Bonds, I presume?

Bond bearishness continues, but the market is not doing much beyond reacting to supply and demand, alongside the usual flow of economic data, and expectations about central banks. My view is we are in a different regime to the interest rate-resetting years of 2022-2024. It’s more of a bond-normal regime. Curve steepening is cyclical and will probably extend further with more rate cuts. Yes, there are concerns about inflation and fiscal balances, but that might all be priced in. The big bond losses are potentially behind us and today the fixed income markets are doing what they are supposed to – provide income with a total return volatility that is typically a third that of equities.

- I still like short duration credit, inflation-linked bonds, high yield, and increasingly gilts

- I’m worried about US equities, interference with the Federal Reserve, and the noise around gilts

Rates regime reset

Long-term government yields have continued to rise and yield curves continue to steepen. The trend started in early 2022 with the pivot towards tighter monetary policy in response to the post-pandemic inflation shock. However, the trend has extended beyond the tightening cycle, with yields rising even as central banks have been cutting rates. Monetary policy expectations drive the short end of yield curves. The decline in global inflation rates since 2022 has allowed central banks to ease, a process that the market expects to continue, at least in the US and in the UK (Europe has already done a lot). What drives the long end are expectations on growth and inflation, and premiums related to fiscal policy, as well as other risks, such as not meeting an inflation target. In the US and UK, inflation has not fallen back enough and fiscal concerns have come more into focus. Hence, curve steepening and some over-dramatic commentary on the future of borrowing costs, public debts and bond pricing.

Dramatically ordinary

In the UK, 92% of the increase in the 10-year government bond (gilt) yield between early 2022 and today happened during the period when the Bank of England took the policy rate from 0.1% to 5.25%. For the 30-year maturity, 79% of the increase in yields between early 2022 and now happened during that policy tightening period. It has been a very similar story in other markets. In 2025, the 10-year gilt has traded within a 46 basis points (bp) range, with the 30-year in a 67bp range. For the US market the ranges have been 80bp and 68bp respectively, and in Germany, 53bp and 81bp. For the whole of 2024, the 30-year yield trading ranges were 104bp, 89bp and 55bp for the UK, US and German markets respectively.

Risk premium steepening

Globally, long yields have risen relative to short rates even with central banks easing. But in terms of volatility, there is nothing unusual about the range of trading in bond markets in 2025 (in September 2022 alone, the range for the 30-year gilt yield was 180bp). But the UK has underperformed. With several changes of prime minister in recent years and, since July 2024, a new government, the market is not convinced that UK policies can deliver a more stable outlook for public finances. If the UK government were to borrow by issuing 30-year bonds today, it would pay 72bp more than if the US government did the same. Good job it isn’t then. Indeed, it does not need to. This week the Debt Management Office cancelled a scheduled auction for 30-year bonds. But it did borrow by issuing 10-year gilts, raising £14bn at a yield of around 4.86% (the order book reached £140bn, showing that higher yields do attract demand from investors). There was no evidence of investors panicking or avoiding buying UK government paper.

Eyes on Reeves

The UK government announced its next fiscal event, the 2025 Budget, will be presented on 26 November. That is later than expected and shows the government needs more time to decide what to do with taxes. Until there is more clarity, gilts could continue to underperform other bond markets. However, a Federal Reserve (Fed) rate cut, or weaker US employment data would allow gilt yields to fall as part of a global response. At any rate, 30-year yields at 5.8% are attractive in my view and the government has shown it has no need to lock into that maturity at these borrowing costs. Outstanding gilts with over 15 years’ maturity now make up just 29% of the total conventional gilt market; that was nearly 50% in 2020. The other bit of potentially good news is that UK growth data has been a bit stronger of late. If there is any change in the Office for Budget Responsibility’s forecasts, there could be some easing of pressure on the fiscal outlook – on a rolling 12-month basis, government cash receipts (taxes) have been increasing by over 7% year on year.

Regime of normal

Global bond yields are not far off what a simple model based on a moving average of nominal GDP growth would suggest. The US is at fair value, as is France; Germany is expensive, and the UK is on the cheap side. It is easy to forget that for a long time, bond yields were kept low by financial repression, and it is only in the last two years they have reverted to more neutral levels. Moreover, yield curve steepening is perfectly understandable. The unusual thing in recent years was the inversion of yield curves – as recently as June 2023, the US 10-year Treasury yield was 100bp lower than the two-year yield. A positive curve gap of between zero and 250bp has been the norm for the best part of the last four decades, and fixed income 101 suggests it is ‘normal’ for curves to slope positively as investors should receive more yield for giving up money for longer. There is more steepening to come in the months ahead – especially if the August US employment report prompts the Fed into cutting by 50bp.

Growth and income in 2025

This year, across fixed income markets, most total returns have come from income. High yield and emerging market debt have been the best sectors for income generation. Long-duration government bonds have best been avoided because, despite some income, price action has been negative. The over 15-year US Treasury index, for example, has a 2.64% income return to date and a 0.68% decline in price return. For long gilts it has been much worse – 2.6% from income but -7.3% from price. The sweet spot has been in short-duration credit strategies or in floating rate asset-backed securities. Growth has come from US equities; European markets have also delivered some growth and decent dividend income. For the balance of the year, short-duration credit and European equity exposure should potentially continue to perform in a similar way.

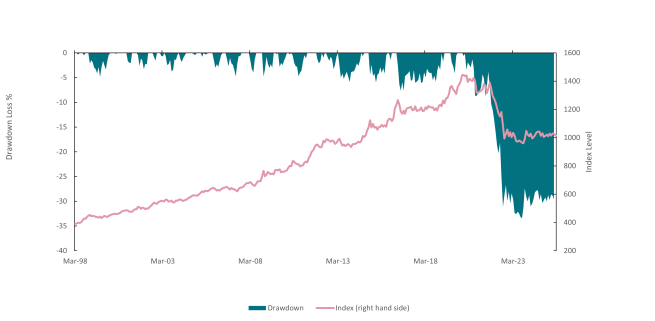

Horses bolted

The final word is about bond bearishness. Concerns about global fiscal trends are legitimate. But there seems to be a misunderstanding about where we are in bond markets. The 2022-2024 period was a rate reset regime. That is when the money was lost. Since then, we are in a bond-normal regime where a lot of time is spent trying to observe the unobservable (term premium, neutral rates, etc.) rather than accepting the cyclical dynamics. The chart below is the drawdown chart for the UK Gilt index. Passive investors in gilts lost more than 30% from the peak and those losses have not been eroded. But the point is that the bulk of this happened in 2022. To lose another 30%, the market yield would need to go to 9%. And I certainly would bet against that happening.

Performance data/data sources: LSEG Workspace DataStream, ICE Data Services, Bloomberg, AXA IM, as of 3 September 2025, unless otherwise stated). Past performance should not be seen as a guide to future returns.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.