Institutional investors can look to new diversification opportunities in the pandemic recovery

- 25 June 2021 (5 min read)

The global economy is recovering from the worst of the damage done by the COVID pandemic. Vaccination programmes and a careful relaxation of managed restrictions on activity have allowed economic activity to recover strongly in developed economies. Many countries are on track to reach levels of economic activity that they would have reached without the pandemic by the end of this year or at some point in 2022.

At the same time, inflation has picked up driven mostly by frictions created by supply chains being disrupted and demand coming back quickly. Markets in early 2021 have been focused on inflation and whether this means interest rates will be increased ahead of the timing suggested by global central banks like the Federal Reserve and the European Central Bank (ECB).

Despite the better economic outlook, it is very likely that fixed income markets will still be characterised by the “lower for longer” outlook for interest rates and bond yields. The increase in long-term yields in 2021 has taken levels back to where they were just before the COVID crisis. Yields remain low by historical standards. As such, building asset portfolios to match liabilities and deliver additional income will continue to be a challenge for insurance companies, pension funds and other long-term investors.

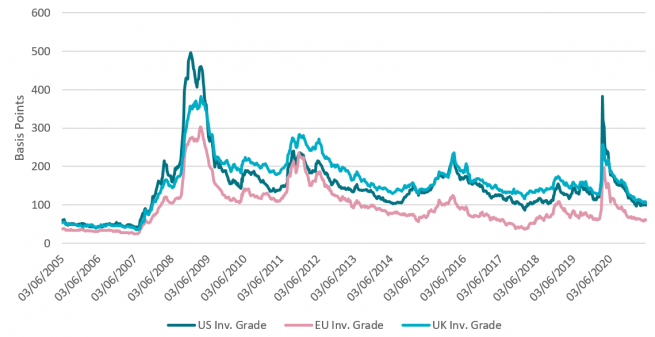

For European investors with liabilities in sterling or euros, the environment remains one of very low bond yields and credit spreads – the additional yield provided by corporate bonds relative to swaps or government bonds – which are at their tightest levels since before the global financial crisis. A quarter of the European Corporate Bond Index (BAML ER00) currently trades with a negative yield-to-worst with over 60% of the issues in the index currently priced with a spread over government bonds of less than the 86 basis points weighted average for the index as a whole.1 In the UK corporate bond market, spreads over government bonds are at their lowest since before the global financial crisis in 2008.

- U291cmNlOiBJQ0UtQkFNTC4gRGF0YSBhcyBvZiAyNSBNYXk=

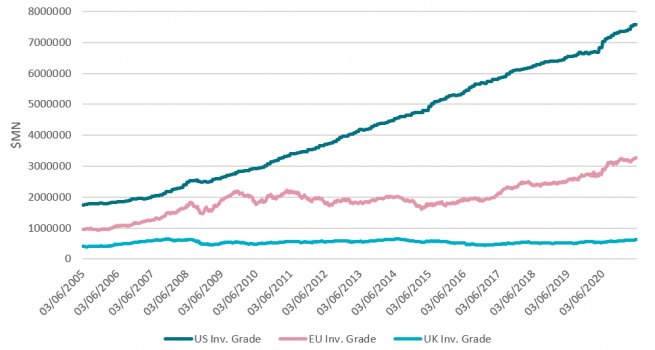

Investors who seek to broaden their universe beyond their domestic market could benefit from greater diversification, a more optimal sector allocation and higher spreads. For Europe-based investors, there can be opportunities to achieve a more diverse portfolio, with longer-duration and higher spread by allocating to the US dollar market, for example. If we look at the European investment grade market today it represents around 25% of the global credit market (the UK market accounts for just 5.4%). The US represents 60%.2

- U291cmNlIElDRS1CQU1MLiBEYXRhIGFzIG9mIGVuZC1NYXkgMjAyMQ==

The European market has a duration of just over five years while it is around eight years for the US. The current market yield in the US is 175 basis points higher than in Europe with a slightly higher spread over government bonds. Yields and spreads are also higher in the US than in the UK corporate bond market3 . Adding some exposure to the US market could potentially create the opportunity for euro-based investors to extend duration, add yield and benefit from increased diversification. Sterling-based investors, of course, would have the option of looking to both Europe and the US.

For institutional investors focused on cashflow driven investment, any potential spread pick-up will be appealing, while the simple act of diversification should improve the stability of cashflows over time. And anything that improves liquidity or opens up access to more issuance for active investors would smooth the process of setting up new mandates, adding to existing ones or rebalancing to exploit pricing differentials.

- U291cmNlIElDRS1CQU1MLiBEYXRhIGFzIG9mIGVuZC1NYXkgMjAyMQ==

Buying assets in a currency that is different to that of the liabilities on the balance sheet creates new risks. One risk is foreign exchange volatility, and another is the risk associated with overseas interest rate moves. Fortunately, both can be hedged. Investors use instruments like cross-currency swaps to hedge the risks associated with exchange rates.

There can be opportunities that allow a European investor to buy a US-dollar-denominated corporate bond with a higher yield than an equivalent euro asset, even when the cost of hedging is factored in. Interest rate differentials and the ‘FX basis’ must be considered. Currently, differences in the shape of the yield curve between the US dollar market and the euro market mean that investors can potentially pick up more spread relative to their liabilities by investing in certain dollar assets.

Global bond markets do tend to be quite correlated. However, idiosyncratic economic developments can generate significant deviations in bond yields across markets. Earlier in 2021, the fact that the US economy appeared to be reopening more quickly than was the case in Europe pushed US Treasury yields up relative to government bond yields in Europe. This also had an impact on corporate bond yields. In a global credit portfolio, the negative impact of this on valuations can also be hedged by managing the duration exposure in the individual currency buckets. In a euro-US credit portfolio the risk of US rates going up relative to euro rates can potentially be hedged through derivatives like bond futures or interest rate swaps.

There is currently considered to be more risk of interest rates rising in the US than in Europe or in Japan. This is already reflected in a steeper yield curve. European investors who need long duration assets are faced with a limited market in Europe – partly because of the ECB taking more duration out of the European bond market relative to the case in the US.

Adding US credit helps meet the challenge. The over 10-year part of the US credit market currently yields more than 200 basis points more than its equivalent sector in the euro market4 . Hedged into euros and with the US rate duration managed, this could provide a more optimal opportunity than being confined to the euro credit market alone.

The medium-term outlook for bonds is uncertain. Debt levels in both the government and corporate sector have risen sharply through the pandemic. Rates and yields have been kept low by quantitative easing and the huge purchases of bonds from central banks. If central banks start to withdraw support, yields might increase, and credit spreads could widen. This should happen most vividly in the most indebted parts of the market. Our view is that a more diversified credit portfolio could allow investors to improve the credit profile and thus reduce the risk of impairments and credit losses.

Financial theory tells us that being more diversified improves risk-adjusted performance. Global credit markets provide the opportunity for long-term fixed income investors to diversify their credit, economic, interest rate and liquidity exposures. Having an asset manager with the means to deliver global resources in terms of credit analysis, best-in-class credit exposures from an ESG perspective and a strong trading platform to manage liquidity, should allow investors to exploit all the benefits of a global credit allocation.

- U291cmNlIElDRS1CQU1MLiBEYXRhIGFzIG9mIGVuZC1NYXkgMjAyMQ==

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.