A motionless journey: From CFA franc to eco

Key points

- The West African Economic Monetary Union countries and France have reached a set of reforms modernising the functioning of the franc zone, an area of monetary cooperation in West Africa. The previous agreement, which came into force in 1973, was seen as out-of-date and an obstacle to freedom by the local populations

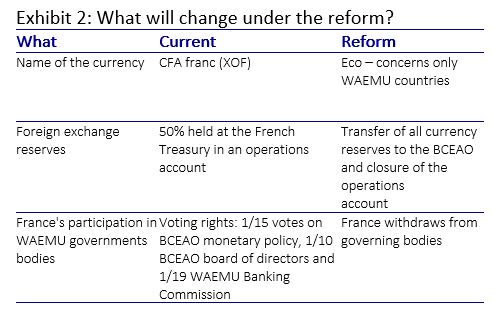

- The reform will be developed along three axes: First, changing the name of the currency from CFA franc to eco. Second, abolishing the obligation to centralise foreign exchange reserves on the French Treasury's operations account, and third, withdrawing France from the main decision-making bodies in the zone. But the same exchange rate of the eco to the euro will be maintained (ECO655.957 per euro) as the CFA franc, and convertibility to the euro guaranteed by the French Treasury

- This reform comes on top of a long-term project for a common currency extended to other West African countries - but this new agreement is not fully compatible. The transition towards an enlarged common currency will require an economic convergence of the countries towards established criteria. But currently the disparities are significant. It also needs agreement on the functioning of the enlarged monetary union. The fact that the eco remains indexed to the euro is an obstacle, particularly for Nigeria (which accounts for two-thirds of the proposed new area’s GDP) which would like to have a flexible exchange rate regime

In 2019, the West African Economic and Monetary Union (WAEMU1) initiated a shift from the CFA franc, the local currency, to a newly created currency – the eco. This marked the first changes to an agreement signed in December 1973 between the countries within the zone and France – but these changes were mostly symbolic, and the foundations of the monetary system will remain the same. The eco will still be pegged to the euro at the same rate as the CFA franc. The region must now review the benefits that monetary union has delivered in recent decades before it decides whether it should – and can – expand its membership to form an enlarged monetary union in West Africa.

The changes initiated

At the end of December 2019, French President Emmanuel Macron and Ivory Coast President, Alassane Ouattara, announced the end of the African financial community, Communauté Financière en Afrique Franc (CFA) for West African countries. A new cooperation agreement replaced the 1973 model. The franc zone includes 14 sub-Saharan African countries, divided into two groups (Exhibit 1): WAEMU and the Economic and Monetary Community of Central African States (EMCCA2). Each zone has its own currency, the CFA franc with the currency code XOF for the WAEMU countries and the CFA franc (XAF) for the EMCCA countries. For the purposes of simplicity, discussion of the currency in this paper will refer to the CFA franc (XOF).

The new deal will involve amendments to the existing agreements between the countries of the WAEMU and France, and include three major developments:

- The change of name of the WAEMU currency to the eco

- The end of centralisation of 50% of the foreign exchange reserves of the Central Bank of West African States in an operating account at the French Treasury

- The withdrawal of French government representatives from the WAEMU governance bodies (BCEAO3) – also removing voting rights in these institutions.

History and role of the CFA franc in West Africa

The franc zone system4 was created in 1945 at the dawn of African countries’ independence. It established an area of free movement of capital with a single exchange rate, regulation and free convertibility, at fixed parities with the different currencies of African countries.

The monetary union was based on three founding principles.

- Fixed parities with the anchor currency – at first the French franc (FRF) and thereafter the euro

- Guarantees of unlimited convertibility to the franc (then euro) by the French Treasury – requiring in return the centralization of member countries foreign exchange reserves in France

- Free transferability of capital between France and the zone – transfers are, in principle, free within the zone

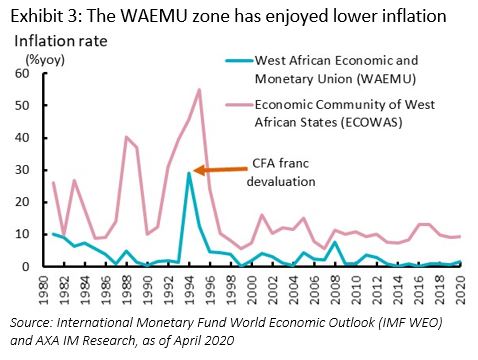

The West African countries within the franc zone have a similar economic structure, each with a high dependence on traded commodities. The trade in goods represents on average around 89% of their exports, comprising mainly coffee, cocoa, cotton, gold and oil. Therefore, these countries are very sensitive to changes in the prices of commodities. The single currency thus provided the WAEMU countries with economic stability by hedging them against local and external risks. Notably, it allowed the countries to escape the high inflation of surrounding economies. This can be seen in Exhibit 3 – the difference in inflation rates between this monetary region and the broader region has averaged 12% since 1980.

