COVID-19, economic stimulus and monetary policy... How is Japan responding to the crisis?

- 06 May 2020 (5 min read)

Key points

- Until recently, in relative terms, Japan has not been as heavily impacted by the spread of the coronavirus pandemic. However, Japan’s official cases have increased in recent weeks, leading the government to declare a state of emergency.

- Most sectors will suffer from these lockdown measures, with the likely exception of the healthcare and IT sectors. We estimate the lockdown will cost six to eight percentage points of GDP in 2020.

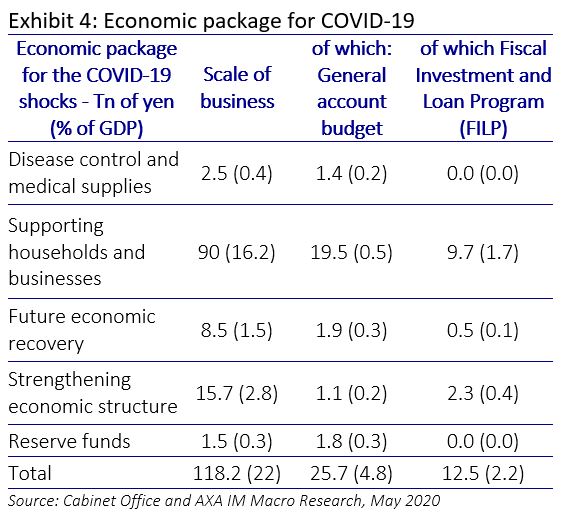

- In parallel, Prime Minister Abe has announced a massive economic stimulus. The total programme size should reach ¥118tn ($109bn), or about 22% of GDP, including a planned ¥100,000 grant per person. Effective fiscal spending is likely to be a much smaller ¥25.7tn (4.8% of GDP).

- Once again, a consensus has emerged amongst Japanese politicians that companies and households should prioritise job security over wage levels.

- Given the latest developments, the Bank of Japan enhanced monetary easing through further – and ample – fund supply, including purchases of JGBs and dollar funds-supplying operations, as well as measures to ease corporate financing and active purchases of ETFs.

State of emergency

Until recently, in relative terms at least, Japan has not been as heavily impacted by the spread of the coronavirus pandemic. Until 7 April, when the first state of emergency was announced, Japan officially had 3,900 confirmed cases and 93 deaths. However, cases have since grown to approximately 15,000, which resulted in the declaration a nationwide state of emergency on 16 April – just before the Golden Week holiday. However, Japan’s current situation cannot be compared with the lockdown in Europe. In Japan, the law does not empower prefectural leaders to punish those who do not comply, while some businesses are still open, and many employees continue to commute.

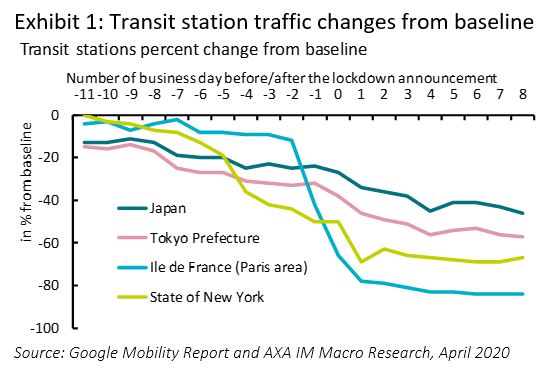

Tokyo has seen a gradual decline in footfall in transit stations since the initial spread of the virus in its closest neighbours, China and South Korea. But more than two weeks after the state of emergency announcement, the decline in transit station traffic is less than seen in Paris or New York. And without strict lockdown, there is a risk of a longer-than-expected mild state of emergency (Exhibit 1).

