US High Yield Market Review

- 12 January 2021 (5 min read)

Review of 2020

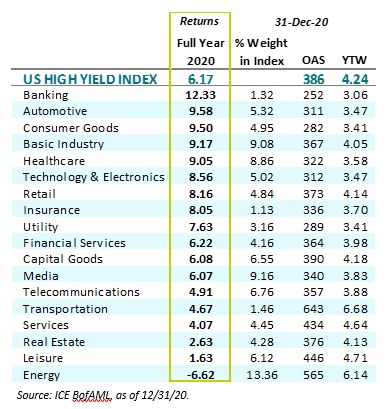

The US high yield market (as represented by the ICE BofA Merrill Lynch US High Yield Index) produced a 6.17% return in 2020, slightly better than the yield-to-worst at the start of the year, and in-line with the average coupon. However, any casual observer of financial markets would recognize that 2020 was not a simple coupon-returning year. The negative impact of Covid-19 and subsequent economic lockdowns, followed by the positive impact of unprecedented fiscal and monetary support, created significant volatility and opportunities during the year.

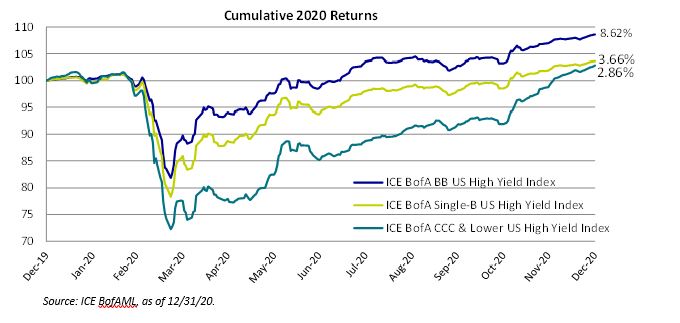

The US high yield market trailed equity indices and higher quality, longer duration fixed income indices in 2020. Higher quality securities also outperformed lower quality securities within the US High Yield market, as BB, B, and CCC rated bonds returned 8.62%, 3.66%, and 2.86%, respectively. The double B rated portion of the market benefited from Fallen Angels, which saw a large portion of their price declines happen while rated Investment Grade, and the following rebound in prices occurred while rated double B. The longer duration of Fallen Angels and BB-rated securities also helped their performance relative to B-rated or CCC-rated securities. Permanent losses from an increase in the default rate negatively impacted the returns of the lower rated portion of the market and the Energy sector. However, the combination of defaulted securities leaving the index and a strong risk-on environment at the end of the year led to the significant outperformance of triple C and the Energy sector in the 4th quarter, closing some of the return gap for the full year 2020.

Breaking down the 2020 return into the sell-off that occurred in the 1st quarter and the rally that occurred the last 3 quarters of the year, we see a typical return outcome within our custom buckets under both time frames. Once again, short duration securities showed how they can limit drawdowns in difficult environments, as was the case in q1 of 2020. However, higher yielding and longer duration securities led the market higher for the remainder of the year.

Q1 2020:

| Avg. | Q1 Total | |

| AXA Custom Bucket | Weight | Return |

| Duration to worst 0-2 | 28.03 | -6.06 |

| 0-5% Yield | 25.20 | -7.83 |

| Duration to worst 2-3 | 18.01 | -9.80 |

| Long duration | 3.23 | -12.74 |

| 5-6% Yield | 7.07 | -13.82 |

| 6-7% Yield | 4.02 | -16.40 |

| 7-8% Yield | 3.10 | -22.37 |

| 8-9% Yield | 1.98 | -25.14 |

| 9+% Yield | 9.35 | -35.13 |

| Grand Total | 100.00 | -13.12 |

Source: AXA IM, Factset, as of 12/31/20. Securities re-grouped monthly.

Q2-Q4 2020:

| Avg. | Q2-Q4 Total | |

| AXA Custom Bucket | Weight | Return |

| 9+% Yield | 13.18 | 61.34 |

| 8-9% Yield | 2.98 | 41.57 |

| Long duration | 4.77 | 41.03 |

| 7-8% Yield | 5.13 | 31.56 |

| 6-7% Yield | 6.61 | -26.61 |

| 5-6% Yield | 9.67 | 21.57 |

| 0-5% Yield | 22.76 | 13.61 |

| Duration to worst 2-3 | 13.18 | 12.38 |

| Duration to worst 0-2 | 21.72 | 6.43 |

| Grand Total | 100.00 | 22.20 |

Source: AXA IM, Factset, as of 12/31/20. Securities re-grouped monthly.

2021 outlook

2020 reminded us that market outlook reports and investment plans at the start of a calendar year can become obsolete much sooner than expected. The swift changes in the economy and asset valuations that occurred in March of 2020 quickly altered any strategic plans that were set at the beginning of the year. We believe 2021 also calls for a flexible strategy in investing in the US High Yield market. The severity of Covid-19 in the winter months, the progress made in distributing vaccines, inflation data and continued fiscal and monetary policy adjustments will all have the potential to shift economic forecasts and valuations rather quickly. Similar to 2020, a strategy that can quickly adjust positioning during periods of volatility should prove successful in 2021.

Amazingly, despite the volatility of the past 12 months, the market finds itself in a similar position today as it did this time in the previous year, from a valuation perspective. Both 2020 and 2021 started the year with a historically low yield-to-worst and a significant portion of the market trading to its first call date. Compared to a year ago, today’s market has a slightly higher spread, a lower yield-to-worst, fewer higher yielding securities and a higher percentage of longer duration securities. Our custom market segmentation compares the two time periods below:

Undoubtedly the US high yield market’s return of 6.48% in the fourth quarter of 2020 took away some 2021’s return potential. Despite a low yield-to-worst to start the year, we still think it is reasonable to expect a 4-6% return for 2021. Our positive outlook for the US high yield market over the near to medium term hinges on the draught of high yielding opportunities in the current global fixed income environment. The lack of yield in other global fixed income markets will continue to support demand for the US high yield asset class. Combined with our expectation that net new issuance will be lower in 2021 than 2020, market technicals should continue to have a positive impact on spreads. In addition, fundamentals should improve and the default rate should decline throughout the year.

A return above our expected 4-6% range would have to be an environment that includes a strong economic recovery, a significant rebound in sectors that were deeply impacted by Covid-19 (Energy, Leisure, etc.), and Treasury rates remaining near all-time lows. A return below our range would be driven by either an increase in rates as the economy recovers (where HY outperforms IG and BB-rated securities underperform B and CCC), or a scenario where the distribution of the vaccine disappoints and the economy is slower to fully recover (IG outperforms HY, BB-rated securities outperforms B and CCC).

In conclusion, the current valuation of the market leads us to structure a more defensive positioning to start the year, with a preference for shorter duration securities. We continue to be cautious towards longer dated BB-rated securities that are trading to earlier call dates, as the negative convexity in these bonds is unappealing to us. We also believe outperforming returns can be achieved by seeking off-the-run securities with idiosyncratic return potential, rather than chasing high beta securities from today’s valuations. Flexibility is key in our strategy, as we expect to have the opportunity to pivot this positioning in favor of better valuations in some portions of the market in the future.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

The ICE BofA Merrill Lynch High Yield Index is composed high-yield corporate bonds and other distressed securities. Taxable and tax-exempt US municipal, DRD eligible and defaulted securities are excluded from the Index. Indices are rebalanced monthly by market capitalization. An index is unmanaged and is not available for direct investment.

Issued in the U.K. by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the U.K. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries. © 2021 AXA Investment Managers, Inc. All rights reserved.