Gender (in)equality in India: Women and the informal economy

Gender inequality in India appears to start at a very young age – even from before birth. Women are heavily under-represented in India’s economy and achieving gender equality needs a significant shift in attitudes towards the perception of women and work.

It is estimated that better female participation in India’s job market could add $770bn to the country’s GDP by 2025 compared to 20151. But this will not be easy.

We are looking at the gender equality picture in India as the final part of our series where we have already examined the situation for women in Germany, Japan and China. These four markets have been used to illustrate what we have identified as the key drivers of gender inequality, through the different stages of a woman’s life.

Like China, prejudices against girls appears to start from birth. Gender-based selective abortions have led to a skew in the number of baby girls born compared to boys. For every girl born, 1.11 boys are.2

Girls are faced with persistent inequality during childhood which affects access to nutrition, health and safety. The Lancet medical journal says that over 2.4 million girls under the age of five died every decade because of gender bias3.

India is ranked the world’s most dangerous country for women due to factors which include sexual violence and human trafficking.4Statistics show than more than 63 million women are “missing” in India.5

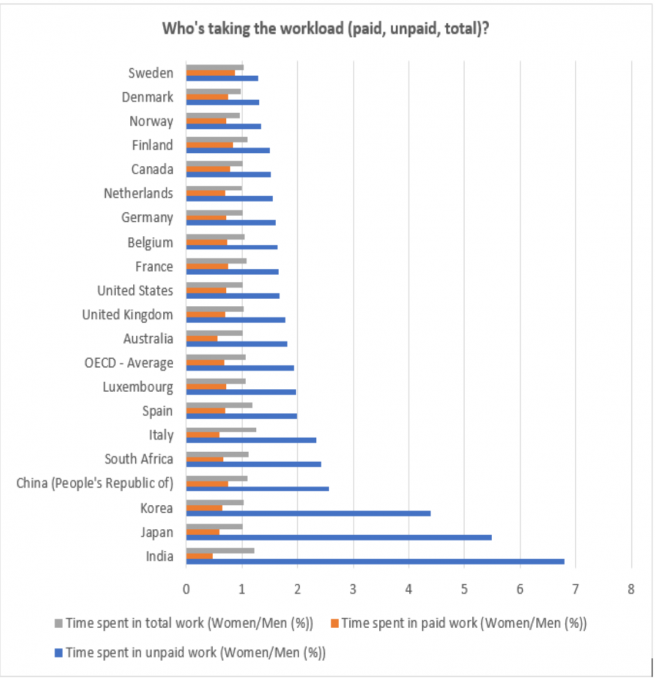

One aspect where the sexes are more equal is education – there is relatively little difference through participation in various stages of school. The gap, however, becomes evident the moment women start to work – and the rate of female participation rate in the labour market is just 28.4%.6

One of the main reasons for this lies in time spent in unpaid work. Women spend seven to 10 times more on domestic tasks than men7, compared to an average of two to three times worldwide. Yet women do want to work – a third of those who are primarily in housework say they would like a job.8

- International Labour Organization (ILO), Women and men in the informal economy: A statistical picture, Third edition, 2018

- ILO Global Wage Report 2018-2019

- World Bank, Women in India’s Economic Growth, 16 March 2018

- TeamLease Maternity Report 2017

- The Washington Post, 29 January 2018

- World Bank database, 2018

- OECD and McKinsey May 2018

- Harvard Kennedy School, 10 March 2018

Segregation in the workplace

The huge majority, at 88%, of India’s employment is informal1. This has an impact on both sexes, and it is even more difficult to fight against inequalities as there is no workers’ protection. The challenge of creating jobs of quality in India is closely related to first creating more jobs in the formal economy.

For women who do work there is a 34% gender pay gap in hourly wages2, although this is narrowing over time. The gap can be attributed to various forces of discrimination, including segregation at work. Women are restricted in their physical movements by the male members of the family and are told what type of work would be appropriate for them. Beyond that, there are traditional factors such as age, education and experience and others which are less visible and subtle.

