When it comes to market volatility, sometimes it’s best to stay put

- 06 April 2022 (5 min read)

The coronavirus pandemic and the recent escalation of military conflict in Ukraine have caused significant volatility in financial markets.

Global stock markets plunged in early 2020 as COVID-19 swept the world, before recovering as governments and central banks launched unprecedented stimulus and, later, vaccines and treatments for COVID-19 were developed. As economies came out of lockdown, many equity indices hit record highs in 2021.

Russia’s subsequent invasion of Ukraine triggered a sell-off in global stock markets and sent the price of oil above $100 a barrel for the first time in seven years. The war has taken a considerable toll on the country and its people – while the uncertainty over the path and duration of the conflict and the impact on economic growth in Europe has had a far-reaching impact on financial markets.

This kind of volatility can, naturally, be unsettling for investors. But the reality is that there are always events taking place around the world that can cause investor sentiment to sharply change direction. And difficult as it might be, sitting tight and doing nothing can often be the best course of action for investors when markets turn turbulent.

This is because investors who delay putting their capital to work in the hope that prices will fall further, or who sell in the hope that they will be able to buy again at the bottom of the cycle, risk missing out on some of the potentially best gains.

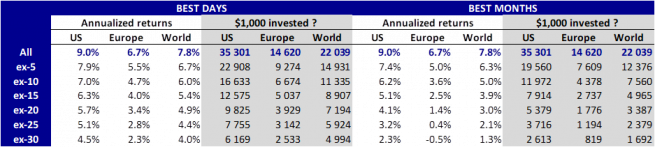

Past performance should not be viewed as a guide to future returns. But to illustrate the potential benefits of thinking long-term, if an investor put $1,000 into the MSCI World Index 40 years ago, they would since have seen that lump sum grow to $22,039, equivalent to an annualised total return of 7.8%, as at end December 2021 (see table below).*

However, if they’d missed just five of the best days over that four-decade period, their annualised return would have been 6.7%, leaving them with a far lower $14,931.

And if they had missed the 30 best days, they would have endured an even more dramatic impact on their returns, accumulating just $4,994 after 40 years, equivalent to an annualised total return of 4%.

Regional variations

The difference in performance between remaining invested and missing some of the best days can be even more pronounced when looking at specific regions. For instance, if an investor had put $1,000 into the MSCI US Index 40 years ago, their investment would currently be worth $35,301, an annualised total return of 9%.

Missing 20 of the best days would see the value of their investment dwindle to just $9,825, a total annualised return of 5.7%, while missing 30 of the best days would mean their investment would have grown to only $6,169.

Similarly, if an investor had put $1,000 into the MSCI Europe Index 40 years ago, and remained invested the whole time, they’d have achieved an annual return of 6.7% and have $14,620. If they missed the best 30 days, their annualised return would be just 2.3%, and their investment would be worth $2,533, some $12,087 less than if they’d stayed put.

The importance of staying invested

It’s extremely difficult for any investor to predict which way markets are going to move next, certainly with any consistency, but as the numbers highlight missing just a few of the best days can significantly impact total returns.

Remaining invested over the long term will hopefully give any investments which do fall in value when markets are volatile plenty of time to recover. It also means trading costs are kept to a minimum because you won’t be buying and selling frequently.

It’s important to remember too that if you are investing regularly, periods of turbulence may work to your advantage, as you’ll be buying more shares when prices are low and less when they cost more. This can help smooth out your returns over the long term, although of course there are no guarantees and there’s still the risk you could get back less than you put in.

Thinking long term and staying diversified

Investing is a long-term endeavour and the more time you give your portfolio, the greater the chance it has of delivering positive returns and the better it can harness the power of compounding. Therefore, we believe the best way to tackle market volatility is to be prepared for it. This means maintaining a well-diversified portfolio, where your money is spread across a wide variety of different investments including equities, bonds, property and cash.

Disclaimer

*All performance data source: MSCI and AXA IM Research. All calculations done using MSCI indices over the last 40 years ending December 2021

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.