Estimating the lockdown’s impact

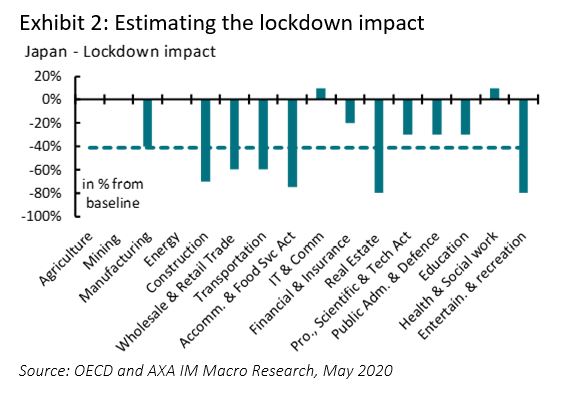

The effect of the Japanese lockdown is likely to have a marked impact on most sectors. The key exceptions are likely to be healthcare and IT. Factories are likely to stand idle, while households are adapting their consumption and reallocating most of their spending to food and other staple products. Services such as transport are also likely to face a massive decline in activity. Beyond that, leisure activities and travel are banned. The most crucial economic sector is consumption which accounts for 56% of GDP. Based on a bottom-up approach, we have estimated the cost of the state of emergency by main sectors (Exhibit 2). Assuming containment lasts at least eight weeks, we believe it could cost six to eight percentage points of GDP in 2020.

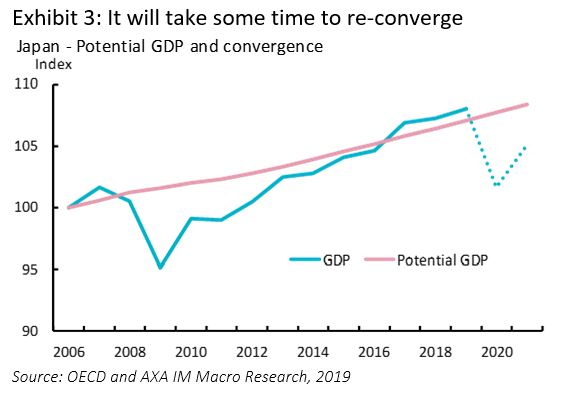

We acknowledge a significant uncertainty in such an assessment. Although Japan’s lockdown seems less severe than Europe’s, a “mild” lockdown could persist for longer. Overall, we estimate GDP is likely to drop to -5.8% in 2020, but a slow and gradual recovery should help it rebound to 3.3% in 2021. However, we estimate that it will take several years before Japan returns to a positive output gap (Exhibit 3).

What kind of economic stimulus is required?

In response to the expected economic shock, Prime Minister (PM) Abe announced a massive economic stimulus. The total programme size should reach ¥117tn ($109bn), or about 22% of GDP (Exhibit 4).

Most of the strategy is oriented towards supporting households and businesses (¥90tn –16.2% of GDP). Each citizen will receive a ¥100,000 grant (¥13.3tn in total) while some small and medium-size enterprises (SMEs) and individual business owners will receive some support through cash and financing support (¥6.2tn). Thus, there will be a deferment of tax and social security payments for SMEs (¥26tn) but we do not account for them in direct fiscal spending, as it will probably be paid in the coming months. The government enhanced its support by including private-sector investment as well as loans and loan guarantees from public financial institutions, such as the Fiscal Investment Loan Program (FILP) and other policy banks.

Among other measures, the government announced ¥2.5tn (0.5% of GDP) to prevent the spread of the virus and bolster the healthcare system and ¥25.7tn (4.8% of GDP) for the economy after the crisis. Key measures include subsidy vouchers to support tourism, promoting local economy and supply-chain diversification, agricultural subsidies and enhanced use of IT in SMEs and schools.

Within the package, we believe direct fiscal spending is likely to be a much smaller ¥25.7tn (4.8% of GDP).

Spill-overs into the labour market

Once again, a consensus has emerged among politicians, companies and households to prioritise job security rather than wage levels. To achieve this, the Employment Adjustment Subsidy Program (EASP) has been recently reinforced. The government has loosened the conditions of the plan during this economic downturn to heavily subsidise firms’ costs of temporarily furloughing workers. From 1 April, until June 30, the government:

- Lowered the cut-off from drops in production/sales required for businesses to qualify for the programme

- Expanded coverage to include workers who were not part of the employment insurance (non-regular)

- Increased the benefit (subsidy rate) to as high as 90%.

