COVID-19: Greening the recovery

Executive summary

- The economic shutdown due to the coronavirus pandemic has led to a steep fall in greenhouse gas emissions around the world. Estimates suggest it has fallen by a quarter.

- This means that global carbon emissions may end up having reached a peak in 2019 and could be down by more than 5% in 2020.

- Despite such historic falls, we would need to replicate – and more – the effects of the last few months if we are to achieve climate change goals to keep global warming to within 1.5 degrees Centigrade.

- Policymakers, industry and financial institutions must use this crisis as an opportunity to construct a recovery that ensures a sustainable economic recovery while minimizing carbon emissions.

- AXA IM has recently supported the European Alliance for a Green Recovery. AXA IM is also proposing concrete solutions like the “European Climate Emergency Fund”, modelled on the European Stability Mechanism to finance green projects.

- AXA IM believes investors have a key role to play here through their stewardship efforts. They must scale up their engagement agenda. They should use a 360° view engaging with energy and power producers but also end-use demand side sectors promoting both the shift of energy supply mix and efficiency gains

- from consuming sectors.

The coronavirus outbreak has been a tragedy for many, a shock for us all and a crisis for economies around the globe. We have essentially embarked on a massive experiment – slashing economic activity to limit the pandemic, sharply reducing carbon emissions and preparing for only a slow resumption of growth. The question now is whether the world can use this moment to build a less carbon-intensive economic model as we return to something like normal – a model that could put the temperature goals of the Paris Agreement tantalisingly within reach.

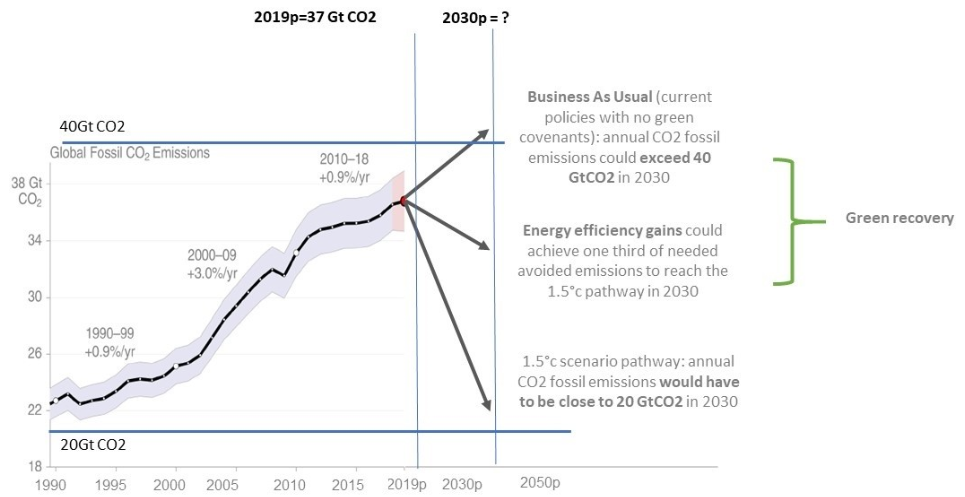

It won’t be simple. It now seems likely that COVID-19 will leave 2019 as the first peak in carbon emissions since the financial crisis of 2008-2009 but it remains difficult to estimate the extent of any drop. The analysis released so far implies it would be more than we have seen in any other recessionary environment, but it may still fall short of the annual decrease in emissions needed to fulfil the Paris Agreement goals – to keep global warming to within 1.5 degrees Centigrade of pre-industrial times.

Chart: Evolution of CO2 emissions from 1990

We believe that the decisions taken by society next will be crucial. This is a chance for government, industry and financial institutions to give thoughtful consideration to every unit of carbon allowed back into the system as economies reignite. The goal must be to preserve a sustainable economic growth while minimising emissions, and here lies a role for responsible investors.

