Multi-Asset Investments Views: Give me reason, take me higher

KEY POINTS

Investors’ focus has shifted away from idiosyncratic credit market problems to the Federal Reserve’s (Fed) policy outlook following the end of the US government shutdown. In essence, the end of the 40 days in the wilderness is positive for our policy and markets outlook, albeit with one caveat. In the absence of much fresh labour market data for the Fed to consider at its December meeting, several members of the central bank’s board have expressed a need for pragmatism and more time before they will vote for a further Fed Funds Rate reduction.

The data which has been available has been relatively comforting: while the labour market remains weak, it did not significantly deteriorate during the shutdown. Should a December interest rate cut be delayed, January appears likely. But we believe the Fed is justifiably ‘playing by the book’ to ensure its credibility, as well as that of the US dollar and US Treasury market, all remain solid. Investors should not yet extrapolate that the Fed is walking back on the three near-term rate cuts that its forecasting ‘dot plot’ indicated in September.

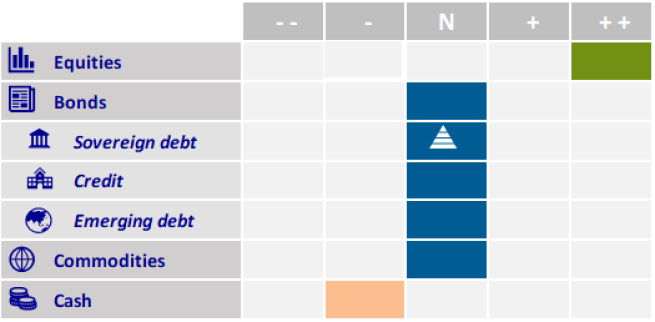

We have increased our allocation to equities, as the current environment remains supportive for risk markets. The earnings season was a resounding success on both sides of the Atlantic, albeit to differing degrees. Potential policy accommodation from the Fed has merely been delayed. The little macroeconomic data available, complemented by private-sourced alternative data, has not indicated a slowdown in activity. The Atlanta Fed’s ‘nowcast’ for US GDP growth is even cruising close to 4% on an annualised basis. In Europe, survey data has held up despite a persistent risk of a more challenging deflationary environment in its largest economies.

Further to the supportive macroeconomic and central bank policy elements, we are also encouraged by our reading of investor positioning. Discretionary investors remain below their long-term neutral allocations to equities, whilst falling systematic investor positioning should eventually prove positive as it was stretched especially in relative terms. Nonetheless, cross-market volatility will need to abate over the near term. Structurally, our machine learning-powered Bull/Bear model indicates that we remain in a bull market, uninterrupted since the US policy turnaround in late April.

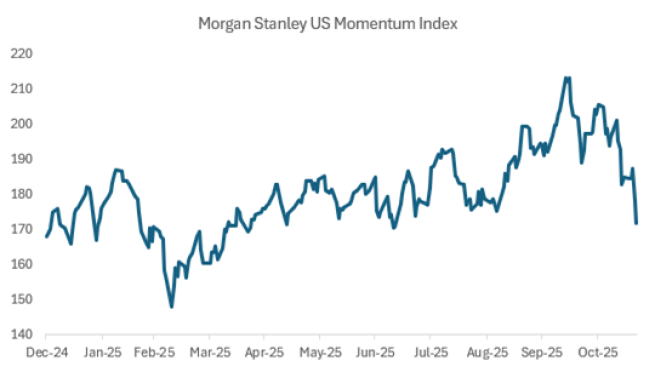

Although difficult to rigorously quantify, we believe Bitcoin’s severe correction (-33% from early October to late November) and other crypto assets may have contributed to the rise in risk aversion in the equity market. Indeed, even if only 0.4% of institutional cash is invested in such crypto assets (according to the Bank of America November 2025 Fund Manager Survey), US retail investors are more heavily exposed. This may have deprived listed markets of the usual retail dip buyers who have been unseasonally absent in recent weeks. If anything, we take comfort that retail-favoured ‘momentum’ stocks - those which have had a positive price change relative to the market - seem to have troughed at a depressed level, consistent with previous instances earlier this year.

Meanwhile, we remain neutral (structurally invested) on credit, as we prefer to concentrate our risk-taking within equities. It is interesting to observe during the recent equity market weakness how well credit markets have resisted the stress. This is even more impressive considering the focus on difficulties experienced by several issuers and banks that were exposed to some unexpected losses. Credit default swap values for investment-grade issuers are currently resisting the spike in volatility. We have witnessed a significant increase in credit market issuance from companies seeking to fund artificial intelligence (AI) infrastructure investment. It appears doubtful however that cash-rich AI companies could be considered a source of the stress and risk aversion that has led to recent equity market weakness.

We continue to believe the combination of looser monetary policy; positive economic growth; AI infrastructure spending - and the potential productivity gains - as well as ongoing fiscal stimulus in Germany, Japan and China, and resilient corporate earnings, maintains a favourable setting for risk assets into 2026.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2025 AXA Investment Managers. All rights reserved