(Really) not there yet

- 01 November 2021 (5 min read)

- Divergence between emerging and advanced economies reduces the chance of success of COP26 – possibly another side-effect of the Great Rivalry between the US and China.

- We think the market pricing of the ECB’s first hike is too aggressive, but we are probably stuck in a waiting game until inflation slows down and vindicates the central bank. Until then, volatility will rise.

Expectations for the outcome of COP26 are now very low, after the G20 meeting failed to produce more tangible commitments for the intermediate decarbonization target of 2030, beyond a generic statement to reach net zero “by or around mid-century”. It seems that China’s interest in the COP26 has diminished just as Biden stated his intention to take an international leadership position on climate upon bringing back his country to the Paris agreement. Chinese officials have recently rekindled the old dispute between emerging and advanced economies on the “burden sharing” of decarbonization, while Beijing’s updated Nationally Determined Contribution (NDC) provides only minimal progress on their own intended trajectory by 2030.

To be fair, it would be too easy to blame the lack of collective ambition on the emerging countries alone: an assessment of updated NDCs excluding China’s but including the US and the EU’s suggest GHG emissions would be only c.10% below their 2010 level by 2030, while a decline of 45% is necessary to keep global warming to 1.5 degrees. Yet, it may well be that COP26 is a victim of the Great Rivalry between the US and China. If the cooperative approach weakens, we suspect trade policy will be an instrument of choice to force faster decarbonization in laggards. We note that upon burying the hatchet on their steel trade war last weekend, the US and the EU agreed to work on a framework to take sustainability criteria into account in trade relations.

Still, COP26 is not just about intergovernmental negotiations. It has federated efforts by the private sector, and especially the financial industry. We think this is only a start, especially since governments everywhere are likely to use the “sustainable finance lever” even more if the outcome of the COP26 negotiations is mediocre.

It was not a good week for the ECB, which failed to convince markets to give up on their very aggressive pricing of the first rate hike despite statements which we consider as quite dovish. We continue to think that the market got carried away. The ongoing tightening in financial conditions may ultimately force the central bank to remain accommodative for even longer than what the governing council intended based on their latest forecasts. Still, we expect a “waiting game” for several months, until inflation starts slowing down and vindicates the governing council’s view. In the meantime, the ECB will have to be very disciplined in its communication, but it does not control all the levers there: the latest hawkish statement by Germany’s FDP leader – and potential finance minister - on monetary policy will not help calm the market down.

Far off the mark

Beyond setting a more ambitious – albeit “softish” – target for average temperature rise by the end of the century (parties agree to “pursuing efforts to limit the temperature increase to 1.5°C above pre-industrial levels”), the most tangible achievement of the Paris agreement of 2015 was to set up a mechanism to monitor individual countries’ progress towards decarbonization. Each of the Treaty’s party agreed to submit every five years a detailed account of its planned reduction in GHG emissions (Nationally Determined Contributions – NDCs), complying with minimum transparency criteria, which would “ratchet up” at every round (i.e., governments would commit to more ambitious decarbonization targets in every new version of their NDC).

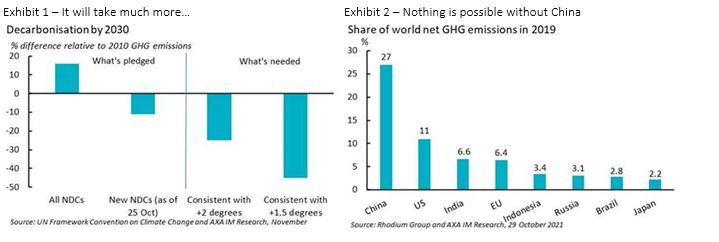

The assessment of these NDCs, published by the United Nations (UN) on 25 October based on the latest version of 165 NCDs available as of 25 October does not make for comforting reading. The total global greenhouse gas (GHG) emission level would be 15.9% above the 2010 level by 2030, while the scientific consensus considers a decline of 45% by 2030 is what is needed to limit global warming to 1.5 degrees (see Exhibit 1).

Of course, this assessment Is based on the pledges available in the NDC repository at the cut-off date and some participants had not produced updated targets in time. The “elephant in the room” is China, which in 2019 accounted for 27% of global net GHG emissions, against 11% for the US and 6.4% for the EU (see exhibit 2), and which has submitted its new NDC on October 28 only, too late for the secretariat to take it into account in its analysis. On substance, though, it’s unlikely that it would have changed its results much. Indeed, while China has committed to reach net zero by 2060 last year, progress relative to the 2016 version for the 2030 intermediary target is minimal : the new version targets a peak in GHG emissions in 2030 at the latest, against “around 2030” in the old one, but this hardly constitutes a profound alteration in the trajectory. Xi Jinping’s absence from Glasgow will make this lack of ambition even more glaring.