Detailing the impact

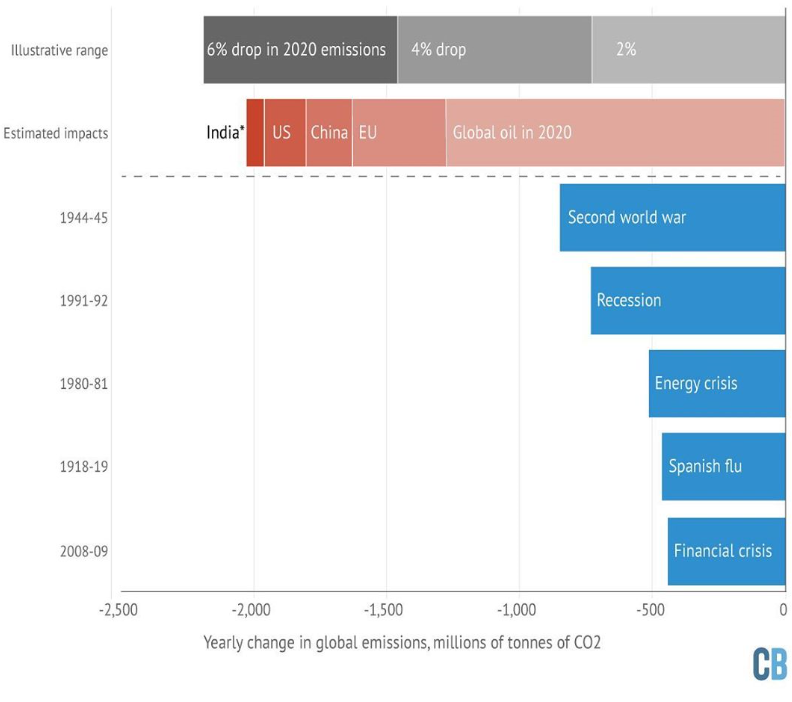

What has been the effect of coronavirus on greenhouse gas (GhG) emissions? In Asia, particle & CO2 output has fallen thanks to lockdowns, factory closures, bans on large gatherings and transport curtailment. In fact, analysis by specialist publisher Carbon Brief has estimated that carbon emissions in China fell by 25% in February 2020, equivalent to 200Mt of CO2 avoided1 .

In Europe, where emissions had likely already fallen in 2019, emissions measured through the EU emissions trading scheme (EU ETS) could face a significant drop of 25% from 20192 . European power sector emissions are expected to decrease by 12.7%. In the US, the impact of COVID-19 on carbon emissions is harder to estimate, given the lag time in the virus spread, but the Energy Information Administration (EIA) has already forecast that total oil consumption would decline 6.5% in 2020 to average 19.1 million barrels per day. This would be the largest percentage decline in 40 years.

That estimate may prove too modest. Oil markets have been stunned in recent weeks by massive price drops as global storage reached capacity and the sudden shock of the temporary collapse in demand became clear.

Carbon Brief has already gone back to update its forecasts based on this slump in demand. In mid-April it increased its estimate of the emissions impact of coronavirus to -5.5% from -4%3 . That new number equates to 2,000Mt of CO2 this year alone. Before now, the largest annual reduction to date was the 845MtCO2 fall in 1944-45, at the tail-end of the second world war. The decline after the financial crisis of 2008-09 ranks only fifth, at 440MtCO2.

Table: Coronavirus expected impacts on Carbon emissions

Living within our means

Where does that leave us on the path to achieve the Paris Agreement commitments? It’s tempting to think that the world in which we now live– with airlines grounded, meetings moved online, business and economic activity shackled – has put us in the place we need to be. Not quite.

To put the potential 2020 coronavirus effect in a broader climate context, global GhG emissions would need to fall by more than 6% every year this decade4 – more than 2,200MtCO2 – in order to limit warming to a maximum of 1.5C above pre-industrial temperatures. If negative emissions technologies are excluded or fail to become available at scale, then the required emissions reductions for 1.5C would be even higher, at 15% every year until 2040. Starting next year, yearly emissions cuts should be more than 7% and emissions need to peak as soon as a possible.

