Gender diversity in Earnings Calls: Why do men talk so much?

The myth that women talk more than men is just that – a myth – at least when it comes to corporate earnings calls.

And if you are a senior executive called Jennifer or Laura, you are likely to have contributed to the increase in US female boardroom representation in the past 10 years.

These are just two of the insights we have gained from developing natural language processing (NLP) language models for use in our stock selection process. Companies’ quarterly earning calls transcripts are among our key data sources, and we looked at these transcripts from a diversity point of view – the results were surprising.

Gender balance starting to improve

Usually it is the company chief executive (CEO) and chief financial officer (CFO) who speak to investors on earnings calls. Our NLP model allows us to assess gender balance at these companies – and we found that businesses are making progress, but it is slow.

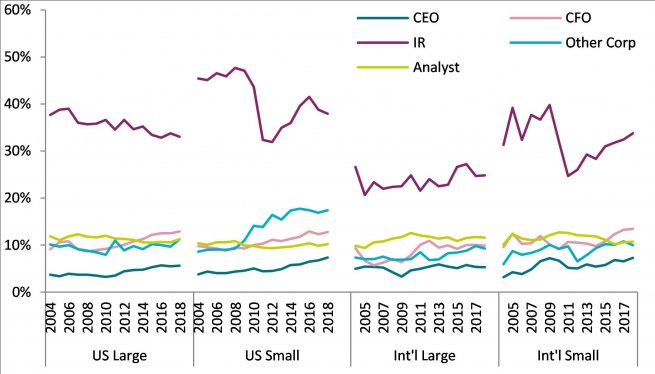

Among US companies, the proportion of comments from female CEOs (or equivalent) rose from around 3.5% of the total participants on earnings calls in 2004 to 5.5% in 2018. In fact the increase has only taken place since 2010 (Chart 1). For female CFOs, participation rose from around 10% to 13%, albeit with a fall during the Great Recession. Among Investor Relations officers, female participation is much higher, but fell from around 38% to below 34%.

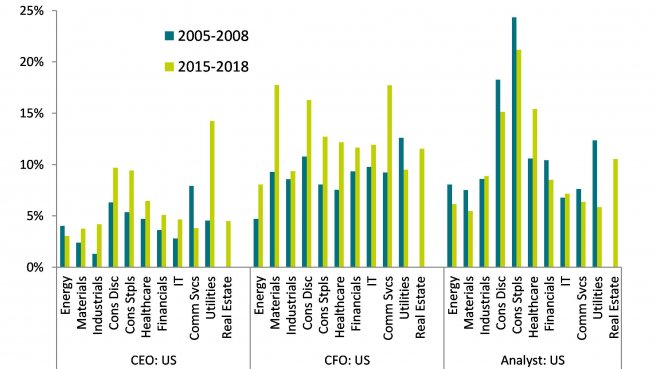

These biases and trends are almost identical for large-cap and small-cap companies, and for non-US companies (see ‘International’ on Chart 1). Furthermore, progress towards gender balance in earnings call participation at CEO and CFO level was made in almost all US industries (Chart 2). This gives us confidence that listed companies have successfully increased female participation in senior management. Incidentally, the widely reported pattern of relatively low female representation in Information Technology workforces compared to other industries is not seen in this analysis of senior roles.

Meanwhile, a quite different pattern emerges when looking at investment analysts asking questions during earnings calls. The number of female investment analysts’ comments fell from 12% to 11% in US large cap (Chart 1), with significant falls in several industries being offset by increases elsewhere, notably healthcare (Chart 2).

Why do men talk so much?

