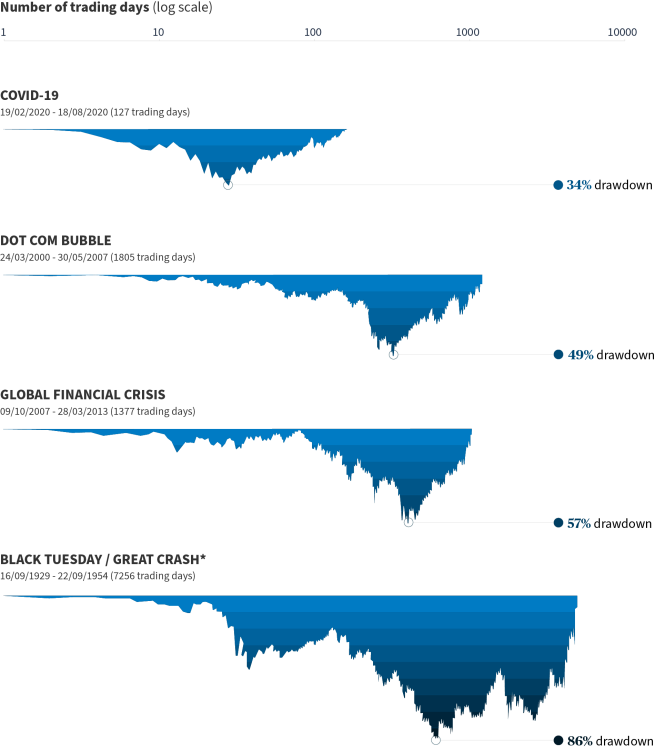

Market sell-offs

The chart below highlights how long major market sell-offs have lasted, and the comparable percentage drawdowns in the S&P 500.

If there is one takeaway from index corrections, it is that no matter how severe or bleak prospects appear at the time, markets do recover, eventually. In other words, market sell-offs are followed by upturns.

Investors in broad, well-diversified portfolios, who stay invested or even purchase more shares when prices are low and sentiment is weak can potentially experience lesser adverse effects on their portfolio than those who sell during the downturn and attempt to time their return to the market.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved