Big Figures Looking Smaller

- 18 May 2020 (7 min read)

Key points

- The ECB's EPP looked massive when it was announced. We are now getting concerned by a pace of purchases consistent with the EUR750bn being spent by the end of the summer.

- A side-effect of QE is a "renationalization" of bond markets.

- The UK is having a lot on its plate at the moment.

The ECB has to deal with a nasty form of circularity: doubts on its capacity to break its self-imposed limits – further fueled by the recent decision of the German Constitutional Court – trigger bond offloading in some of the most fragile countries, forcing the central bank to increase its daily purchases significantly. At the current pace the ECB will have spent the entirety of the current PEPP package by the end of the summer. This in turn forces the central bank to consider raising this quantum much more quickly than expected (possibly at the June meeting already). Doing so may could antagonize the German constitutional further, since a bigger PEPP would be very difficult to implement without doing away with at least one of the red lines explicitly set-up by the GCC, either the capital key of the 33% holding limit.

While we are convinced that massive central bank intervention is the only workable policy at this stage, and probably for long after the recovery from the pandemic starts, we recognize it comes with significant drawbacks. One is that it triggers a “renationalization” of bond markets, with lower participation from non-residents. This could well be temporary, but other trends may contribute to the fragmentation of the global financial markets. The US administration’s interest in “financial decoupling” from China could further drive a hardening of competing “financial blocks”.

The UK is one of the countries where institutional limits to quantitative easing are negligible. The country may need a lot of that. It is facing difficulties to keep the covid pandemic in check, and the clock is ticking on negotiating a good quality Free Trade Agreement with the EU as the government is publicly rejecting the possibility to extend the post Brexit transition period beyond December 2020. Another issue for the UK though is its sensitivity to exchange rate movements, which a combination of the pandemic shock, post-Brexit uncertainty and ultra-accommodative monetary policy may trigger.

The circular firing-squad

We were thoroughly impressed by the European Central Bank (ECB) at the end of March when after some communication glitches they chose to provide massive additional support through the EUR750bn Pandemic Emergency Purchase Programme (PEPP) on top of the EUR120bn boost to the “old” Public Sector Purchasing Programme (PSPP). Together with the announced “flexibility” in the way the usual limits to QE would be implemented, this made us hopeful there would be enough to support governments as they substitute public spending to constricted private expenditure through the pandemic. Unfortunately, the risk that the ECB would “run on empty” much earlier than the end of this year – the provisional term of PEPP – is now very real.

We are faced with a nasty circularity: the doubts on the capacity of the central bank to provide unlimited support, strengthened by the recent German Constitutional Court (GCC) ruling – are fuelling an acceleration in sales of government securities in the most fragile member states, forcing the ECB to buy large quantities of bonds to keep spreads in check. This puts the central bank under pressure to raise its quantum of purchases in the next few Council meetings already, but since this may entail politically sensitive decision on its “limits”, investors may want to further accelerate their off-loading.

