Investing for net zero: How fixed income investors can apply a sustainability framework

KEY POINTS

Investors have a vital role to play in securing a sustainable future for both people and the planet, by supporting the transition to net zero.

They can do this by investing in companies with robust net zero alignment plans, or by channelling their capital towards solutions that are helping to drive a positive impact for the environment and society at large.

Fundamentally, there are a range of significant and compelling reasons why we believe institutional fixed income investors should consider integrating sustainability into their portfolios.

First, there is strategic importance. Fixed income investments are often large, long-term, strategic allocations, meaning the impact of any sustainability risks, and the positive impact from becoming more sustainable, are heightened. In addition, the longer time horizon over which many sustainability themes are expected to emerge is often closely aligned to the maturity of fixed income allocations.

Secondly, there’s risk mitigation. Fixed income strategies are frequently designed to reduce risk as part of a broader portfolio. This means that bond investors need to consider a wide range of risks, including environmental, social, and governance (ESG) factors.

And third, it’s about being agile as fixed income offers a large investible universe via a range of strategies and instruments, giving investors scope to seek out opportunities that fit with both their sustainability and long-term financial objectives.

Integrating sustainability into fixed income portfolios

There are five key methods through which sustainability can be integrated within fixed income portfolios. These are:

- Decarbonisation

- Net zero alignment

- Green, social and sustainability bonds

- Engagement

- Exclusions

These methods go over and above traditional ESG integration – incorporating ESG risk analysis into investment decisions - which is a standard part of the day-to-day financial management of portfolios.

These five methods can be targeted individually but are most often combined in a bid to achieve the optimum financial and non-financial outcomes.

Below, we explain how they can potentially help institutional investors.

Decarbonisation

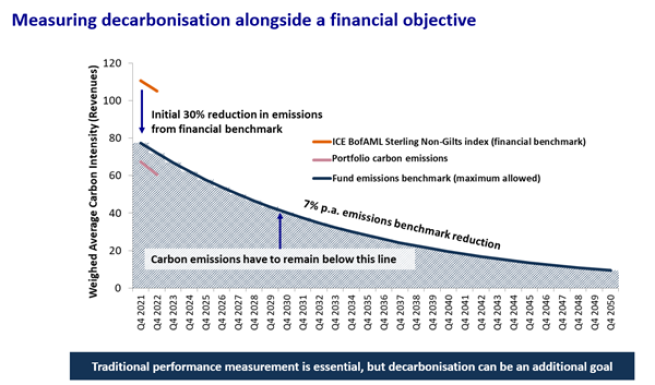

A common objective for many investors is to reduce their portfolio’s carbon emissions, while simultaneously aligning with wider fund-level financial objectives. This can be through explicit decarbonisation objectives, such as a 50% reduction in emissions by 2030, or a target that seeks to reduce emissions to net zero by 2050. A decarbonisation objective can be a simple metric to manage and monitor by both the asset manager and asset owner.

The chart below shows an example of how investors may set a decarbonisation objective by using a carbon emissions ceiling. The starting point is the carbon intensity of the financial benchmark, targeting an initial 30% reduction in emissions from that level, then a 7% year-on-year reduction thereafter. This creates a carbon emissions ceiling with the aim of keeping portfolio emissions below a certain level.

When integrating a decarbonisation objective into fixed income portfolios, investors must consider the specifics of the fixed income strategy. For example, portfolio-level carbon emissions can fluctuate significantly in short-dated strategies when issuers fall out of the investment universe or bonds mature, as a greater proportion of bonds mature each year compared to longer-duration strategies. Strategies with smaller investment universes (e.g. UK credit) may see a high concentration of emissions within only a handful of issuers and sectors, thus heavily influencing both portfolio and benchmark emissions.

Net zero alignment

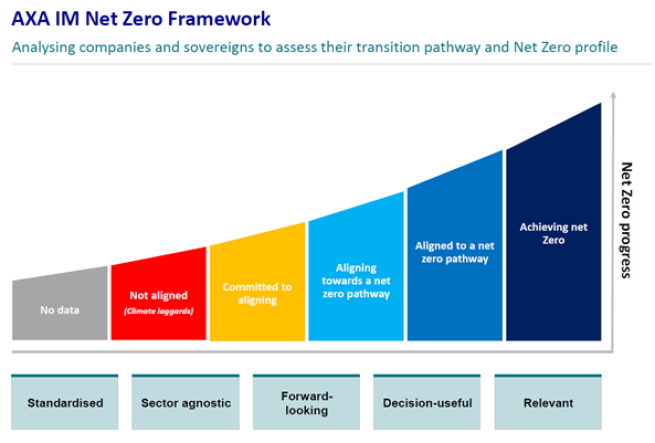

While global decarbonisation is often the end goal, focusing on portfolio-level alignment is a forward-looking approach to climate change rather than one looking at historical emissions.