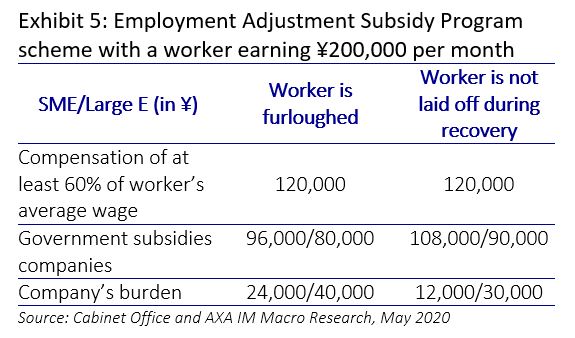

In concrete terms, companies whose monthly production/sales fall by more than 5% year-on-year (yoy) are eligible. Employers provide 60% of workers’ average wages if they furlough workers. The government will subsidise 80% of the cost for SMEs (two-thirds for large corporates). For companies that do not make workers redundant, subsidies will account for 90% for SMEs and 75% for large corporates. The subsidy is capped to ¥8330 per employee, per day (Exhibit 5).

For companies, the main problems with this scheme are the administrative burden, especially for SMEs, and the time to receive pay-outs – estimated to be two months. However, the government has promised to shorten this time length.

Job security is clearly Japan’s priority, but some SMEs are unlikely to be able to support this burden. Direct cash handouts to SMEs were also part of the latest fiscal package, to mitigate such concerns. Looking forward, companies are likely to decrease the burden by reducing the hours worked by employees and then by starting to lay off part-time workers, especially in the case of a soft recovery.

Estimating the unemployment trend

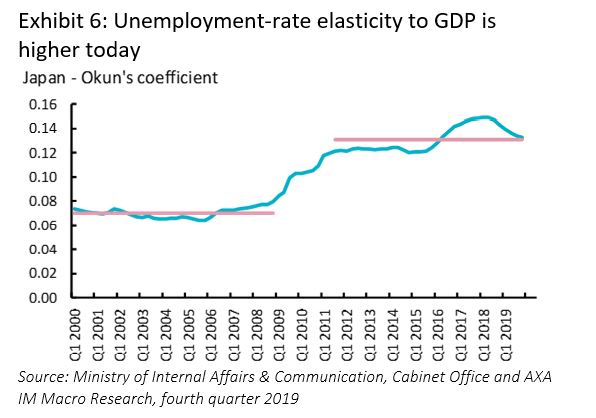

Okun’s law is a relationship between the unemployment rate and economic activity.

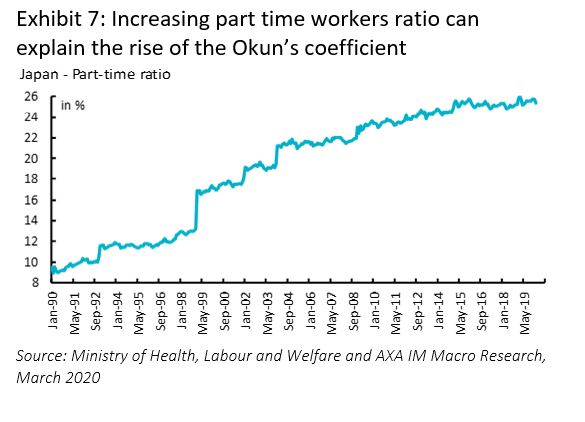

We estimate a dynamic (20-year rolling) model to consider the structural change after 2008. Exhibit 6 illustrates that unemployment’s elasticity to GDP is approximately twice as important as it was in 2008. This is at least in part likely to reflect the increasing share of part-time workers in the economy. Effectively, they are often the first to be laid off during a recession, and a rise of the ratio – towards a more flexible labour market for companies – can explain the recent elasticity increase (Exhibit 7).