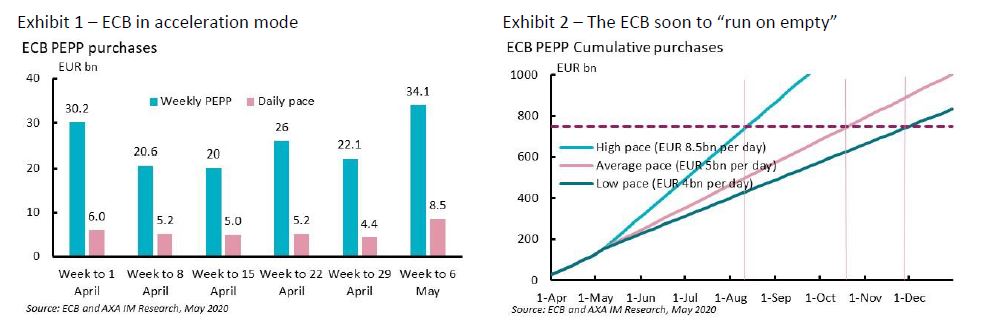

Philip Lane made the readiness to fight “fragmentation” in financial conditions in the Euro area crystal clear in his blog post on 1 May. “In the absence of the stabilising presence of the central bank, a crisis environment can give rise to self-fulfilling flight-to-safety dynamics and illiquidity in individual sovereign bond markets, on account of the high substitutability across sovereign bond markets in the absence of currency risk”. This was echoed by Isabel Schnabel in an interview to La Repubblica on 11 May, and in the post-GCC context it was important it came from the German member of the board: “a divergence of spreads is often a sign of fragmentation, and such fragmentation hampers the smooth transmission of our monetary policy”. This readiness is concretely reflected in the very significant acceleration in purchases in the week to 8 May, with a jump from a daily pace of EUR4.4bn to EUR8.5bn (Exhibit 1).

If such pace is maintained, the PEPP would run out of resources before the end of the summer (Exhibit 2). From the start, the ECB made it plain that they could change the duration and composition of the programme if need be. This does not mean it is going to be easy. The Governing Council needs to deal with two different issues.

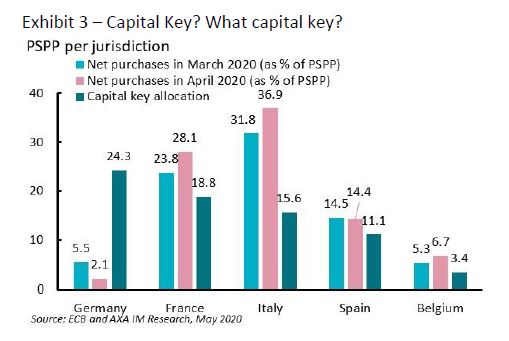

First, on substance, they may have to make a choice between two of their “limits” when raising the quantum of purchases. According to research by Barclays, the Eurosystem’s holdings stood at 29% of eligible German sovereign and “sovereign-like” bonds before PEPP started. With a strict compliance with the “capital key” the ECB would hit the 33% limit within six months under the EUR750bn quantum, assuming a regular distribution of the programme over time. The ECB will start publishing granular data on its PEPP programme only in June (with a bi-monthly frequency), but it is probably a fair assumption, given Christine Lagarde’s insistence on “flexibility” to consider that a very significant deviation from the capital key is at work on the PEPP as well as on the PSPP, through which Italian bonds are benefiting from massive support (their share in PSPP, already public, is now almost twice the share of Italy in the ECB’s shareholding, Exhibit 3). Mechanically, a bigger PEPP quantum will force an even larger deviation from the capital key.

The tactical timing of the decision on PEPP is the second issue. Announcing an increase in PEPP at the 4 June meeting already, before any solution to the legal predicament can be found, could be seen as a “provocation” after the German Constitutional Court ruling. Symmetrically, “staying put” at the next meeting could be seen by the market as a lack of resolve accelerating divestments from the fragile signatures. The ECB would then only have one more chance left, on the 16 July meeting. Based on the purchasing pace of the 8 May week, the central bank will have spent 71% of the PEPP envelope by then. Note that if the purchasing pace had to increase beyond EUR 13bn/day, for instance as a need to counteract miscommunication at the June press conference, all the current PEPP capacity would be spent 16 July. It is always preferable for a central bank to be pro-active rather than being forced into additional action by market forces. On balance, announcing a PEPP extension in June already would be the preferable course of action in our view.

Now, there might be some possible “compromise solutions” for the June meeting. ECB’s communication so far suggests the reinvestment period is considered for “re-converging” towards the capital key. We were disappointed at the last ECB press conference that Christine Lagarde touched upon the reinvestment schedule of the PSPP but chose not to address this when it came to the future of PEPP. This is key, since the longer the reinvestment period is, the easier it would be to slowly move away from the current overweighting of Southern Europe. She could focus on this aspect in June.

