Can electric vehicles help drive a green recovery?

The Impact of Covid-19 on Air Pollution

Our world is increasingly urban. The U.N. calculates that more than one-quarter of the world’s population live in cities with more than 1 million inhabitants. But while city populations are growing quickly, their transport systems can’t keep up. According to McKinsey 1, vehicle traffic speeds in many of these city centers average as little as nine miles per hour.

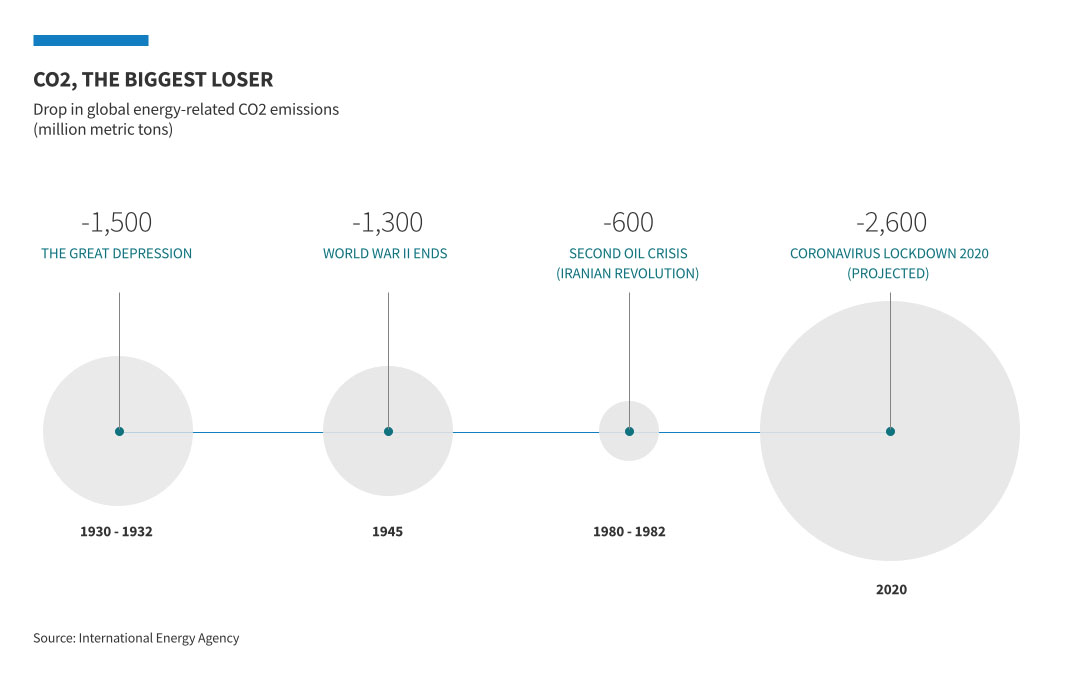

Increasing population density and slow-moving traffic mean unhealthy environments for citizens. The dramatic drop in air pollution during the coronavirus lockdown offered the world a stark reminder of the damage regular traffic volumes have on air quality. As an estimated one-third of the world’s population 2 went into lockdown, air pollution levels plummeted, and CO2 emissions dropped by the highest amount ever recorded.

"Coronavirus looks set to cause the largest-ever annual fall in CO2 emissions." Dr. Simon Evans, Deputy Editor and Policy Editor, Carbon Brief

Transport is the second-largest contributor to air pollution, after industrial processes; BloombergNEF (BNEF) calculates that it accounts for one-quarter of the world’s total CO2 emissions. When that figure is broken down, road vehicles—cars, trucks, buses, two- and three-wheelers—account for nearly three-quarters 3 of it.

With an estimated 64 million passenger cars 4 expected to be sold this year, in a global automotive industry projected to be worth $8.9 trillion by 2030 5, there is a growing opportunity for investment in not only clean vehicles—which make a real difference to air quality—but also the sector’s surrounding infrastructure and supply chains.