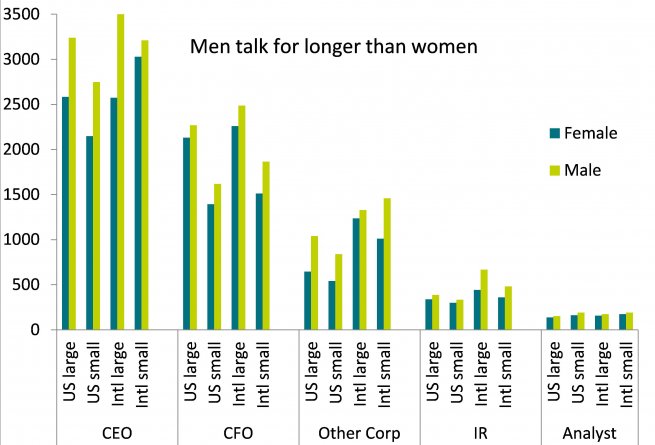

Looking at the length of contributions made by earnings calls participants, we see a consistent pattern that men speak for longer than women in similar roles (2018 data, Chart 3). Remarkably, this pattern holds among CEOs, CFOs and investment analysts in their questions to company management, and across US, international, large-cap and small-cap companies.

It could be the case that female participants are more guarded in their comments, or more economical in their speech – any number of factors could account for this difference between male and female presenters, and warrants further research.

What’s in a name?

There are many dimensions to diversity, not just gender. There are some interesting points about social diversity that can be inferred by the given names in US conference call participation.

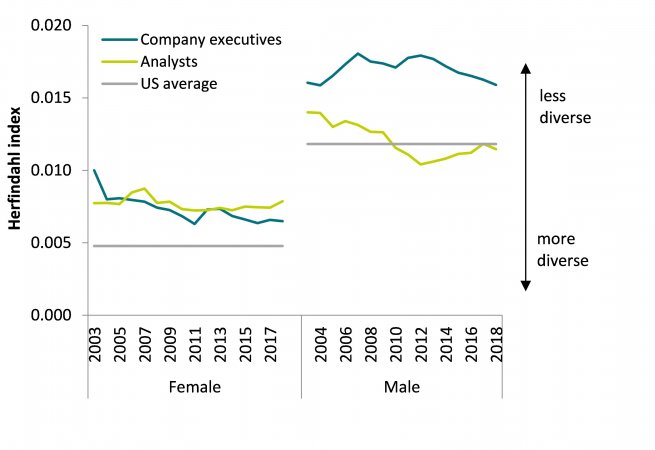

We found that participants on US corporate conference calls are more likely to have the same first name than the typical occurrence of that name in the country’s population as a whole. For example, looking at female participants on earnings calls, we found an increasing number of women called Jennifer, Laura, Lynn, Kimberly, Deborah and Kelly.

The fact that they share relatively fewer names suggests that company officers and analysts (both male and female) have not been drawn from a broad cross-section of the population. In other words, there is a lack of diversity, perhaps – but not necessarily – related to social class, religion, age, or ethnicity bias. We found just one exception: among male analysts, the mix has become more diverse over the past 15 years, to the point where now it is quite similar to the overall US population.

We used a Herfindahl index for comparison (a standard measure of concentration, see Chart 4). The analysis is split between male and female names. Because female names are simply more diverse across the population than male names we account for that in our analysis.

Companies don’t talk about diversity

Finally, we analysed how often diversity and related topics are mentioned in company financial reports and in results meetings. We find no evidence of any trend – for example the word ‘diversity’ was mentioned in various contexts in 5% of meetings in 2018, a rate unchanged since the mid-2000s. We were only a little surprised by this: it’s not unreasonable as company reports and meetings are intentionally focused on financial results.

What does this mean for investors?

For some years now companies have expressed their ambition to increase diversity in their workforce and management. We believe that this goal can have benefits for shareholder returns.

We have previously found evidence that diversity is associated with positive economic outcomes for companies, and a profitability ‘moat’ among companies that are the most threatened by competitive forces. Diversity isn’t just a ‘nice to have’; it is an economic advantage. We are therefore encouraged at the progress our analysis shows in gender balance at US corporates, but in terms of social diversity, there is still some way to go.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

This document has been edited by AXA INVESTMENT MANAGERS SA, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 393 051 826. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

In the UK, this document is intended exclusively for professional investors, as defined in Annex II to the Markets in Financial Instruments Directive 2014/65/EU (“MiFID”). Circulation must be restricted accordingly.