EM titans: How China and India are driving growth for fixed income investors

- 15 September 2021 (7 min read)

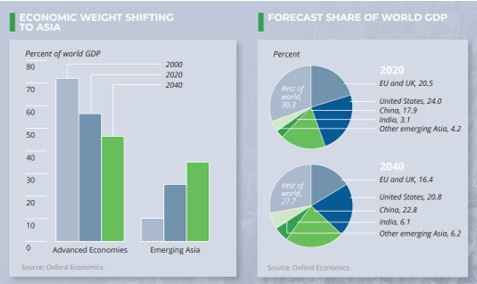

Changes in domestic consumption patterns in emerging markets and the rise of the middle class are likely to see a huge shift in economic power away from advanced economies - and Asia is expected to be the main beneficiary of this change. The chart below illustrates the dramatic increase in Asia’s contribution to global GDP over the past 20 years – a trend which is expected to continue to only grow. By 2040, emerging Asia is forecasted to contribute over 35% of global GDP compared to 25% now, almost matching that of advanced economies.

China and India are forecast to be the main drivers, with their combined contributions to global GDP forecast to increase from 21% to 29% by 2040. As a result, in 20 years’ time, China is predicted to be the largest single contributor to global GDP, with India the third highest, marking a huge shift in terms of taking economic power away from the G7 countries.

One vital factor behind this growth has been the massive growth in the two countries’ populations - now the two most populous in the world. China currently boasts a population of 1.45 billion1 – to put this into perspective, the province of Beijing has a population comparable with Finland, Norway and Sweden combined. This huge human capital has been a key reason for China’s emergence as a global superpower.

India is currently home to just under 1.4 billion people, representing roughly 20% of the global population. This figure is anticipated to grow to around 1.7 billion by 2050, overtaking China as the world’s most populous country. By this time, it's estimated that the size of India's working age population will be comparable to China's current working age population of 800 million, a key indicator of the potential for economic growth.

As a result, over the last 20 years China has exhibited average annual GDP growth of 9%, a huge number compared to more developed countries. This has translated into a huge surge in manufacturing and infrastructure development, and today China accounts for over 50% of global demand for cement, nickel, steel and copper.

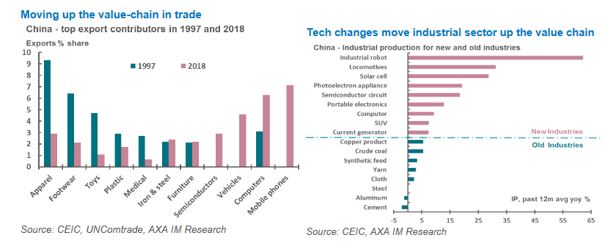

China’s economic model, previously dubbed the ‘world’s factory’, has begun its transition to ‘lead innovator’ with a move up the global value chains with a huge investment in technology.

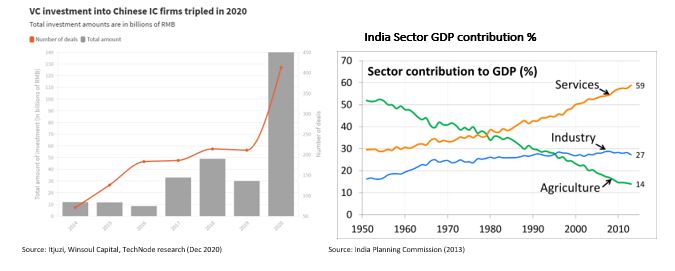

China is already making significant advances in research development spending, research publications and patents granted. For example, the country has started a mass-scale investment in semiconductors, with $35bn flowing into the industry in 2020 and the amount of private capital investment more than tripling from the previous year2 . This investment is likely intended to reduce reliance on other countries, in particular the US, for imported chips, and to support China’s ambition to lead the world in high-tech areas such as artificial intelligence, supercomputers, and electric vehicles.

In India the service sector, covering a wide array of activities such as trade, leisure, accommodation, transport and communication, has also been a key driver of Indian and global economic growth over last three decades.

After its economy growing by an average of around 6.5% over the last 20 years, India’s GDP is expected to increase another 80% by 20303 . The country is making a huge investment in infrastructure to increase the sustainability of its economic growth, which can be seen in the development of its healthcare and real estate sectors. India is seeking to provide 500 million people with government-sponsored health insurance, which could translate to one of the fastest growing healthcare markets in the world. This opportunity is capturing the attention of foreign investors, and we have seen around $25bn of foreign investment in Indian healthcare over the last 20 years4 .

In addition, India has been key in the production of coronavirus vaccines, a strong indication of the development of the country’s healthcare sector. Alongside this comes the rapid rise of megacities and the associated economic impacts of urbanisation.

This has been a significant trend in Asia with the development of a new generation of smarter cities with new infrastructure and services. With 10 million people migrating to its cities each year, real estate development is another top priority for India5 . Supply shortages are offering opportunities for both domestic and foreign developers, and the government is encouraging this by allowing 100% ownership of real estate projects.

Looking ahead, the real estate market in India is expected to be worth $1trn by 20306 , representing huge potential for investors.

Both China and India have enjoyed huge growth in recent decades, but we believe there is still huge potential for their economies to expand. By investing in manufacturing, infrastructure development and technology, both countries have increased the sustainability of their economic growth and ensured their status as global superpowers for decades to come.

- WzFdIFBvcHVsYXRpb24gJmd0OyBXb3JsZCAtIFdvcmxkb21ldGVyICh3b3JsZG9tZXRlcnMuaW5mbyk=

- SXRqdXppLCBXaW5zb3VsIENhcGl0YWwsIFRlY2hOb2RlIHJlc2VhcmNoIChEZWMgMjAyMCk=

- T0VDRCAoMjAyMCk=

- SUJFRiAoQXVnIDIwMjAp

- SWJpZC4=

- S1BNRyAoU2VwdCAyMDE4KQ==

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities. It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.