At AXA IM, we use the Institutional Investors Group on Climate Change (IIGCC) Net Zero Investment Framework (NZIF)1 to assess issuers’ net zero alignment. Our quantitative analysis draws in a large array of data points from various sources and provides coverage for the entire investible universe while our qualitative analysis is undertaken by the analysts closest to each issuer, so they can fully integrate all issuer- and sector-level specificities which may impact achieving net zero.

We believe that net zero alignment is preferable to a simple decarbonisation approach because it is:

- Standardised – allowing aggregation of results across multiple portfolios

- Sector agnostic – removing financial biases when building portfolios

- Forward-looking – compared to one-to-two-years old carbon emissions data

- Relevant – to achieve portfolio and real-world decarbonisation

- Decision-useful – thanks to our robust analysis we can make portfolio-level decisions based on this data.

- {https://www.iigcc.org/hubfs/nzif/pdf/IGOT%20master.pdf;Net Zero Investment Framework: Implementation Guidance for Objectives and Targets, IIGCC}

Within our net zero-focused portfolios, we seek to increase the alignment of the portfolio over time, due to the limited number of issuers with zero emissions today.

The IIGCC’s framework aims for 100% of assets to be considered at least ‘aligned’ to a net zero pathway by 2040 and 100% at net zero by 2050. Clients often have intermediate goals and, in our experience, many have been looking to increase the data coverage in their portfolios and reduce the exposure to climate laggards, either through exclusions or by not re-investing.

The net zero journey will not be uniform across sectors and regions, something our assessment framework takes into account. For example, emerging market sovereigns are exempt from some of the criteria required from the NZIF, so as not to disadvantage issuers in those markets, and to support their important transition to net zero.

Green, social and sustainability bonds

Reaching net zero requires a great deal of investment – and one way that we can help finance environmental solutions is by investing in companies that create the products and services, enabling other businesses to decarbonise or support initiatives focused on renewable energy, preventing pollution or protecting biodiversity.

Green, social and sustainability bonds (GSSBs) allow investors to purchase debt securities earmarked for projects with a positive environmental, social or sustainable aim, and are becoming increasingly standardised, transparent and credible as an asset class. GSSBs can play an important role in contributing to a portfolio’s sustainability profile and providing a positive net impact.

The size of the GSSB market is now similar to the euro investment-grade credit sector, at around €3trn.2 This means that the GSSB universe is mature enough for investors to build diversified portfolios that invest dynamically across asset classes, sectors and regions, rather than being a niche allocation. Alternatively, investors can have an allocation to GSSBs within a wider fixed income portfolio.

Engagement

Fixed income investors are in a unique position to be able to drive change through engagement, encouraging more sustainable policies from the issuers in which they invest.

The size of the fixed income universe and the opportunity to interact with issuers not available to investors in other asset classes, for example sovereigns, quasi-sovereigns and private companies, is an opportunity for investors to work towards making a difference.

While we believe all fixed income strategies should benefit from active engagement, those with a longer-term horizon, such as Buy and Maintain, can track engagement progress from the outset to engagement completion over a 24 to 36-month time frame while also bringing the scale of an institutional asset base to the engagement table.

Exclusions

At its simplest level, investing sustainably means excluding certain holdings based on certain risks, including climate risks, controversial weapons, deforestation and more. For many investors, this will be how they started their sustainability journey, screening to mitigate the potential risk on portfolio performance, or to exclude issuers that have a large negative impact on the wider world, either environmentally or socially.

However, investing sustainably involves much more than exclusions, and in our view should be embedded into the investment philosophy as well as business practices and culture.

As with the other sustainability integration methods, a pragmatic approach must be taken with exclusions, particularly with sovereign investments. For example, institutional investors with Liability-Driven Investment portfolios could find it challenging to exclude sovereign issuers which fulfil an important risk management function, and active Aggregate-style allocations would be unable to exclude a large proportion of their investible universe without potentially causing excessive tracking error risks and reducing an important source of alpha. Credit strategies, by contrast, typically have a broader investible universe meaning targeted exclusions can be offset by reallocating within the same sector to maintain the required financial characteristics.

A challenging but essential pathway

The road to net zero is challenging and requires a collective effort from individuals, companies and governments. We believe that investors can play an important role in both committing to, and implementing, a net zero approach in their investment strategies to build a sustainable bond portfolio.

A net-zero aligned portfolio can help investors manage sustainability-related risks while accessing a range of instruments across a diversified investment universe, seeking out opportunities that target decarbonisation alongside a financial objective. In this way, investors can aim to build stable and prosperous portfolios – and contribute towards a stable and flourishing world.

- Based on ICE index data, as of 31 March 2025

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved