Why the construction of a Cashflow Driven Investment strategy is key

KEY POINTS

Within any portfolio, getting the construction right is an important element to ensuring that the objectives and aims are met. For Cashflow Driven Investment (CDI) strategies, this is particularly true given their long-term horizons and often tailored fixed income allocation.

At a high-level, CDI strategies help address a pension fund’s income requirements through regular income streams from bond coupons and maturities. While that sounds straightforward, outcome needs can vary hugely. Therefore, the structure and holdings within CDI strategies can greatly differ depending on client portfolios; there is no one-size-fits-all approach.

Nevertheless, there are a few common factors to any CDI portfolio:

- Core credit allocation - All CDI portfolios that we manage have a meaningful allocation (60-100%) to investment grade credit. Other asset classes such as high yield, ABS or sovereign could be considered to dial up or down the expected risk and return profile.

- Investment style – Most CDI portfolios are managed in a buy and maintain style, meaning that bonds are held for the long-term with the aim of keeping turnover levels to a minimum.

- Home bias – To avoid currency hedging costs, collateral calls and to help towards any liability hedging, many CDI portfolios have a home bias; in other words, they invest predominantly in the local currency of the pension fund.

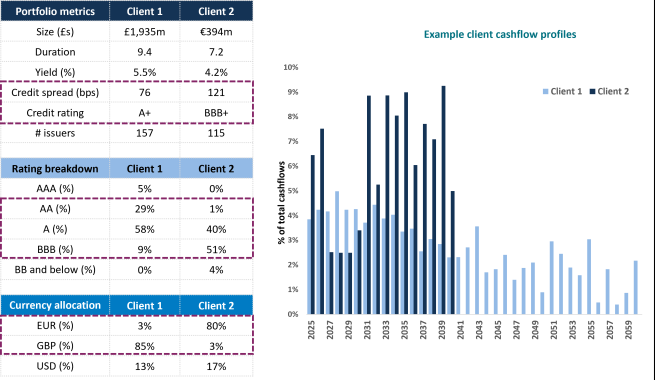

Below are examples from two live client portfolios, one GBP-denominated and one EUR-denominated. Both portfolios have a core allocation to investment grade credit, a focus on their home currency and are managed with a buy and maintain approach. The case study also shows how both have been designed to meet the individual fund requirements, as the average rating, spread, and maturity profiles of the portfolios reflect the different client requirements.

Levers to pull to create a bespoke CDI portfolio

A CDI strategy offers institutional investors five potential benefits: capital growth, liquidity, hedging, sustainability, and risk reduction. So when constructing a CDI portfolio, investors are able to apply a range of levers that can be used to reshape portfolios to give more focus on one or more of these benefits.

Most institutional clients will want to tailor their CDI portfolio to meet their specific needs. Different approaches can produce remarkably different portfolios. That is why we work closely with our clients, and any advisors they may use, to understand the primary factors which determine the shape of a CDI portfolio.

Such considerations are wide ranging but there are a few key ones to be aware of and understand the considerations behind them:

Maturity

Client cash requirements vary, and so CDI strategies should reflect those varying requirements. Shorter-maturity portfolios deliver a greater proportion of cash in the near term, appealing to mature funds with heavy upfront cashflow requirements. There is often greater clarity on the cashflows required at the short end, so the match-precision can be more exact.

Longer-maturity portfolios spread the cashflows over a greater number of years. This provides a higher degree of interest rate sensitivity, contributing to delivering and diversifying the liability-hedging portfolio.

Our experience has shown that some clients start with matching shorter cashflows, and then add more matching at the longer end when de-risking or when allocating more capital to the strategy.

Credit quality

The bedrock of a CDI portfolio will be high-quality investment grade credit, to balance the benefit of the spread over government bond yields with the additional risk taken from investing in credit. Clients can, however, seek to go up or down on the risk return spectrum, for example by limiting investments to a AAA-AA-A rated portfolio for a low risk but low spread solution, or adding more BBB or high yield bonds to deliver capital growth at the expense of a higher risk of capital loss and lower liquidity.

Asset classes

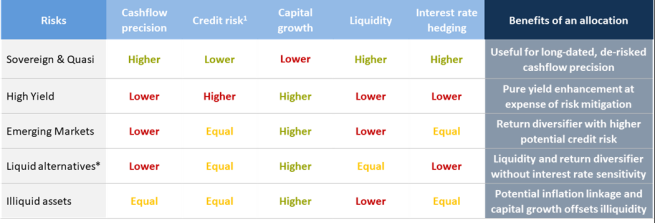

An allocation to different fixed income asset classes outside of investment grade credit can be used to tailor the CDI portfolio to different investor needs. The table below shows an overview of how a proportion, typically up to a maximum of 30% of the CDI portfolio, can be used to tilt a CDI portfolio:

Currency allocation

A local bias is preferable for most pension funds in order to match the denomination of their liabilities. But there may still be appeal for global exposure. The gains from going global are higher when:

- implementing a large portfolio,

- where local currency universe size is small

- when clients have a global liability profile.

The above factors are some of the more important aspects in construction to try to get right. In doing so, the majority of the main risk factors are accounted for.

Of course, there are other factors that can be implemented, but these tend to be smaller tweaks which can reflect specific requirements for an institutional investor such as sustainability integration1 and vehicle choice.

AXA IM’s partnership approach

Some clients will have a clear indication of what they are looking for from their allocation to CDI, however others may want to see the impact of pulling different levers to tailor the portfolio to different risk and return requirements. When working with clients, we often run several iterations based on the different levers noted above. To help with this analysis we use a proprietary optimisation tool over a range of different portfolio guidelines to work in partnership with our clients to find their desired solution.

- {https://core.axa-im.com/investment-strategies/fixed-income/insights/why-should-investors-consider-sustainability-cdi;Why should investors consider sustainability in CDI? | AXA IM Core}

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.