The only major exception to this was the depreciation of the CFA franc in 1994, which was a product of the US dollar’s Plaza Accord devaluation nine years before, and the French franc’s strength post-German reunification, reducing the CFA franc’s competitiveness. Commodity export revenues fell as the ECOWAS5’ terms of trade deteriorated by 36% over the following 10 years. This ended a long period of sustained growth, and the contribution of trade to GDP in these economies fell to 49.7% from a historical average of 65% of GDP.

In the absence of real economic adjustments, the Bretton Woods institutions advocated a monetary adjustment and the CFA franc devalued by 50% in 1994 to FRF0.01 from FRF0.02. Inflation spiked to near 30% in the aftermath, and governments’ social measures had to be financed through external debt. This resulted in a significant spike in foreign direct investment outflows, to 2% of GDP from an historic average of 0.4%. However, the devaluation led to a sustained return to growth and a consolidation of public finances.

Structural reforms have sustained these benefits since – notably by reducing the state's involvement in companies, developing health and education through public finances to help poverty reduction and liberalising prices to enhance the transmission of global trade prices to domestic producers. In addition, these reforms have, in the background, created a more homogeneous economic area with a high degree of convergence of economic performance.

Where is the growth dividend?

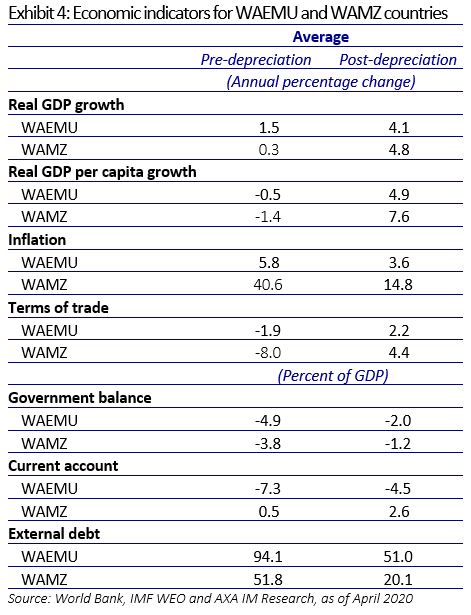

One criticism of the WAEMU monetary union is that it has not provided a significant growth advantage over other countries in the West African Monetary Zone (WAMZ). Exhibit 4 shows that the growth of the two regions has been very close - since 1994 they averaged 4.1% year-on-year (yoy) in WAEMU and 4.8%yoy in WAMZ.

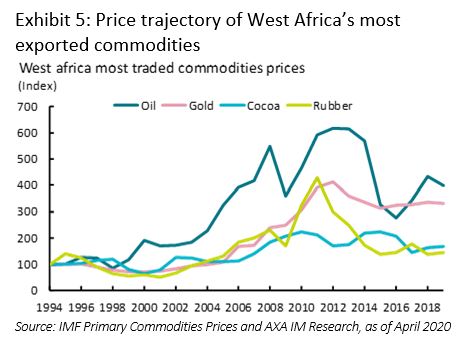

Admittedly, WAEMU countries have enjoyed better price stability compared to other West African countries, with an average inflation rate of 3.6% versus 14.8%. That said, growth in terms of trade has been much lower for the franc zone countries, at 2.2% against 4.4%. Both countries of course benefitted from the rise in commodity export prices (Exhibit 5), but the improvement of both current account balances was insufficient to lift WAEMU balances into surplus.

In terms of domestic developments, WAEMU countries have underperformed their regional peers. Before the 1994 depreciation, the WAEMU countries enjoyed an average GDP per capita of US$600 – in excess of regional peers. By 2018, the gap had reduced to a deficit of $800 per capita, lower than regional peers – significant when this constitutes around two-thirds of annual GDP per head.

This adjustment is sharp. While initially WAMZ economies may have benefitted from a convergence effect6, the ongoing improvement likely reflects a far sharper increase in international openness7 and a larger improvement in the terms of trade in WAMZ, to 4.4% from -8.0%, compared to the WAEMU, to 2.2 from -1.9%. Moreover, WAMZ economies have invested more heavily in human capital over the period. In 1994, 89% of primary school age children were enrolled in school compared to only 58% for WAEMU (with Togo an exception at 94%). Not unrelatedly they have benefited from a lower unemployment rate for a larger working-age population, with WAMZ unemployment averaging 4.8% compared to 5.5% for WAEMU, while the share of the working age population is lower in WAEMU economies at 52.2% versus 53.6% in WAMZ.

However, the underperformance of the economies in the monetary union has led to popular speculation that the currency regime itself is to blame. This has added to a long-standing resentment in some areas that the CFA franc was a remnant of colonialisation. The common currency has certainly not created a feeling of unanimous progress within the monetary union.

This rising social dissatisfaction was demonstrated by questions asked to President Macron during his visit to Ouagadougou University in Burkina Faso in 2017 and other local events8 criticising the role of France within the monetary union. The eco should help to ease the tensions within the states by breaking some of the symbols that have fueled the discontent.