Indian working women are discriminated both at the top (the “glass ceiling”) and at the low end of the wage distribution (a “sticky floor”), where the pay difference is higher. In conservative India, women are often discouraged from working and men are still the bread-winners.

Women often quit their jobs to take care of families, explaining why it is challenging to climb up the corporate ladder and make it through managerial positions. The World Bank estimates that 20m women dropped out the workforce between 2004 and 20123– and the situation is deteriorating.

To decrease gender disparity in the labour market and encourage the return of mothers after childbirth, the Indian government – through the Maternity Benefit (Amendment) Act – increased the amount of paid maternity leave from 12 to 26 weeks in 2017. Yet, as costs for maternity benefits are passed on to employers, an unintended consequence is that there are bigger hurdles for companies to hire women and to keep their pay levels lower.

We expect this to be most pronounced in small and medium-sized companies where the presence and productivity of staff is a key driver of performance. This assumption was echoed by several recent surveys, which showed that a potential one to two million women could lose their jobs across 10 sectors within the first year of implementation of the extended maternity leave.4

At higher levels in an organisation, the quota on boardroom diversity mandating at least one woman on the boards of listed companies has resulted in a more gender-diverse picture of directors. While this is a good start, we believe that more needs to be done before reaching a critical mass that will allow women directors to have a voice that truly counts.

The investor engagement playbook in India

There are numerous levers that we think can be activated to advance gender equality in India. The main priorities of improving women empowerment at a corporate level and convincing companies to embark on a more diverse and inclusive journey revolve around shifting societal attitudes in the workplace and creating a safe workplace environment.

Our engagement recommendations with Indian companies include:

- A clear tone from the top from senior management and the board of directors calling for equal opportunities and zero-tolerance of gender inequality and sexual harassment. Without accountability and engagement from the top, changes in a company’s values and climate are unlikely to happen. We would require the senior management and the board to make a public statement around gender equality.

- Establishing equal opportunities policies and programmes to ensure gender equality. In a country where few women access the job market, making sure companies have set policies in terms of gender recruitment is a first step before expecting better gender balance representations at managerial levels.

- Flexible working to allow men and women to reconcile their private and personal life. It is particularly important in a country like India where women still spend much of their time in taking care of children, elderly family members and household tasks.

- Clear reporting of gender data which provides a granular breakdown of the proportion of women in positions across different seniorities and by different business units. We want to understand the gender balance within the company and see specific data (and possibly guidelines/targets) around the gender breakdown of entry-level workers and turnover. Some other metrics could include percentage of women on boards and anonymous gender-based reporting on whistleblowing systems.

Gender inequality remains a challenge that virtually all countries – regardless of the stage of their economic development – must overcome. This is not an industry, nor a market issue. It is a global one.

Ultimately, we believe that the persistence of the gender gap threatens the success of companies and economies as it leaves on the table $160 trillion of unrealised wealth, according to a World Bank estimation – and if not addressed puts at risk Goal 5 of the UN Sustainable Development Goals. Achieve gender equality and empower all women and girls. For investors, it risks dampening long-term returns.

The recommendations from this research form the basis of a multi-year engagement initiative which we started conducting with companies in 2019.

Having looked at the situation in Germany, China, Japan and now India, we have found similarities but also many differences in the way women and women workers are perceived and the opportunities and barriers they face. Resolving the issues that we have identified in each country, and others which no doubt exist elsewhere, require differentiated and targeted approaches. We hope that the frameworks suggested in this research will be adopted by the investor community to engage with companies based in many other countries which share similar gender inequality trajectories and economic development and that together we might be able to help improve the situation for women around the world.

- McKinsey, The Power of Parity: Advancing Women’s Equality in India (2015)

- The Economic Times, July 2019

- The Lancet, 21 August 2019

- Thomson Reuters Foundation experts’ survey, 2018

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

This document has been edited by AXA INVESTMENT MANAGERS SA, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 393 051 826. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

In the UK, this document is intended exclusively for professional investors, as defined in Annex II to the Markets in Financial Instruments Directive 2014/65/EU (“MiFID”). Circulation must be restricted accordingly.