Possibly sensing the risk of backlash, China’s Ambassador to the UK extolled his country’s contribution to the fight against climate change in a letter to the Guardian, but perhaps more fundamentally, a careful reading might shed light on what is behind China’s “distance-taking” from the Paris process. Indeed, the Ambassador focused on the need to balance the efforts of developing and emerging economies with those of more advanced countries in a rather blunt fashion: “Developed countries with a couple of hundred years of industrialisation behind them and historical environmental debts should make bigger contributions to tackling pollution and protecting the environment, instead of pinning the responsibility on China and other developing countries”, then calling on the developed nations to make good on their Paris pledge to find USD100bn a year to help poorer nations to mitigate (and adapt to) global warming, a target which was due to be hit in 2020.

China there puts the finger on another source of disappointment when it comes to assess the tangible effects of the Paris agreement. The OECD – in charge of monitoring the pledges towards this USD100bn target – reported earlier this month that for 2021 the amount would be in a range of USD82 to 88bn only, and that USD100bn would not be reached before 2023.

While the Paris agreement reflected stronger North/South convergence on the fight against climate change, we find quite telling that India, now standing for a slightly higher share of world emissions as the EU at 6.6%, hasn’t updated its NDC as we write. Brazil has provided an update to its first NDC which merely re-states the same objectives as in 2015, in contradiction with the intended “ratcheting up” of the Paris agreement. The “giants” of the emerging world have not fully embraced the COP process.

In this context, Beijing may be tempted to take the lead of developing/emerging nations against the advanced economies as part of its overarching will to counter US influence. Given the seemingly unstoppable rivalry mounting between China and the US, the fact that Biden is vying to take a global leadership role on the fight against climate change on the occasion of COP26, operating a complete turnaround for Washington policy under Trump, may make this process less attractive to Xi Jinping.

Still, the gap on the decarbonization pace between the existing pledges and what’s needed cannot be reduced to China’s reluctance, or the BRICs’, to adjust their NDCs. The UN secretariat produced a separate assessment of the policies put forward by the countries which submitted new versions in time. Even for this subset, the pace of decarbonization would still fall far off the mark: GHG emissions of these countries would fall by only c.10% by 2030 (that’s the second column from the left in Exhibit 1). In clear, assuming all parties were to converge to the pace set by these countries, this would still be too slow to protect against a global warming exceeding 2 degrees by the end of the century, let alone the 1.5 degrees soft target. The new, more stringent objectives set by the EU and the US – which both submitted their new NDCs in time to be considered in the UN’s assessment – did not move the dial enough.

Going one step further, immediate doubts as to the signatories’ capacity to deliver on their pledges may well emerge while the leaders are still talking in Glasgow. Making electricity net zero by 2035 was a key “sub-target” in the NDC update submitted by the US in April. As we discussed two weeks ago in Macrocast, this is already being tested in Congress, given the necessity for Biden to downscale his ambitions on creating a substitute to carbon pricing in the US, in the form of a bonus/malus imposed on power generation companies according to the carbon intensity of the production mix. We note that in the same letter to the Guardian, the Chinese Ambassador made a point of highlighting his country’s capacity to deliver on pledges, a thinly veiled criticism of the difficulties liberal democracies meet when dealing with the cost of transition.

On substance, we do not agree with the trope according to which non-liberal states can more easily deal with the fight against climate change. The challenges are simply expressed differently. Democracies find it difficult to set a clear decarbonisation path given the different views of competing parties (even when they agree on the principle – as is the case in most western countries with the exception of the US – they usually disagree on the actual measures). But authoritarian regimes, focused on maintaining “social stability”, could well ultimately balk at the cost to economic growth, accumulated wealth and purchasing power which decarbonisation can entail.

The G20 meeting – where crucially advanced and emerging countries such as China meet - which concluded last weekend, setting the tone for COP26, did not point to much progress on the intermediary 2030 targets, even if all members agreed to reach net zero “by or around mid-century”, which is vague enough to accommodate both the US and the EU’s 2050 and China’s 2060. Expectations are now so low on the outcome of COP26 that upside surprises cannot be discarded. It may well be that China – and India – may choose to make additional announcements at the conclusion of the COP, potentially in exchange for some concessions from the advanced economies. Progress is also possible on targeting methane emissions more specifically or doing more to curb deforestation.