The next steps to broader monetary union

In its final report of the 2019 June summit, the broader ECOWAS region reaffirmed its desire for a common currency to create a better regional dynamic with stronger integration, thanks to a gradual process built on defined convergence criteria. However, this long-term project faces several obstacles.

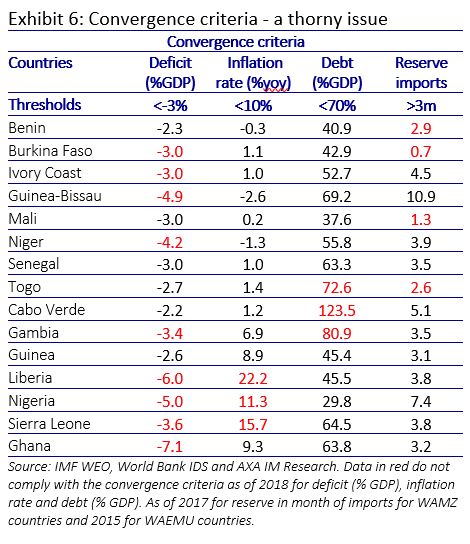

The establishment of a single currency will require the fulfilment of certain convergence criteria to eliminate macroeconomic imbalances between member states. But the convergence criteria are far from being met in most countries, presenting a material obstacle to the creation of a broader monetary area (Exhibit 6).

In 2019, only six of 15 countries met the convergence criterion for public deficits (below 3% of GDP), including only two ECOWAS countries formerly part of the CFA franc zone. Three countries deviated from the inflation criterion (equal to or below 10%), namely Liberia, Nigeria and Sierra Leone. Similarly, three – Togo, Cabo Verde and Gambia – do not meet the debt criterion of below 70% of GDP. Four countries had their reserves below three months of imports. At the time, just Senegal and Guinea, were the only countries to fulfil all the convergence criteria.

Not complying with these rules would raise concerns over the sustainability of the monetary union. The adoption of a single currency could create imbalances where weaker economies would adopt an overvalued currency, which would require painful real adjustment in economic variables.

Failure to meet these criteria has led to doubts on the capacity of some countries to meet these criteria. The report of the ECOWAS summit in Abuja, Nigeria, in June 2019 detailed the worsening macroeconomic convergence and called on member states to improve efforts to fulfil this element of building a monetary union.

Moreover, some of the key features of the new agreement further undermine progress towards an enlarged common currency. Notably, the fixed parity between the eco and the euro maintained in the new accord runs contrary to the flexible exchange rate regime adopted by ECOWAS during the June 2019 summit. This has raised objections from Nigeria, which alone constitutes two-thirds of the proposed new area’s GDP.

The modernisation of monetary management will also be a priority, particularly considering the merger of monetary mechanisms and currency reserves. A clearer timetable needs to be defined.

Expansion still a difficult and long-term project

We believe the CFA franc reform announced in December 2019 will be a transitional reform. The new currency – the eco – will initially help to break symbols that have seen growing objections in the local populations.

But many challenges remain. As stipulated in the draft law published at the end of May 2020 by the French National Assembly, the agreement ratified in December 2019 will have to be supplemented by a guarantee convention - a technical implementation text, which will be concluded with the Central Bank of West African States (BCEAO).

In the background, the implementation of the eco in 2020 could form the foundation for a common currency for the whole West African area, reviving an old aspiration.

Beyond the details of an agreement for a larger monetary union, the type of exchange rate regime – fixed or fully flexible – and the fulfilment of convergence criteria remain fundamental imperatives for a sustainable currency union. Yet both could prove economically and politically difficult to deliver. Therefore, the road towards a single currency at the ECOWAS level remains a difficult, long-term project.

- The West African Economic and Monetary Union (WAEMU) is composed of Benin, Burkina Faso, Ivory Coast, Guinea-Bissau, Mali, Niger, Senegal and Togo

- The Economic and Monetary Community of Central African States (EMCCA) is composed of Cameroon, Central African Republic, Chad, Congo, Gabon, Equatorial Guinea.

- The Central Bank of West African States (BCEAO) is composed of Benin, Burkina Faso, Ivory Coast, Guinea-Bissau, Mali, Niger, Senegal and Togo

- The franc zone is a monetary area composed of the WAEMU, EMCCA and the Union of Comoros.

- The Economic Community of West African States (ECOWAS) comprises the eight countries from the WAEMU in addition to Cabo Verde, Gambia, Ghana, Guinea, Liberia, Nigeria, Sierra Leone

- Robert J. Barro, 2003. "Determinants of Economic Growth in a Panel of Countries," CEMA Working Papers 505

- Since 1994 a measure of WAMZ international openness improved to 40 from 29, whereas WAEMU substantially decreased to 59.9 from 63.1

- Le Monde, « Manifestations d’opposants au franc CFA en Afrique et en région parisienne », September 2017

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.