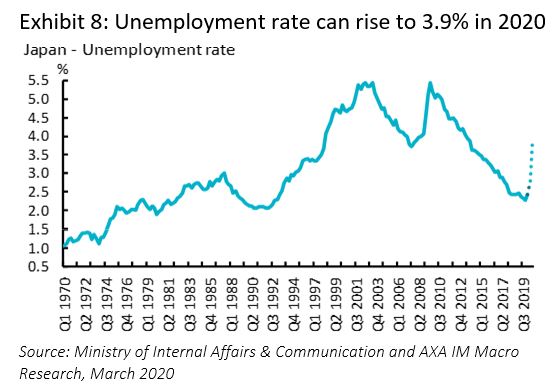

Based on this estimate, our forecast of a major drop in Japanese second quarter (Q2) GDP (-10.2%yoy), should see the unemployment rate rise by +1.5 percentage points, reaching 3.9% in Q3 2020 (Exhibit 8).

Two additional factors bring uncertainty:

- Elasticity shifted higher during the global financial crisis. This could be repeated during this phase, meaning companies could incorporate a new normal in terms of expected future demand and adjust their staff in real time. This presents upside risks to our forecast.

- The long-term trend of labour shortages due to deteriorating demographics favours job security. Labour shortages are expecting to increase further by approximately 7% over the next 10 years, and forward-looking firms may attempt to hoard labour more now, to avoid struggling to rehire workers in the future. This presents downside risks to our forecast.

The Bank of Japan is stuck

In response to the financial market turmoil and COVID-19 spreading, the Bank of Japan (BoJ) has announced additional accommodation:

- US dollar funds supplying operations in conjunction with the Federal Reserve

- Raising the annual purchase target of exchange-traded funds (ETFs) and Japanese Real Estate Investment Trusts to ¥12tn (from ¥6tn) and ¥180bn (from ¥90bn) respectively

- Conducting further active purchases of both Japanese government bond (JGBs) and Treasury bills and removing the target of net JGB purchases

- Increasing the upper limit of commercial papers and corporate bonds purchases to ¥20tn in total and introduce a “Special Funds-Supplying Operations to Facilitate Corporate Financing”.

The “Special Fund” provides loans against private debt in general (including household debt) as collateral at an interest rate of 0% with maturity of up to one year. Twice as much as the current amount outstanding of the loans will be included in the Macro Add-on Balances in current accounts held by financial institutions at the BoJ (the middle tier at 0% in the tiering system), while a positive interest rate (+0.1%) will be applied to the amounts outstanding of loans provided. This operation clearly supports financial institutions to further fulfil the functioning of financial intermediation. It will be conducted until the end of September 2020.

In addition, the BoJ is designing a measure with the aim of further supporting financing small and medium-sized firms, taking account the government’s programme.

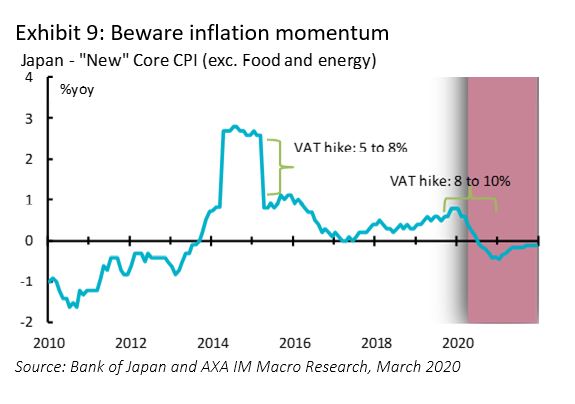

Beware of inflation momentum

As in many parts of the world, the BoJ will also face issues with inflation momentum. The sharp drop in oil prices will weigh on inflation in the short term, while the negative output gap should dampen inflation over the medium term. In such an environment, companies are not likely to raise prices, especially after the sales tax (VAT) hike from 8% to 10% in October 2019. We believe the “new” core Consumer Price Inflation (CPI) rate (excluding energy and food) is likely to converge to 0.1% in 2020, on average, and only -0.2% in 2021 (Exhibit 9). But we also note that even before the pandemic, Japan had fought a war with deteriorating inflation expectations – which it had recently started to win. These developments risk resuming a downward trend in inflation expectations, which could reawaken deflation concerns in Japan.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.