Gender equality in Japan: Can ‘Womenomics’ deliver?

The gender pay gap in Japan is the third highest amongst the world’s major developed economies1. Traditionally, women gave up their careers at marriage or at the birth of their first child. This is partly due to culture but also due to relatively poor childcare provision and the typical environment of long working hours.

But things are changing, particularly as the Japanese government itself is pushing for reform. Prime Minister Shinzo Abe has been an advocate of equality with his so-called “Womenomics” plan. The need to have more women participate in the work force is a key solution to the falling numbers of male workers in Japan’s rapidly aging population.

Despite these reforms, job quality is still a concern. Casual and part-time employment continue to dominate job opportunities for many women.

In a series of articles, we look at the dynamics of gender inequality throughout a woman’s entire working life, taking four key capital markets as examples.

Beginning with Germany, and now looking at Japan, then later China and India, we identify the drivers of inequality, assess local company practices and highlight recommendations for investor engagement.

Macro snapshot: The motherhood penalty

Employees have become a scarce resource in Japan. Since 2000, there has been a 13% fall in the number of working-age people2. Japan is already the oldest country in the world in terms of population age and the birth rate is one of the lowest3.

By 2040, more than a third of people in Japan will be over 65 years of age. The International Monetary Fund (IMF) assessed that this backdrop could potentially lead to GDP falling by a quarter over the next 40 years.4

Prime Minister Abe launched a series of goals in 2013 to encourage higher female participation in the workforce. The government has put in place clear targets to attract and retain women workers. These include policies to increase the number of childcare facilities and to provide a year’s paid parental leave for both parents after the birth of an infant. There is also a bonus entitlement if both parents take the leave.

As a result, the participation rate of working-age women has topped 69% – versus 65% in 2013.5 But the effectiveness of these policy moves has been watered down by other existing regulations, such as the strong financial disincentives in terms of tax, pension and insurance coverage.

We believe these are structured so that the unintended consequence has been to discourage one half of a couple – typically the woman – from seeking full-time work. The lack of enforcement and legal penalties for corporate inaction is also to blame for the slow progress of gender equality.

There is a huge incentive for Japan to rectify this. If the same proportion of working-age men and women were in jobs by 2025, the labour force would grow by 1.5 million, according to the OECD. This would add 0.8 percentage points to GDP per capita per year. A positive side-effect would be to widen the tax base and ease the dependency ratio.

In the workplace: Leave with no return

Women are highly educated in Japan. At the point of graduation when most companies hire new employees, the gender ratio of the pipeline is basically equal6. The real impact of gender discrimination is felt once they get married or have their first child as females are still traditionally seen as the main caregiver and household manager. As a matter of fact, Japanese women spend five to six times more in unpaid domestic work than men – the highest rate among OECD countries7.

Corporate culture is also in dire need of reform – especially the image of the ideal Japanese salaryman. They are expected to put work ahead of family, accept grueling hours, and take little holiday as a demonstration of strong loyalty and commitment to their company. In return for this, the post-war model was that companies provided life-time employment.

Going on maternity leave and taking time to raise a child is counter to this. As such, women returning from leave often face a break in their career path and/or are downgraded to lower positions. This explains why almost one out of two women don’t return to work after giving birth to their first child.8 And for the one who go back to work – 77% do so as non-regular workers, e.g. part time, temporary or contractor.

Social norms and peer pressure dissuade fathers from taking paternity leave. Despite the very generous paternity leave policy of 52 weeks, the uptake is very low. In 2016, out of the 3% of fathers who took the leave, more than 80% took less than a month and 57% took less than five days9.

Companies continue to offer employees allowances and benefits covering household costs – but this is often subject to wives not earning more than a certain wage threshold. This is another reason why most women, at 56%, are dissuaded from accepting regular jobs.10

