Purchasing power and greater connectivity: The EM debt opportunity

- 05 July 2021 (7 min read)

As the number of working age people across emerging markets expands, consumption patterns are changing, creating new opportunities for fixed income investors.

Greater demand for consumer-driven sectors could potentially start to improve the corporate fundamentals of companies in these areas and have a positive impact on their long-term credit quality.

According to one recent study1 , 89% of Generation Z – those born between the mid-1990s and mid-2010s – live in emerging markets. As that generation reaches working age, their global income is forecasted to increase five-fold to more than $33trn by the end of this decade, creating a significant boost in disposable income for developing market workers.

GDP growth bounces back

After contracting by 2.2% in 2020, emerging market GDP is expected to grow by 6.0% this year but its contribution to global economic growth is projected to reach 60% by 2025 – in parallel with its younger populations’ greater mobility.2

As emerging markets move up global supply chains, this is generating a growing demand for skilled labour; a trend encouraging many workers to flock to urban areas in search of higher wages and a better quality of life. These shifts are also reflected in the infrastructure development of rural areas to match urban levels, and by changed consumer patterns in these regions.

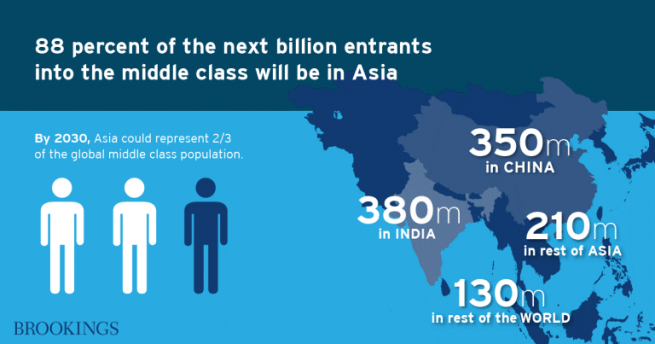

As a result we are seeing a huge surge in the emerging market middle classes, particularly in Asia which is expected to represent two-thirds of the global middle class by 2030.3 As disposable income increases, it is creating greater demand for higher-priced goods as well as a wider variety of choices across sectors such as food, transport, fitness and more, representing a shift in consumption patterns from necessary to discretionary spending.

- QmFuayBvZiBBbWVyaWNhLCBEZWNlbWJlciAyMDIw

- U291cmNlOiBEYXRhc3RyZWFtLCBJTUYgYW5kIEFYQSBJTSBNYWNybyBSZXNlYXJjaCDiiJIgQXMgb2YgMjQgSnVuZSAyMDIx

- QnJvb2tpbmdzIEluc3RpdHV0ZSwgRmVicnVhcnkgMjAxNw==

New opportunities for emerging market fixed income investors

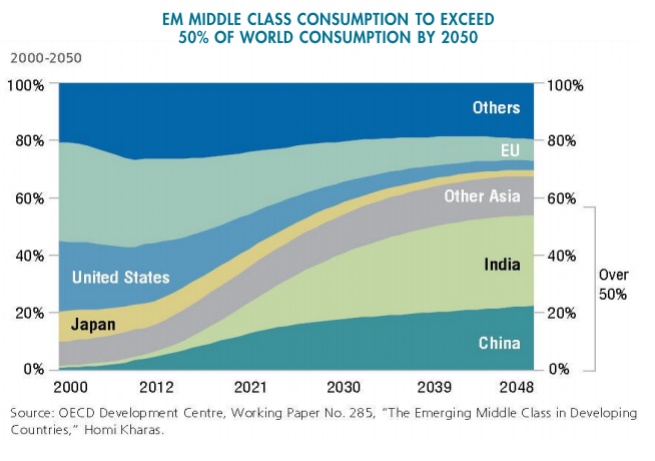

More than 70% of global consumption is expected to come from the emerging markets middle class by 2050. India’s domestic consumption alone is estimated to hit $6trn by 2023, four times its 2018 level – the current combined domestic consumption of France and Germany is around $5trn. This increase in spending is likely to offer opportunities for global brands diversifying into emerging markets or domestic companies with a proven track record, both of which represent strong potential for investors. For example, Brazilian global personal care cosmetic group Natura, which owns the Avon and Aesop brands, has seen rapid expansion as demand for its products has soared.

Greater connectivity and tech adoption

Another consequence of the change in demographics is that emerging market countries are rapidly gaining greater access to, and adopting, technology. As a result of their younger working population, a lot of the workforce are from generations that typically consume greater levels of online content. Growth in connectivity is closely associated with improved productivity, and many emerging market countries are poised for a surge in online users, accelerated by the COVID-19 pandemic.

China and India have two of the largest digital markets worldwide, with a combined online population of over 1.3 billion. However, they also have huge market potential; China’s online participation is only 59% while India’s untapped market is larger than the entire population of Europe. Looking at internet growth over the last 20 years, Bangladesh has seen the greatest increase at over 94%, while Nigeria sits second at 63%4 .

- aW50ZXJuZXR3b3JsZHN0YXRzLmNvbSwgYXMgYXQgSnVuZSAyMDE5

On the back of this increase in demand for technology, we have seen the rapid growth of tech giants in emerging markets, with China in particular a clear example of this. Alibaba is the country’s dominant online retailer and could potentially rival the growth of Amazon as the country’s consumer market grows. Other examples include Baidu and Tencent, both of which are exhibiting rapid growth as consumer demand surges. Meanwhile Chinese brands Huawei and Xiaomi now represent almost 25% of the global market for smartphones, a huge market share.5

Elsewhere, in Latin America online retail platforms such as Mercado Libre and B2W Companhia Digital have enjoyed huge growth as online participation has soared in the region.

The increase in 3G/4G network volume and coverage is speeding up technological adoption, as well as lowering of the cost of data of smart phones making them more economical. By continuing to contribute to these structural improvements through technological innovation, investors could be able to tap into the economic growth of emerging markets.

As companies in these sectors continue to grow, fixed income investors should expect improvements in debt sustainability, greater business stability and a source of steady income, which we believe is the long-term driver of successful returns in bond markets.

- R2FydG5lciwgRGVjZW1iZXIgMjAyMA==

Disclaimer

All stock/company examples are for explanatory/illustrative purposes only. They should not be viewed as investment advice or a recommendation from AXA IM.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ.

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.