Multi-Asset Investments Views: We all live in America (but investors can travel)

KEY POINTS

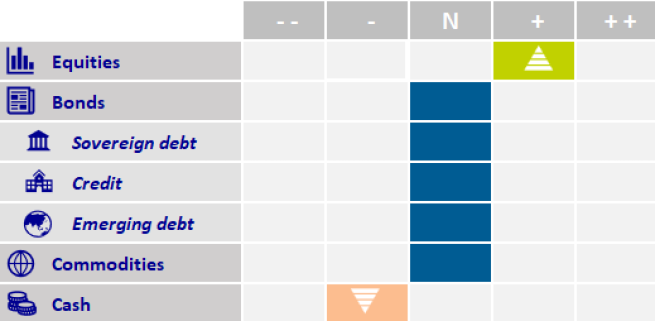

Equity investors’ patience has been rewarded, as markets comfortably navigated August’s introduction of the new US tariff regime. Consequently, indicators of trade policy uncertainty have normalised. The second quarter (Q2) earnings season proved to be globally positive and once again exemplified the US economy’s resilience, although earnings that missed expectations were heavily sanctioned by investors. The macroeconomic backdrop further fueled convictions that the Federal Reserve (Fed) would be in a position to cut rates in September as well as in December. We continue to hold an overweight in risk exposure.

Despite July’s Fed policy meeting minutes striking a hawkish tone investors have since focused on a September rate cut, as signs of weakness were seen in both jobs data at the start of August and in heavily negative revisions to previous numbers. Fed board members are shifting their attention away from sticky inflation to potential labour market weakness.

Fed Chair Jerome Powell emphasised in the opening paragraphs of his speech at the Jackson Hole economic policy symposium that “the balance of risks appeared to be shifting”, potentially warranting a policy adjustment. He did however underline the Fed board’s independence and data dependency which are key for confidence in the US dollar and US Treasury market. We are wary of any further steepening in global yield curves led by weakness in long-dated bonds and are not in a hurry to add duration in this area. We maintain our target of 1.20 for the euro/dollar exchange rate and thus remain US dollar sellers.

Meanwhile, European Central Bank (ECB) President Christine Lagarde’s tone has softened regarding weakening Eurozone activity expected through Q2 and Q3. Hawkish ECB policymakers have dismissed such concerns and maintain the ECB is likely done with rate cuts. The market now is pricing less than one cut before year end which may prove to be overly cautious. We are positive on two-year German bonds (Bunds) and have a preference for Bunds over US Treasuries, but only when we have seen a further shake-out in the long end of the US yield curve due to the overriding influence of the US market on most other interest rate markets.

In the run-up to the Jackson Hole symposium we adjusted our derivatives holdings in our equity overlay strategy. The short position on US small caps versus the Nasdaq index was closed due to extreme short investor positioning on the Russell 2000 index futures. Some exposure was also reallocated from US large caps to Eurozone equity indices to diversify risk and reduce the heavy concentration in the US assets inherent in global strategies. It’s worth noting that even in the perennially dominant US Treasury market, foreign participation is falling from 70% pre-COVID-19 to 64% currently1 and price concessions demanded by local dealers at auctions to make up the shortfall is rising.

- Source: US Treasury statistics

Despite our intention to favour more diversification into European assets there remains a source of stress from the political environment in France which needs to be addressed. To this end we have initiated positions to reduce our exposure, with a long German MDAX (mid-cap) index versus short CAC 40 trade in equity indices and a long Bund 10-year versus French OAT 10-year position in bond futures. The end-of-summer rentrée is shaping up to be a period of political and social tension for France and this is likely to be reflected in equity underperformance, especially given the high concentration of financials in the CAC 40, and a widening of government bond spreads.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

Image Source: Getty Images

© 2025 AXA Investment Managers. All rights reserved