Cities Changing Their Travel Plans

As cities begin to emerge from their respective lockdowns, people are on the move once again, and traffic figures are rising once more 6. Many cities, however, are keen to ensure the path out of lockdown is a green one. Mayors from 40 major cities 7 around the world have warned that the recovery from Covid-19 “should not be a return to ‘business as usual’ because that is a world on track for 3C or more of overheating.”

Many commuters have sought their own solutions to socially distanced, less-polluting methods of personal transport, notably in Europe 8 and the U.S. 9, putting the onus on policy makers and city governments to catch up.

In London, the need to help commuters get back to work in one of Europe’s most congested cities has seen the ban on rented electric scooters on public roads lifted 10. The move is part of a $2.5 billion investment 11 the U.K. government is making in building a green transport network, as it believes that “transport is instrumental to our recovery.”12

Paris Mayor Anne Hidalgo has proposed dedicating a lane of the inner city’s highway road—the Boulevard Périphérique—to public transit, zero-emission vehicles and carpoolers. Diesel vehicles will be banned from the highway by 2024, and only low-emission vehicles will be granted access by 2030.

"Globally, there’s a huge regulatory push to deliver on the Paris Agreement. Ultimately, the long-term goal is to tackle climate change and achieve greater levels of responsible investing." Yo Takatsuki, Head of ESG Research and Active Ownership, AXA Investment Managers (AXA IM)

"Covid-19 is a terrible health crisis, but the lockdown and the recovery should not be achieved at the expense of the fight against climate change and pollution in our cities." Anne Hidalgo, Paris Mayor

"Air pollution is the fourth-largest risk factor to human health on the planet." World Health Organization

The Outlook for EVs: EVs Driving Change

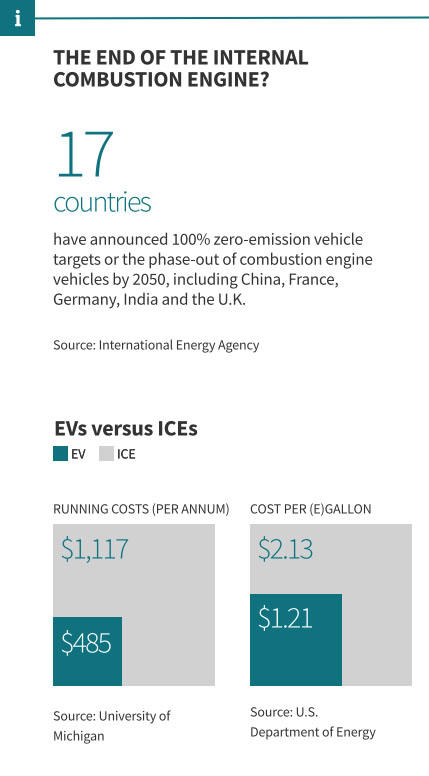

The U.N. has designated 2020 as the start of the Decade of Action 13, in which it wants nations to achieve its 17 Sustainable Development Goals to create a cleaner, more equitable world. The decarbonization of the transport sector seems like a good place to start.

In recent years, the EV industry has worked hard at overcoming the challenges of cost competitiveness, achievable mileage and an adequate charging network to make EVs a viable alternative to combustion engine-powered vehicles.

However, there is still some ways to go. The average retail price of the gasoline and diesel cars sold through September 2019 was $35,970, while the electric counterpart cost $51,691, according to JATO Dynamics, a supplier of automotive business intelligence.

"Automakers are increasingly recognizing that they need to start to invest in products that are viable going forward. Clearly, that means electric." Amanda O’Toole, Portfolio Manager, Clean Economy strategy, AXA IM

The current unique selling point for EVs is their overall lowering running costs, but a number of automakers appear to be addressing the gap by lowering prices 14 and introducing more compact, affordable models 15. According to BNEF, by 2024 some EVs will cost the same at combustion engine models, before becoming cheaper the following year.