Beyond allowing for some delayed but effective compliance with the capital key, a long reinvestment period for PEPP would help deal with the macroeconomic consequences of the pandemic. Since the beginning of the crisis we have been arguing that the duration of the support matters as much if not more than the quantum. If we cannot fully monetise the “debt overhang” which is going to be a likely consequence of the ongoing recession, at least we can endeavour to “sterilize «its market effect. A commitment to reinvest the PEPP over a long horizon would improve debt sustainability conditions by ensuring ordinary investors that a regular, not profit-motivated buyer would remain in the most fragile markets well beyond the recovery is established.

The reinvestment horizon of the PSPP is vague (“for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation”). Still, if the Governing Council considers it is too early to increase would be welcome in our view.

The ECB and de facto yield targeting

In Philip Lane’s narrative on fragmentation which we quoted earlier, “liquidity” is a key word. Implicitly, this means that we could distinguish in each member state’s spread a fundamental level, representative of the “true” risk premium, and a volatile (potentially dangerous) liquidity premium. It is very difficult to quantify this in real time, but in a way the ECB itself is conducting a natural experiment. Investors will be able to guess what is the de facto “fundamental level” that the central bank is targeting by looking at the changes over time in the quantum of purchases on each market. This will not be perfect since the central bank will release only bi-monthly data for market-by-market operations but looking at the weekly total only will already provide a wealth of information. In clear, we should be able to get a fair idea of what the ECB considers the “right” Italian spread to be when we see the volume of purchases fall again from the current peak.

This was by construction impossible under the old version of PSPP since the monthly quantum was fixed. The only way then to gauge the ECB’s level of comfort with sovereign spreads was to try to guess from their communication the likelihood of an acceleration or a deceleration of the pre-set pace for QE.

This suggests the ECB is getting very close to the Bank of Japan’s “yield targeting” approach. A key difference though is that “yield targeting” is hardly consistent with hard limits on the quantum of central bank purchases.

Indeed, in such a strategy, the ECB would have to be ready to absorb the entirety of the outflows from the most “nervous” or the “least captive” categories of investors on a given market. At the extreme, one could think of a national bond market with very few non-resident investors, dominated by local banks (especially since holding sovereign bonds comes with no risk weight in the calculation of their capital ratios) and the central bank. Note that the notion that “the ECB purchases local sovereign bonds” is not exact. Under both PSPP and PEPP 90% of the sovereign bonds are bought and held at their own risk by the national central banks.

Yet, in the case of Italy such “renationalization” of the bond market would not be within the grasp of the central bank under the current rules. Banca d’Italia held c.20% of eligible Italian public debt before PEPP was launched, while non-residents held 30%. By reaching its limit of 33% Banca d’Italia could take over less than half of the foreign investors’ share. If Banca d’Italia is “stopped out” on its local market by PSPP and PEPP reaching 33% anywhere else in the Euro area – and presumably first in Germany – then its impact on local “liquidity conditions”, which have an unfortunate tendency to turn into “solvency conditions”, could well be marginal.

Bond markets renationalization

A “renationalization” of bond markets is already at work in the US. In March, net sales of US treasuries by non-residents stood at USD299bn, the highest figure ever recorded (Exhibit 4). This was probably the reflection of extreme search for cash and a side-effect of some EM central banks selling dollars to support their currency, but the Fed’s resumption of QE is coming at the right time.

Last week we explored the conversion to QE of some key central banks in emerging markets as a reaction to a decline in capital inflows. Such renationalisation of bond markets could be another aspect of the more general “de-globalisation” reflected in the rise in protectionist practices and the decline in global trade.

In principle, it should only be temporary. Indeed, as the economy normalises, the central bank should gradually withdraw from direct interventions on the bond market while the accompanying return of risk appetite would bring non-resident investors back. This rosy normalization is not the only possible path though. We could see independent “financial blocks” harden. The need to manage over a long horizon the “debt overhangs” would keep central banks in play for long, and/or financial repression could be put in place to make sure that domestic savings would find their way to fund governments.