Our Chief Economist Gilles Moec said recently that the ongoing recession is having only a very marginal impact on how we are consuming our “carbon envelope” and is not giving us more time to deal with global warming5. From a macro level viewpoint, we should not rely on the Covid crisis to secure decarbonization of our economy.

It is indeed a sobering thought that over the next couple of decades we would need to replicate – and more – the effects of the last few months. But this crisis has still offered us an opportunity to construct a recovery that builds on the progress we have already made.

Making an impact

One clear point about the hit to global GDP – forecast to contract by minus 3% this year6 – is that it is hoped to be temporary, and that means the drop in global carbon dioxide emissions will likely be temporary too. For all our progress over the years, we have not yet successfully decoupled economic growth from carbon emissions.

The expected recovery, however, will give us a chance to embed industrial and societal shifts that support the energy transition. We believe that the coronavirus outbreak should harden policy thinking around climate change, and the need for decisive and collaborative action to tackle global, existential threats. It should help encourage public stimulus for green initiatives and should strengthen key themes for investor engagement.

And so, while there will remain a direct relationship7 between carbon intensity and economic growth, GhG emissions are also a function of the energy mix and its carbon content, and of the energy efficiency of final consumption/demand. These are the crucial drivers for policy makers and investors who want to green the recovery.

An obvious step is to redouble efforts to shift the energy mix. Renewable energy is growing exponentially (+13.8% per year between 2013 and 20188), but growth has still been too low to offset the growth in fossil energy consumption (+1.5% of oil and +2.6% for gas over the same period) which still dominates. Growth in renewables has outpaced growth in all other forms of energy since 2010, but the share of fossil fuels in global primary energy demand remains above 80%.

Now, with populations locked down to slow the global coronavirus pandemic, the double whammy of oversupply and demand shock is severely limiting the financial resources of oil majors. That has prompted many to announce deep cost-cutting measures that will likely limit large-scale industry investments in the energy transition. This should be avoided, through policy intervention and shareholder pressure where possible. Volatility in fossil fuel revenues means investments in renewables may constitute a way to stabilize the bottom line of majors – it remains important to continue incentivizing oil & gas companies to decarbonize as marginal cost decisions could temporarily postpone some green projects. The same goes for utility companies whose transition projects away from coal or into renewables risk being delayed for similar reasons.

Airlines have been among the most dramatically affected businesses as the outbreak took hold. Planes have been grounded, staff furloughed, and the skies are strangely quiet. We may well find that the road back from the virus softens demand over the longer term, but the risk in racing to recover from a crisis such as this, is that climate commitments fall short.

While it is not covered by the Paris Agreement, the aviation industry has committed to sustainability targets, including carbon neutral growth after 2020 and a 50% reduction in emissions in 2050 vs 2005. Much of this was to be achieved through carbon offsetting but the coronavirus shock is likely to skew how that system works, risking a new rise in net carbon emissions once normal traffic resumes. At the same time, other measures such as sustainable fuels and new technologies or the realisation of efficiency improvements may be deprioritised unless investors keep a careful watch. Airlines are also asking governments to postpone climate-related policy decisions such as green taxes.

Delivering change

This is an important point. Many companies, and even industries, will only survive this crisis with the support of the state. Policy makers are organising bail outs and stimulus in order to support economic activity in the post-crisis environment. This is a clear opportunity to deploy green stimulus by conditioning support on decarbonization criteria.

AXA IM has recently supported the European Alliance for a Green Recovery launched by Pascal Canfin, the Chair of the European Parliament Environment Committee. This initiative brings together a coalition of policy makers, companies, trade unions and financial institutions to develop a recovery package that accelerates the transition towards climate neutrality and healthy eco-system.

AXA IM has also proposed concrete solutions, and an engagement approach, which can contribute to a greener recovery.

In November 2019, AXA IM proposed a “European Climate Emergency Fund”, modelled on the European Stability Mechanism, which would issue debt instruments whose proceeds would be used to fund green transition projects undertaken by governments or corporations9.