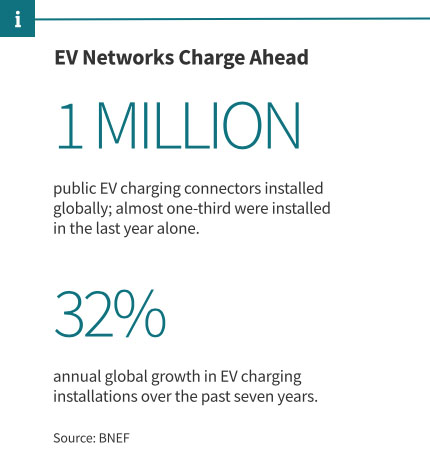

In addition to making EVs more affordable, the charging networks will also need to attract significant levels of investment. BNEF projects that within Europe, the need for expanding EV infrastructure, will create an investment opportunity worth $750 million every year until 2025, and more than $1 billion per year through the decade after that. This could create a myriad of opportunities for active thematic investors.

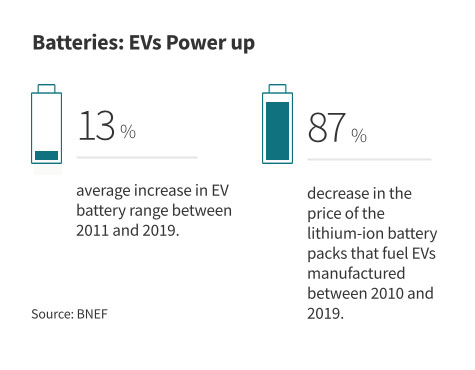

The Million-Mile Battery: In June, Chinese battery maker Contemporary Amperex Technology crossed a major threshold—the development of an EV battery that lasts more than a million miles. The company, which supplies the batteries for Tesla’s and Volkswagen’s EV power units, announced 16 it is ready to produce a battery with a 16-year, 1.2 million mile lifespan. This industry landmark could help automakers convince skeptical motorists to move to EVs.*

*Stocks shown for illustrative purposes only and should not be considered as advice or a recommendation for an investment strategy.