We are not holding our breath though, since we see many opportunities for North/South conflict arising. On the occasion of the G20 meeting the EU and the US managed to put an end to their “trade war” on steel and aluminium. The additional “classical” tariffs on European steel and aluminium imposed under the Trump administration will be transformed into a “tariff rate quota”, which kicks in only when a certain volume of imports is reached, instead of affecting the first dollar of shipments. Details are still scarce as we write but press reports suggest 2/3 of pre-Trump EU exports of steel and aluminium to the US would become tariff-free. In return, the EU will lift the retaliatory duties. What we find interesting is the justification used by US Commerce Secretary Gina Raimonda to explain the deal to the US press: the lower carbon intensity of EU steel and aluminium relative to China’s (for which the tariffs are not being reduced), announcing the US and the EU had agreed on the principle of taking into account carbon intensity in metal trade, and noting that “China’s lack of environmental standards is part of what drives down their costs, but it’s also a major contributor to climate change”.

We have been highlighting this in Macrocast since we’ve started writing on climate issues: there is a significant risk that climate policies focus more on more on international trade and get “polluted” by the rivalry between the US and China. Beyond the introduction of sustainability criteria in the US tariff policy, the EU’s conversion to a “border tax” was a significant step. Now, creating a “western decarbonisation alliance” would come with its own internal contradictions. The current gap in carbon intensity between the US and the EU is likely to make the former less keen on expanding too stringent carbon criteria to many areas of bilateral trade. In addition, the “Western camp” is not fully united on key issues, as Australia’s opposition to a phasing out of coal, expressed again at the G20, illustrates (we suspect Biden would face quite some opposition at home on this as well). Yet, we are concerned about the risk COP26 reflects a strategic rift across key GHG emitters. Non-cooperative approaches would be sub-optimal.

At the COP26 “fringes”

Now, the COP is not just about governments negotiating. It has also been a remarkable source of mobilisation against climate change by the private sector in general and the financial industry in particular, around initiatives such as the net-zero asset owner alliance (NZAOA), the net-zero asset managers’ initiative or the net-zero underwriting alliance in the realm of insurance. Irrespective of the results of the inter-governmental discussion, progress in private sector involvement is likely to continue. Public opinion – and clients’ – pressure is significant, and there is a widespread recognition in the financial industry that it would be next to impossible to achieve decent returns at an acceptable level of risk in a world in which climate change is not curbed.

The emergence of green finance regulation is providing another form of incentives to the financial industry. The EU has taken the lead on these matters, but in the US, even though legislative progress is limited for now – possibly another consequence of the extremely constrained capacity to unlock any congressional process – the SEC is now extending its scrutiny to this field. We are convinced that governments will be increasingly tempted to use the “financial lever” to accelerate the shift to net zero, steering capital allocation away from the most carbonated activities, with transition costs which may be less immediately visible to public opinion than traditional fiscal measures. If COP26 disappoints on the inter-governmental front on more tangible decarbonisation pledges, we expect more pressure on the financial industry. More regulation on sustainable finance should be welcome, helping to create a level-playing field, especially if it comes with a minimum of international harmonization. But efforts from the private sector cannot be perfect substitutes to public action. Key issues, such as carbon pricing, both internally and in the realm of international trade, or key energy choices, require political decisions. Clarity on these would provide visibility for private actors to alter capital allocation, and the cost of capital across sectors, in the right direction.

“Inflation, inflation, inflation”

Discussing the likely trajectory for monetary policy looks obviously much less existential than the fate of COP26, but we suspect the market ramifications of the former will, at least for the near future, be more spectacular.

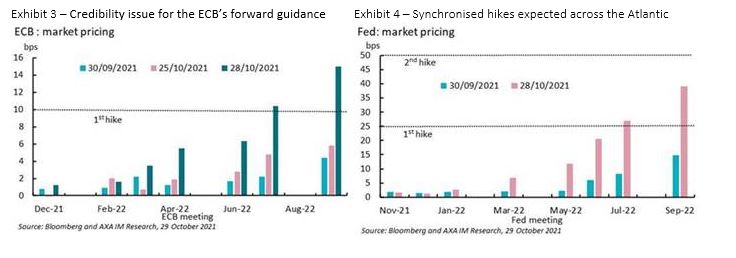

The European Central Bank (ECB) very rarely comments on market pricing. Lagarde did so last week. Her exact words were “our analysis certainly does not support that the conditions of our forward guidance are satisfied at the time of lift-off, as expected by markets, nor any time soon thereafter”. This does not leave much room for interpretation: the ECB disagrees with the market’s view that policy rate could rise next year. There were other dovish aspects in Lagarde’s statement. She also stated that the current uplift in inflation expectations could help the ECB deliver on its medium-term 2% inflation target, reminding everyone that no so long ago, the challenge facing the ECB was its inability, year after year, to resist deflationary pressure. In normal circumstances, this would have been more than enough to calm the market down. This time, it did not, which is testament to the “tide turn” in the market as far as inflation expectations go.