This is not just a theoretical concern. Geopolitical motives could also alter the free allocation of capital across global markets. The US administration on 11 May requested from the Thrift Savings Plan (the main government pension fund in the US) that they stop their investment in Chinese firms. The amounts at stake are small, but this could be part of a more general “financial decoupling strategy” aiming at weaning Chinese firms off tapping US markets for capital through mandatory de-listing for instance (such idea had been floated by Mr. Trump entourage in September 2019 already). China, which holds the second highest quantum of US government securities held by non-residents (USD 1.1tn, Exhibit 5) could respond in kind by reducing its exposure at a faster clip (it peaked at 1.3tn in 2011).

The UK’s double trouble

If there is a country where the government should not be too concerned by institutional hurdles to the central bank’s capacity to help it is the UK. The country stands out among advanced economies for the limits to its central bank’s independence. Setting the explicit inflation target remains firmly in the purview of the government, and failure to deliver on it forces the Bank of England to justify itself in a letter to the Chancellor of the Exchequer. The operational framework still presents vestiges of monetary funding of fiscal policy – the “Ways and Means” facility, in practice a temporary overdraft to the treasury, which has just been reactivated – which would not pass muster in the Euro area. Although the Bank chose on 6 May to refrain from announcing an expansion of its current QE programme, we have never doubted that massive QE would always be on offer if need be with none of the limits the ECB is facing.

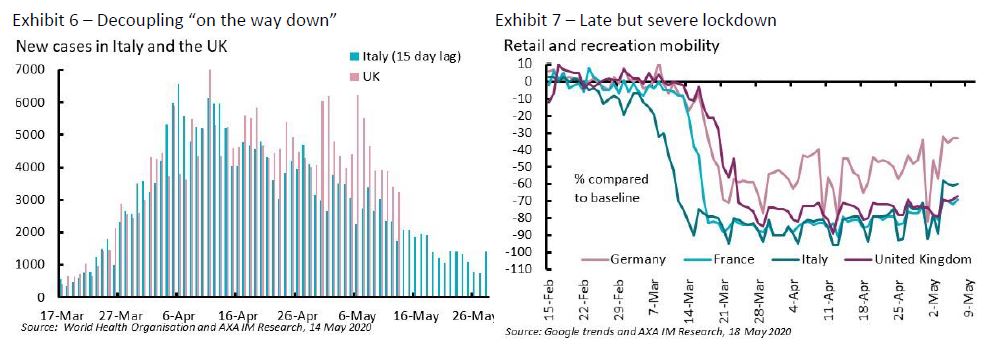

Still, we fear that the UK may well need all the Bank of England’s “readiness to help” to deal with its current predicament. Indeed, on the pandemic front the country is not faring well. On the ascending phase of the propagation of covid-19, the UK was behaving like Italy with a lag of about two weeks. Unfortunately, during the declining phase of the epidemic, the UK has not been able to reduce the number of new cases as fast as Italy (Exhibit 6). The UK now has the highest absolute number of victims in Europe, and this holds also for “alternative measures”, e.g. excess mortality for all causes recorded by national statistical institutes. Q1 GDP came out better than in the Euro area (-2.0% against -3.8%), but this was the reflection of a lag in the lockdown measures, not a difference in the severity of the measures. According to Google trends, the contraction in activity in the UK is on par with that seen in France, Italy and Spain (Exhibit 7). Given the difficulty in keeping the epidemic in check, the UK is extending lockdown measures for longer than in those countries. The UK initially behaved like the US, with a late and reluctant lockdown. The resemblance is no longer there.

In addition to the pandemic shock, the UK needs to negotiate a free trade agreement with the EU before the end of the year – the term of the post-Brexit transition period. The end of June is the last moment when in principle another extension can be requested. The UK government is publicly adamant it won’t request one, while the number of thorny issues to iron out ahead of a good quality Free Trade Agreement remains daunting.

Significant bouts of imported inflation have been a frequent feature of the British economy since the Great Recession. The combination of a deep pandemic shock, post-Brexit uncertainty and possibly ultra-accommodative monetary policy could trigger further weakness in the exchange rate, leading to another shock to prices at a moment when purchasing power is already struggling.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.