Are Trends Electric? A Helping Hand for EVs

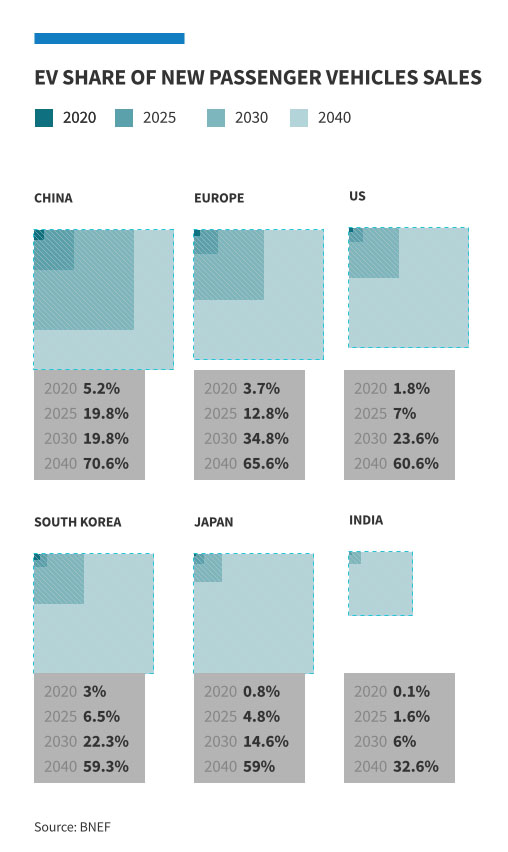

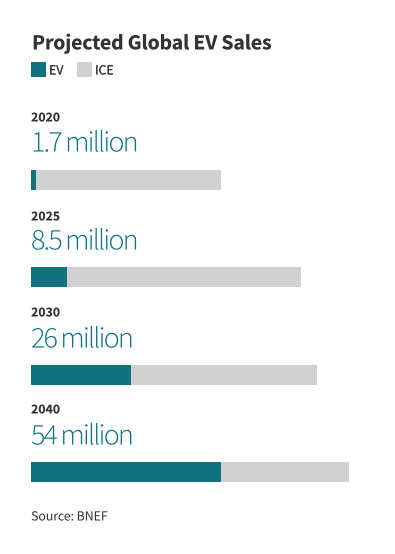

As part of the overall global transport picture, EV numbers remain comparatively small, despite the rapid growth. In its latest Long-Term Electric Vehicle Outlook 17, BNEF calculates that there will be 1.4 billion passenger vehicles on the road in 2030, with EVs accounting for just 8% of them. However, with the decline of oil, increasing environmental pressure and ever-improving range and cost competitiveness, this figure could rise to 31% by 2040 as the global fleet transitions to electric-powered transport.

In spite of ongoing technological advancements, EVs remain reliant on incentives to make a dent in the market dominance of combustion engine vehicles. According to AXA IM’s Amanda O’Toole: “The sort of schemes like the European Union (E.U.) Green Recovery help to support the market and are clearly positive, but I still think there's a lot left to do.”

A number of governments have been keen to bolster the adoption of EVs through subsidies and tax incentives. In 2020, direct purchase subsidies for EVs ranged from over $2,100 in India to a maximum of $14,700 in Singapore, while in some countries EVs can cost as little as a mobile-phone contract 18.

Keen to secure a greener future for Europe, Ursula von der Leyen, President of the European Commission, described the plan to make the E.U. the world’s first carbon-neutral continent by 2050 as a “man on the moon moment.” 19 Within the E.U.’s $1.1 trillion Green Deal economic stimulus package, up to $90 billion has been earmarked to increase EV sales. There is also a plan to double investment in charging networks and to exempt EVs from sales tax.

“The [younger] generations have forced governments to recognize that it has to be a stimulus package that is palatable to them,” O’Toole says. “They would consider it unforgivable for governments to be seen propping up some of the old-world industries that they don’t view as being relevant for the future.

BNEF expects a 23% decline in sales of internal combustion engine (ICE) vehicles this year compared with 2019. However, EVs are not immune to the pandemic-driven global economic slowdown either. BNEF research shows that EV sales will shrink this year, falling 18% to about 1.7 million units, but they are likely to return to growth over the next four years, topping 6.9 million by 2024.

“I think in the short term, what we’re seeing is a fairly cyclical drop in demand for autos,” says O’Toole. “Some people are worried about the economic future and are not out buying a new car. But I’m more optimistic about the medium term, and certainly optimistic about the longer term.”

EVs Offer Asia a Chance to Clear the Air

In China, support for the EV industry is an official priority. In addition to a $30 billion plan to create a series of EV towns 20, the government recently announced 21that it is extending the tax exemption on new EVs to the end of 2022 (although new electric vehicle subsidies will be cut 10% this year). To maintain its number-one position in the EV market, China’s aim is to increase EVs’ share of new auto sales from 5% currently to 25% in just five years. This ambitious target is partly a response to the economic woes caused by the pandemic, but China also has more reason than most nations to clear the air in its cities.

Air pollution problems in Asia’s cities are particularly acute. The drive to quickly expand the economies of China and India, in particular, means that the region is home to many of the world’s most polluted cities 22. In terms of the effects of air pollution in the name of progress, the price has been high.