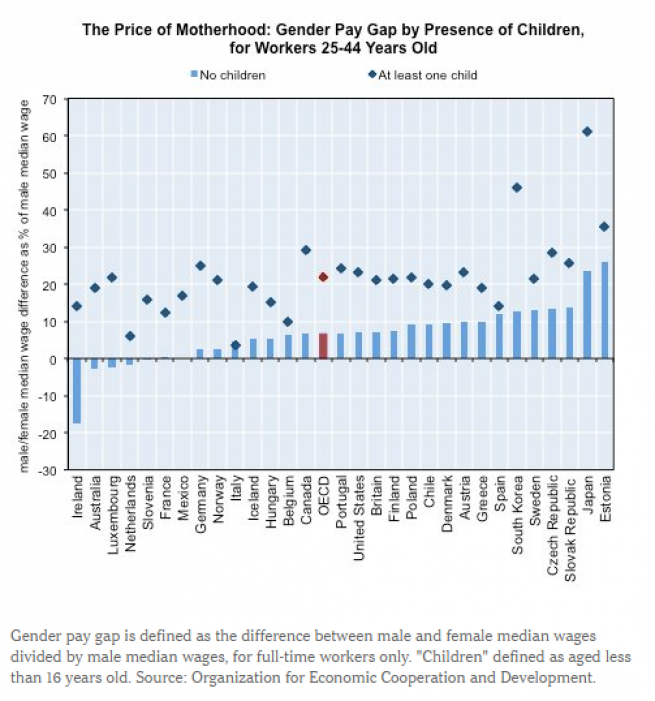

Now, out of the 71% of working mothers in 2017, only a quarter was employed on a full-time basis. Only 13% make it to managerial positions11. Differences in job status and career progression results in a gender pay gap of 24.5% – the third highest among OECD countries.12

- OECD

- World Bank database 2018

- World Population Review, 2019

- IMF Staff Country Reports- Japan, November 2018

- World Bank database

- World Bank database

- OECD employment database

- PRI, 24 August 2018

- Source: Japan’s Ministry of Health, Labour and Welfare

- OECD Economic Surveys: Japan 2017

- World Bank

- OECD, 2017

How investors can start to make a difference

Despite the government’s call for action and policy initiatives that have been running for several years, Japanese companies appear to be generally responding slowly in terms of changing their approach and making the workplace meaningfully supportive of working mothers.

We believe that investors can start to make a difference by engaging with Japanese companies around the following issues:

- Making diversity an explicit business objective. A clear tone from senior management is needed to permeate the company and to encourage employees to rethink traditional norms. Leadership commitment around gender equality would strongly encourage companies to link diversity objectives to broader business targets. It is particularly important in Japan where progress has been slow within companies.

- Pipeline of women in leadership positions. We believe companies need to articulate and explain how they are moving women into senior management positions. Engagement around diversity at top management position and at board levels are important. Performance indicators will include the percentage of women on boards and female executives, and targets for both. But just as important is the pipeline of women who will be future leaders – companies need to report on the number of women in middle management roles.Family-friendly policies, programmes and provisions to help people keep their job while dealing potentially with young children and aged relatives is a priority. In many instances, women’s plates are overloaded with personal and professional responsibilities – often forcing them to choose between family and career. We have spoken with Japanese companies who have introduced specific support systems when they are posted on multi-year foreign assignments such as paying for childcare and education.

- Promote a cultural change in the workplace. As we see it, the division in gender roles is still the main reason holding back women empowerment, so companies need to roll out policies to erase those stereotypes. These should, in our view, include encouraging the take-up of leave – both holidays and parental leave – by both men and women and developing mentoring programmes. It should also include setting clear working hours and making flexibility such as working from home more acceptable. Providing IT infrastructure to enable this as well as management commitment is vital.

- Incorporating women back into the regular workforce. People in non-regular employment usually don’t have access to the same training and benefits. Companies should disclose the proportion and number of women in the workforce by types of contract and employment status – and any gender targets for new regular employment contract.

At AXA IM we intend to engage with companies in Japan using this research as a basis, assessing local company practices and highlight recommendations for investor engagement. Gender inequality remains a challenge that virtually all countries – regardless of the stage of their economic development – must overcome. This is not an industry, nor a market issue. It is a global one.

What is clear is that no governments nor corporations can afford to be passive or reactive when it comes to effectively leveraging female human capital. They need to be pro-active. We believe that investors can play an important role in promoting the women empowerment agenda with policymakers and company boards and management through engagement.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

This document has been edited by AXA INVESTMENT MANAGERS SA, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 393 051 826. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

In the UK, this document is intended exclusively for professional investors, as defined in Annex II to the Markets in Financial Instruments Directive 2014/65/EU (“MiFID”). Circulation must be restricted accordingly.