On the lookout for leaders as opportunities grow

- 21 May 2021 (5 min read)

It has been estimated that around 75% of the infrastructure that will be needed in 2050 does not yet exist1 . That simple estimate signals significant change ahead for investors – and significant risk for those without appropriate strategies in place.

“Clearly this is a world into which we need to factor our exposure, and the ways we can make this an opportunity rather than a threat to our portfolios,” said Amanda O’Toole, AXA IM portfolio manager.

AXA IM seeks to compartmentalise its approach to better target the most exciting themes. These run from demographic trends such as the rise of middle-class populations in emerging markets, through to digitalisation, automation and the expected surge in renewable energy investment as the world moves to align with the goals of the Paris Agreement on climate change.

- IGh0dHBzOi8vbmV4dGNpdHkub3JnL2RhaWx5L2VudHJ5Lzc1LW9mLXRoZS1pbmZyYXN0cnVjdHVyZS10aGF0LXdpbGwtZXhpc3QtaW4tMjA1MC1kb2VzbnQtZXhpc3QtdG9kYXk=

In the long term, CleanTech may be the biggest opportunity of all, said O’Toole, who is lead portfolio manager on AXA IM’s clean economy strategy. The sector brings together companies that are delivering renewable energy, developing techniques to mitigate environmental risks, or providing the tools to allow more carbon-intensive industries to reduce their impact. The goal is long-term, sustainable growth. “It is essentially everything,” said O’Toole. “Every country, every government, every corporation around the world has to adopt CleanTech solutions. There are costs attached, but the cost of failing to act, every study will tell you, is far greater.”2

Financial imperatives are driving the adoption of cleaner solutions, whether through cost savings, efficiency measures, or to meet consumer demand for sustainable solutions. Reputations and market share are at stake; businesses could be left behind. The longer you leave the transition, the more capital will potentially be needed to make it work – and the more expensive it becomes to pollute, so the more CleanTech solutions could gain prominence.

“This is not a question about whether a particular customer base cares about environmental change per se, it’s just more expensive not to do it,” said O’Toole.

Even markets that prove more reluctant will eventually be forced to move by regulatory pressure, O’Toole believes. “It’s happening and it’s happening everywhere and it’s going to take a really long time to get to where we need to be. That means the opportunity is just enormous and we’re still at the start of it.”

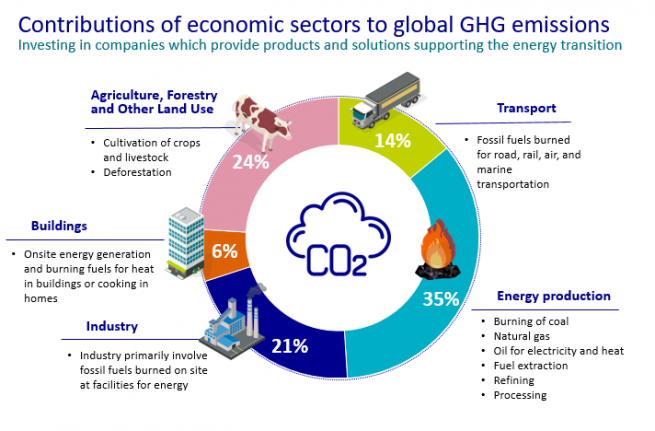

More than 100 countries have pledged to be net zero by 2050 and, overall, some 68% of global GDP is now covered by net zero commitments3 . To give an idea of the speed at which this has happened, in February 2020 that figure was just 49%. In AXA IM’s view, that underpins both the scale and the breadth of the opportunity set, and this is further emphasised by looking at the wide sweep of industries implicated in greenhouse gas (GHG) emissions.

- IGh0dHBzOi8vd3d3LnJldXRlcnMuY29tL2FydGljbGUvdXMtaWVhLWNsaW1hdGUtaWRVU1RSRTVBOTFVNDIwMDkxMTEw

- aHR0cHM6Ly93d3cub3guYWMudWsvbmV3cy8yMDIxLTAzLTIzLW5ldC16ZXJvLXBsZWRnZXMtZ28tZ2xvYmFsLW5vdy1hY3Rpb24tbmVlZHMtZm9sbG93LXdvcmRzLW94Zm9yZC1lY2l1LXJlcG9ydA==

It’s not only about opportunity in a growing, innovative industry. AXA IM’s clients are increasingly thinking about their exposure to climate change, whether that’s through weather events or the cost of carbon. CleanTech is one way that they can start to potentially mitigate against those risks. In effect, the sector can almost act as a potential hedge while investors work through their longer-term strategic approach, she said.

COVID-19 has accelerated digitalisation

As the world grapples with the effects of the pandemic, some of the most compelling ideas have arisen in the connected consumer theme. Corporations have had no choice but to embrace the digitalisation of practically everything, and even as the virus subsides O’Toole expects that trend to continue.

“We continue to see a pick-up. As companies come back and spend, they’re spending on digital advertising, for example. As consumers go out and spend, they’re increasingly using digital solutions.”

Automation, meanwhile, has a potential role in improving supply chains where fragility was revealed by the pandemic. Fully autonomous vehicles remain some way off, but regulatory changes appear likely to drive growth. Automation can also give investors exposure to typically defensive positions through healthcare which is additionally benefitting as economies open back up and the pipeline of delayed surgeries and procedures demands attention. In the medium term, the restructuring of health systems more generally may emerge as a social priority, for investors and governments alike.

Evolving markets need an agile approach

The rise of the Evolving Economy theme has seen valuations move higher, but for O’Toole, this can often be justified. “This is a part of the market that typically attracts a premium. I think it deserves that because we are talking about multi-decade growth opportunities,” she said. And, in O’Toole’s view, they are opportunities that persist across a wide range of GDP and inflation scenarios.

Even if a premium might be warranted, ongoing discipline in portfolio management is crucial to acknowledge how markets evolve. This could potentially mean trimming positions that have outperformed or perhaps simply become outsized in a particular portfolio, or redeploying capital when valuations become stretched relative to the wider opportunity set. That might mean rebalancing away from pure play businesses and looking for those assets that garner less attention, but which share a similar strategic profile.

O’Toole believes it is important to look for leaders in all of the Evolving Economy themes, particularly given the advantage of pricing power in these growth markets. It can also be an advantage to seek out companies with the balance sheet strength to deploy capital where they see powerful arguments to invest in new technology or other innovations.

AXA IM considers the environmental, social and governance (ESG) nature of investments in this space in a “very fundamental way”, in this pursuit of leaders in their fields, said O’Toole.

“We’re looking at companies that we think have business practices and characteristics that should stand them in good stead for the long term,” she said. An important recent focus, for instance, has been on labour practices and staff retention.

“In a strongly growing market one of the inhibitors to growth is often the ability to attract and retain talent, particularly in a tight labour market where the costs are rising.” The best companies in CleanTech, for example, want to be pulling in the very best engineers and scientists so that they can fully exploit the opportunities at hand.

The Evolving Economy encompasses a huge array of investment ideas, from the financial and education services to support an ageing but active population, to the companies starting to clean up extraction methods for battery raw materials – and from circular economy players generating value from waste materials to smart energy infrastructure that seeks to embed efficiency.

O’Toole believes it has become a compelling, exciting landscape, and one that can potentially reward investors who take care to identify the leaders best placed to make the most of structural opportunities. And she added that AXA IM’s active and committed approach to engagement is designed to look for those executive teams with the ability to turn leadership into market growth, market share and resilient margins.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalised recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.