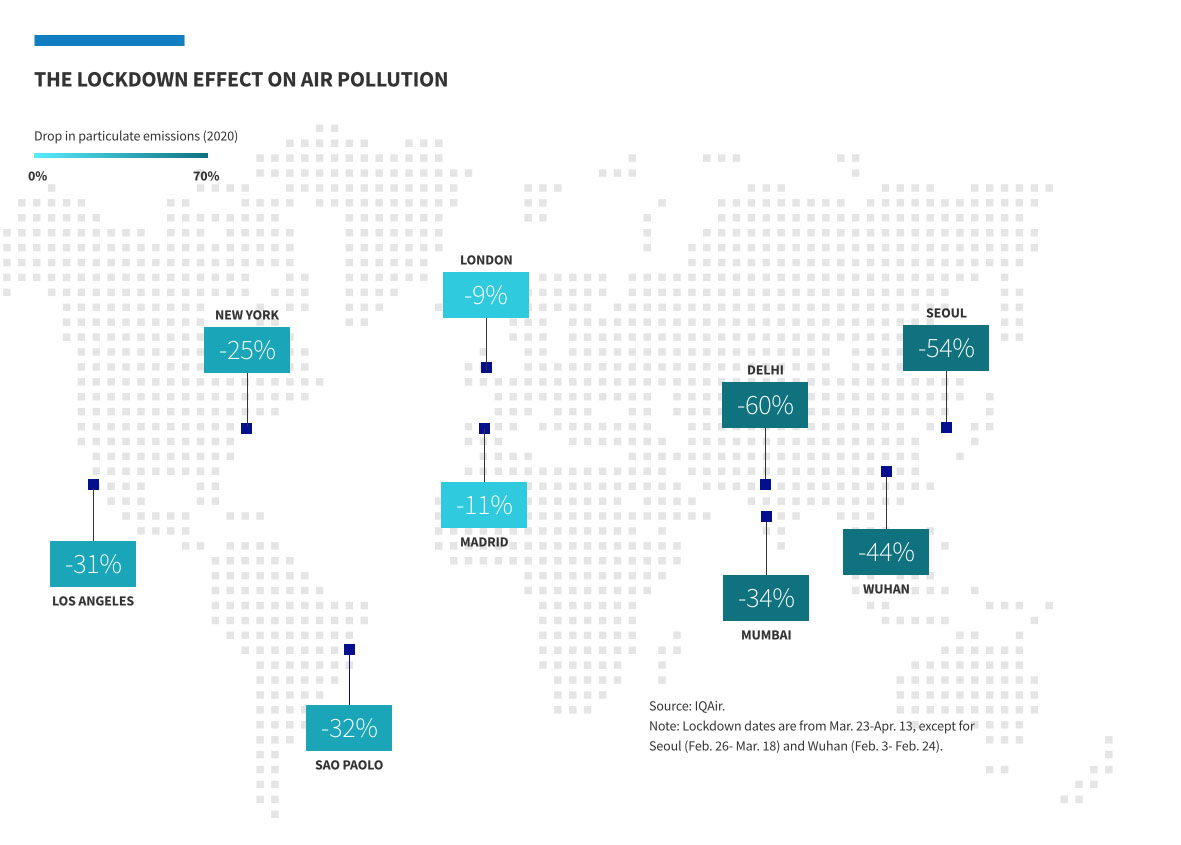

China’s air pollution is so extreme that in 2015, independent research group Berkeley Earth estimated that it contributed to 1.6 million deaths per year in the country. In India, a report on the effect of the Janta Curfew 23 (the nationwide March 22-23 lockdown) on air quality found that the reduction in the number of on-road vehicles resulted in a 51% reduction in nitrogen oxide levels and 32% reduction in CO2 as compared with March 21.

With a growing and increasingly affluent urban population, India is also looking toward EVs as a solution to tackle its transport pollution problems. Last year, a mix of corporate and private equity investors were responsible for $397 million invested 24 in EV-related startups, up from $150 million in 2018.

Elsewhere in Asia, Singapore25, Japan, South Korea26and Taiwan27 have also pledged to phase out petroleum-fuelled vehicles, while investing in and incentivizing adoption of EVs—signalling a potentially strong long-term investment opportunity.