In a nutshell, the market right now does not believe the ECB – nor the Federal Reserve (Fed) for that matter – when they repeat, as Lagarde did last week that inflation will ease back in 2022, as the demand/supply disconnect resolves and base effects disappear, even if the ECB now concedes that the current inflation spike could last longer than expected. Lagarde’s choice of words may not have been optimal, for instance when she exclaimed “inflation,inflation, inflation” when asked about the Council’s discussions, which drowned the actually dovish content of her explanation of the current analysis of the ECB. Still, it seems to us that the bar for successfully pushing back the market’s expectations was simply too high last week. Immediately after the press conference, one and half 10 basis points ECB hike was priced by the market by August 2022, a full 10 basis points more than at the beginning of the week (see Exhibit 3).

We continue to think that expecting the ECB to hike next year is very aggressive. Beyond the points made by Lagarde on the transitory nature of the inflation shock – which we share – the current market pricing for the first rate hike would imply either (i) that the central bank would raise its policy rates before the end of quantitative easing (in the latest monetary analysts survey, APP was seen as continuing well into 2023) or (ii) that the ECB would terminate all its QE programmes very quickly after March 2022 (which has been confirmed by Lagarde last week as the likely date for the end of PEPP).

The first option looks contorted to us. It is technically thinkable, but if the macroeconomic outlook is seen as sufficiently worrisome – in terms of avoiding an all-out inflation shift – to justify a rate hike, then surely it would also warrant the termination of quantitative easing, which in the ECB’s communication has always been presented as the “second line of defence” once moving policy rates down was insufficient to bring inflation back towards 2%. The ECB could try to justify a continuation of QE by the need to deal with a potential “fragmentation” of the Euro area bond markets, but as we discussed a few weeks ago, doing so without conditionality would completely destroy the framework painfully negotiated in 2012 to deal with the sovereign crisis.

It’s more likely to us that the market is currently so concerned with inflation – and the vocal noises coming from the hawks – that it is bringing forward its expectation for the end of QE (which can only be indirectly observed in pricing). This would explain the significant widening in the Italian spread after Lagarde’s speech – 10Y Buoni del Tesoro Poliennali (BTP) broke 1% as Christine Lagarde was speaking. They settled at 1.17% at the end of last week, their highest level since the summer of 2020. In other words, the market pricing of the ECB’s course of action is currently triggering an already visible tightening in financial conditions.

The exchange rate could also be another source of tighter financial conditions. Last summer, thanks to its new – dovish – forward guidance which emerged of its strategy review, the ECB managed to widen the gap with the expected trajectory for the Fed. Such widening contributed to the further weakness of the euro. This is no longer the case: on both sides of the Atlantic, the market is now pricing the first hike – albeit by only 10 bps in the Euro area against a full 25 bps one in the US – at the same time (see Exhibit 4). Fortunately, last Friday, the market corrected most of the euro appreciation observed on Thursday, but the warning shot was significant. At a time when the Euro area exports could be impaired by slower traction from China, the last thing it needs right now is an appreciating currency.

Such market-led tightening in financial conditions would – if unchecked – ultimately weigh negatively on the ECB’s outlook for growth and inflation. This is precisely why we think that the central bank will have to maintain a dovish language in the months ahead. Losing control of the market could trigger a slowdown in economic activity which would impair the chances to see Euro area inflation re-anchor at 2% on a sustainable basis. However, given the current divorce between the ECB’s view and the market’s, we suspect that we are going to be stuck in a “waiting game” for some time, i.e. until inflation comes down to justify the ECB’s analysis.

During that phase, the ECB will have to be very disciplined on its communication, but quite a few levers are now out of their direct control. Jens Weidmann’s early exit may be complicating matters. Christian Lindner, who has explicitly asked the finance ministry as one of the prices to pay for FDP’s support to a coalition with SPD and the Greens, issued a very hawkish statement on Sunday, warning the ECB against “being caught up in the fiscal policy of heavily indebted countries, it would have little means to fight inflation” . In a way, the risk is not so much that Berlin ends up appointing another hawk to the ECB Governing Council – Weidmann’s opposition to unconventional policy had turned somewhat “ritualistic” and had little actual impact on the ECB decision-making – but rather that the central bank would be subject to constant criticism from Germany’s finance ministry, something which had been largely under control since 2012. Too many hawkish noises from Berlin could push the market even further against the most fragile sovereign signatures.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.