The language of a crisis

- 22 April 2020 (5 min read)

Alongside rigorous financial statement analysis, the detailed evaluation of text data has become an important part of Rosenberg Equities’ research and investment process. In this short update, Alex Ions, Head of Alternative Data Research, and Research Analyst Euan Mackay discuss what earnings transcripts and regulatory filings can tell us about companies’ and analysts’ reactions to the coronavirus outbreak.

As part of Rosenberg Equities’ analysis of text data, for the past two years we have announced an annual “Word of the Year”, using our proprietary natural language processing framework to identify what mattered most to managers and analysts based on the words they used in quarterly calls and regulatory filings.

While annual updates provide an interesting longer-term perspective, one of the strengths of our framework is the ability to run the numbers every day. This enables us to capture short-term shifts in sentiment and see market trends take shape on an almost real-time basis.

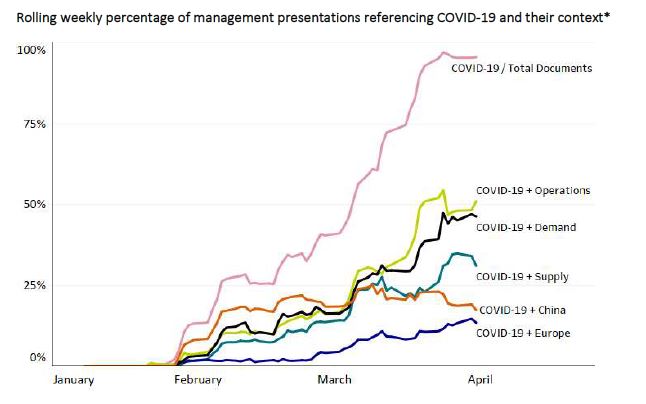

This more immediate perspective yields a clear picture of the most important topic so far this year: Covid-19. In line with the tragic spread of the coronavirus across the world in recent months, references to it – as well as to related terms, such as “pandemic” – have sharply increased. Analysing close to 5,000 earnings calls since the start of this year, we find that these “keywords” went from appearing in almost no meetings at the beginning of the quarter to featuring in essentially every management presentation by the end of March.

As the chart below shows, initial mentions of Covid-19 by management teams were largely related to its outbreak in China, but began to focus on the broader impact to global supply and demand as the quarter progressed. Similar patterns are also evident in the questions analysts posed to managers and in companies’ regulatory filings, where the crisis has come to dominate disclosures in recent weeks as executives sought to inform investors about interruptions to their operations.

From information to insight

The language that managers and analysts use can tell us much about the sentiment around individual stocks and the market as a whole.

For example, raw ‘language sentiment’ scores can give us an insight into managements’ confidence at a given point in time. They can also alert us to how analysts are responding to their strategies.

Beyond this, by evaluating how the language in analyst meetings and corporate filings has evolved over time we gain a sense of the trajectory of sentiment around a company, complementing what we see in other data sets, such as price momentum, media coverage and analysts’ earnings revisions. Aggregating this data can reveal a big-picture view of the direction of sentiment in the economy.

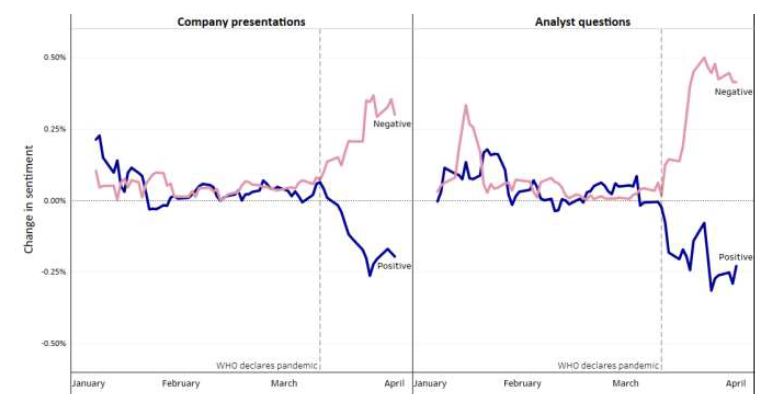

Unsurprisingly, the latest shift in sentiment has been decidedly negative. As the charts below show, companies’ presentations on earnings calls have become increasingly pessimistic since the start of March and the tenor of analyst questions has turned similarly negative, although the latest data suggest some improvement.

Clearly, this is a short-term view of a highly complex and extremely fast-moving crisis. These conditions create challenges to detailed analysis that must be carefully managed. We must also recognise that the data suggest most managers and analysts were late to recognise the severity of the coronavirus and its likely business impact. (Notice that the spike in negative sentiment shown in the charts came only after the WHO’s official declaration of a pandemic on March 11.)

Conclusion

As the collective understanding of the virus improves, company statements and analyst questions should reflect this, providing more nuanced information around the risks and opportunities faced by individual firms and how they are approaching them. This could increase the quality of insights we can glean from the analysis.

In time, we also hope to see other signs in the data. Most notably, as the global response to the coronavirus gains traction, we look forward to seeing references to our keywords stabilize and eventually fall and the tone of the references start to improve. These would be early markers that the world is beginning to recover from this crisis.

Change in sentiment, 1-week moving average1

- U291cmNlIG9mIGFsbCBkYXRhIGlzIFJvc2VuYmVyZyBFcXVpdGllcywgYXMgb2YgMSBBcHJpbCAyMDIwLCBiYXNlZCBvbiBvdXIgZ2xvYmFsIGludmVzdG1lbnQgdW5pdmVyc2UuIENoYW5nZSBpbiBzZW50aW1lbnQgZm9yIGVhY2ggbWVldGluZyBpcyBtZWFzdXJlZCByZWxhdGl2ZSB0byB0aGUgY29ycmVzcG9uZGluZyBjb21wYW55IG1lZXRpbmcgaW4gMjAxOS4gQ2hhcnQgc2hvd3MgYXZlcmFnZSBzZW50aW1lbnQgYWNyb3NzIGFsbCBjb21wYW5pZXMgaGF2aW5nIG1lZXRpbmdzIGluIGEgMS13ZWVrIHRyYWlsaW5nIG1vdmluZyB3aW5kb3cuICZuYnNwOw==

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.