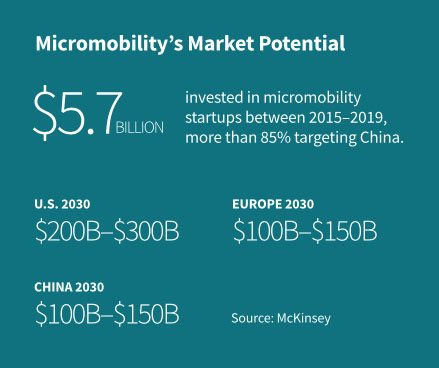

The Market for Micromobility: In 2020, the smaller, micromobility EVs, with two or three wheels, are leading the way. Almost 250 million of these electric vehicles are on the road today. Chinese consumers will buy an estimated 18.2 million electric two-wheelers this year and by 2040, BNEF expects the world will buy 70 million of them annually. However, this is not the first time the prospect of a micromobility revolution has ridden into view. In 2018, early success in bike rental and sharing led to oversupply in the market and bike “graveyards,” as the trend for two-wheeled transport turned sour. It does appear that the next generation of bike-sharing businesses are taking a more measured approach. In China, for example, bikes will be connected to the domestic BeiDou 28 navigation system to improve operations and offer more precise positioning data to manage the fleet.

The Environmental Impact of EVs: How to Keep the Skies Blue

In a world weaning itself off the internal combustion engine, the need for gasoline will be overtaken by a growing demand for renewable electricity. By 2040, EVs will account for 9% of the world’s total electricity demand, and for air quality to improve (without drastic global lockdowns), the energy that powers the EV revolution needs to be equally clean.

Yo Takatsuki of AXA IM points out that in Australia “public transport networks are being fuelled by electricity generated by coal fired power stations. You need to be mindful that ultimately the source of energy is really what we need to be questioning first and foremost. And then the demand side of how we're using it.”

Through initiatives such as the E.U. Green Deal, along with improving technology and increasing investment 29, the renewable sector will shift power generation away from fossil fuels and toward a global economy increasingly powered by clean energy. BNEF calculates 30 that the MWh cost of generating electricity from wind and solar power has fallen 49% and 85%, respectively, since 2010 making them cheaper than new coal and gas plants across two-thirds of the world. Overall global installed capacity is forecast to shift from 57% fossil fuels today to two-thirds renewable sources by 2050.

“When it comes to energy generation, it’s clear that some countries are already considering whether to turn back on the most polluting forms of energy generation, which are inevitably coal, first, and then other types of fossil fuels,” observes Takatsuki. “But the U.K. has accelerated its reliance on renewable energy as the base energy [source]. That’s been a big miracle that’s happened in the U.K., and we may see similar patterns replicated elsewhere.”

The Investment Outlook for EVs

Through subsidies, incentives and regulation, governments are keen to see an end to combustion-powered vehicles. Automakers are responding, with ambitious plans to transition to EVs 31. While challenges around improving battery performance will draw large-scale investment32, so too will EV charging infrastructure33. The scale of the transition to EVs will require input from a range of industries beyond automakers, with technology companies34 and power companies35 and utilities 36 forming part of a wider investment opportunity for the EV sector.

With 10 years left to meet the Paris Agreement that aims to limit the Earth’s temperature rise to less than 2C, investors are looking to industries that offer sustainable returns37. According to Bloomberg, the value of global sustainable investments totaled $30.7 trillion38 last year, a 34% rise in two years.

The era of the EV isn’t here just yet, but if the last century was driven by the combustion engine, this one will be battery-powered. As the world looks for sustainable solutions that help it deal with the wide-ranging effects of the pandemic and the urgent challenge of climate change, EVs offer an opportunity to invest in both.

- https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/micromobilitys-15000-mile-checkup

- https://www.bloomberg.com/opinion/articles/2020-03-25/coronavirus-how-to-make-locking-down-2-6-billion-people-work?sref=mxFiG2OM

- https://www.iea.org/topics/transport

- https://www.bnef.com/flagships/ev-outlook

- https://www.statista.com/statistics/574151/global-automotive-industry-revenue/

- https://www.bloomberg.com/news/articles/2020-05-10/the-car-is-staging-a-comeback-spurring-oil-s-recovery

- https://www.c40.org/press_releases/taskforce-principles

- https://www.bloomberg.com/news/articles/2020-07-04/bicycles-are-pushing-aside-cars-on-europe-s-city-streets