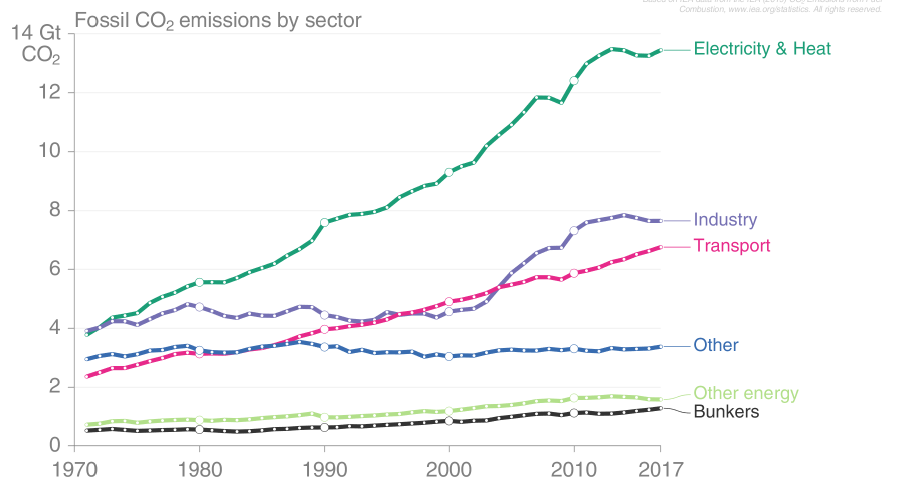

Investors also have a key role to play here and can scale up their engagement agenda, not only towards energy producers, but also with end-use demand side sectors. According to the World Resource Institute, since 1990 three sectors stand out as the fastest-growing sources of greenhouse gas emissions: energy use in industrial processes, transportation and manufacturing/construction grew by 174%, 71% and 55% respectively.

In comparison, emissions from electricity and heat generation started to decrease from 2013 thanks to various factors, including a shift to natural gas from coal and increased use of renewables.

Chart: CO2 emissions by end-use demand sectors since 1970

As a global investor, we adopt a climate-focused engagement and voting strategy across all sectors of the economy which have a role to play in limiting global warming10.

The Climate Action 100+ initiative is one of the best-known investor coalitions and engages with the most carbon intensive companies in the world on climate related issues. It has been mostly focused on energy supply sectors so far. But engagement opportunities still exist in the end-use consumption sectors. As an example, the Transition Pathway Initiative (TPI) group of Grantham Institute researchers at the London School of Economics is used as an academic advisor by Climate Action 100+ investors. It has developed a framework covering more than 230 companies to evaluate the alignment of their carbon pledges to Paris Agreement scenarios. TPI analysis says that only 13% of that sample is currently in line with a below 2° scenario. This poor performance is spread quite homogeneously between energy supply sectors and demand-side industries.

Responsible investors must be vocal in using these tools and developing others. The message should be powerful and clear. We have been given a glimpse of the kind of adjustments our world needs to make if we are to definitively tackle the looming threat of the climate crisis. Far from distracting us from this, COVID-19 should harden our resolve while teaching us valuable lessons.

- Carbon Brief, April 2020.

- Estimate from the Independent Commodity Intelligence Services company (ICIS)

- “Analysis: Coronavirus set to cause largest ever annual fall in CO2 emissions”, April 2020

- UNEP Gap report 2019

- See Gilles Moec MacroCast #42, 20th April 2020

- IMF World Economic Outlook, April 2020

- This relation is also known as the Kaya equation relating GhG emissions to GDP per capita, Demography, Energy intensity of GDP and Energy efficiency

- Bioenergy, Wind, Solar, Other Renewables (does not include Hydro) - Global Carbon Project 2019

- See « A European Climate Emergency Fund », Gilles Moec AXA Chief economist. 19th November 2019.

- For more details on our engagement and voting, please refer to our 2019 Active Ownership report

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.