- https://www.bloomberg.com/news/articles/2020-05-18/coronavirus-bicycle-sales-surge-in-america

- https://www.bloomberg.com/news/articles/2020-07-01/rental-e-scooters-will-be-legal-on-u-k-roads-from-this-weekend

- https://www.gov.uk/government/news/2-billion-package-to-create-new-era-for-cycling-and-walking

- https://www.gov.uk/government/speeches/transport-secretarys-statement-on-coronavirus-covid-19-12-june-2020

- https://www.un.org/sustainabledevelopment/decade-of-action/

- https://www.bloomberg.com/news/articles/2020-07-12/tesla-shaves-3-000-off-model-y-price-months-after-sales-start

- https://www.autocar.co.uk/car-news/best-cars/top-10-best-electric-cars

- https://www.bloomberg.com/news/articles/2020-06-07/a-million-mile-battery-from-china-could-power-your-electric-car

- https://about.bnef.com/electric-vehicle-outlook

- https://www.bloomberg.com/news/articles/2020-07-15/electric-car-subsidies-have-rendered-renaults-free-in-germany

- https://www.bloomberg.com/news/articles/2020-07-15/electric-car-subsidies-have-rendered-renaults-free-in-germany

- https://www.bloomberg.com/news/articles/2019-06-02/china-s-spending-30-billion-to-assemble-its-electric-detroits

- https://www.china-briefing.com/news/china-electric-vehicles-hybrid-vehicles-industry-incentives-extended-investment-new-infrastructure/

- https://www.bloomberg.com/graphics/climate-change-data-green/air-quality.html

- https://cpcb.nic.in/air/NCR/jantacurfew.pdf

- https://www.business-standard.com/article/companies/corporate-pe-investments-in-ev-start-ups-grow-170-in-2019-to-397-mn-119120301052_1.html

- https://www.bloomberg.com/news/articles/2020-02-18/after-dismissing-musk-s-jibes-singapore-is-welcoming-evs

- https://theclimatecenter.org/wp-content/uploads/2020/03/Survey-on-Global-Activities-to-Phase-Out-ICE-Vehicles-update-3.18.20-1.pdf

- https://www.intechopen.com/books/energy-management-for-sustainable-development/electric-vehicle-promotion-policy-in-taiwan

- https://www.scmp.com/tech/apps-social/article/3091368/chinas-bike-sharing-platforms-connect-beidou-satellite-navigation

- https://www.bloomberg.com/graphics/climate-change-data-green/investment.html

- https://bnef.turtl.co/story/neo2019/

- https://cleantechnica.com/2018/10/29/worlds-10-biggest-automakers-their-ev-plans/

- https://www.bloomberg.com/news/articles/2018-11-06/the-battery-boom-will-draw-1-2-trillion-in-investment-by-2040

- https://www.bloomberg.com/news/articles/2020-06-23/electric-car-charging-stations-are-finally-about-to-take-off

- https://citywire.co.uk/wealth-manager/news/axa-ims-five-stocks-to-play-the-auto-tech-revolution/a1130077#i=4

- https://group.vattenfall.com/press-and-media/news--press-releases/pressreleases/2018/vattenfall-aims-for-leadership-in-ev-charging-infrastructure

- https://www.woodmac.com/press-releases/strategic-vendors-and-european-utilities-dominate-ev-charging-ma-activity

- https://www.bloomberg.com/news/articles/2020-07-06/global-pension-giants-start-green-investing-tool-to-rank-firms

- https://www.bloomberg.com/news/articles/2019-04-01/global-sustainable-investments-rise-34-percent-to-30-7-trillion

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial, and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee that forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document are provided based on our state of knowledge at the time of creation of this document. While every care is taken, no representation or warranty (including liability toward third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision. Issued in the U.K. by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the U.K. Registered in England and Wales, No: 01431068. Registered Office: 155 Bishopsgate, London, EC2M 3YD (until 31 Dec 2020); 22 Bishopsgate, London, EC2N 4BQ (from 1 Jan 2021).

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.